2015 ALEC Comments on IRS Reg-138344-13

•

1 like•1,266 views

The Internal Revenue Service (IRS) has proposed new regulations threatening taxpayers who support charities. Yesterday, the American Legislative Exchange Council (ALEC) submitted comments to the IRS in an effort to protect those donors. Find out more at alec.org

Recommended

Recommended

More Related Content

More from ALEC

More from ALEC (10)

Recently uploaded

Recently uploaded (20)

2015 ALEC Comments on IRS Reg-138344-13

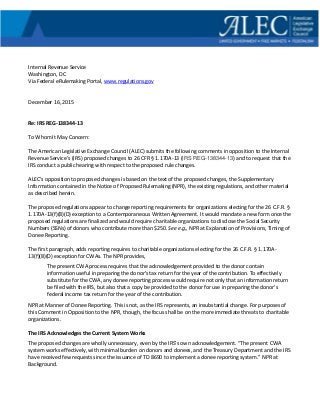

- 1. Internal Revenue Service Washington, DC Via Federal eRulemaking Portal, www.regulations.gov December 16, 2015 Re: IRS REG-138344-13 To Whom It May Concern: The American Legislative Exchange Council (ALEC) submits the following comments in opposition to the Internal Revenue Service’s (IRS) proposed changes to 26 CFR § 1.170A-13 (IRS REG-138344-13) and to request that the IRS conduct a public hearing with respect to the proposed rule changes. ALEC’s opposition to proposed changes is based on the text of the proposed changes, the Supplementary Information contained in the Notice of Proposed Rulemaking (NPR), the existing regulations, and other material as described herein. The proposed regulations appear to change reporting requirements for organizations electing for the 26 C.F.R. § 1.170A-13(f)(8)(D) exception to a Contemporaneous Written Agreement. It would mandate a new form once the proposed regulations are finalized and would require charitable organizations to disclose the Social Security Numbers (SSNs) of donors who contribute more than $250. See e.g., NPR at Explanation of Provisions, Timing of Donee Reporting. The first paragraph, adds reporting requires to charitable organizations electing for the 26 C.F.R. § 1.170A- 13(f)(8)(D) exception for CWAs. The NPR provides, The present CWA process requires that the acknowledgement provided to the donor contain information useful in preparing the donor's tax return for the year of the contribution. To effectively substitute for the CWA, any donee reporting process would require not only that an information return be filed with the IRS, but also that a copy be provided to the donor for use in preparing the donor's federal income tax return for the year of the contribution. NPR at Manner of Donee Reporting. This is not, as the IRS represents, an insubstantial change. For purposes of this Comment in Opposition to the NPR, though, the focus shall be on the more immediate threats to charitable organizations. The IRS Acknowledges the Current System Works The proposed changes are wholly unnecessary, even by the IRS’s own acknowledgement. “The present CWA system works effectively, with minimal burden on donors and donees, and the Treasury Department and the IRS have received few requests since the issuance of TD 8690 to implement a donee reporting system.” NPR at Background.

- 2. Assuming the proposed regulations apply only to charitable organizations electing to follow the (f)(8)(D) exception, it is unclear whether the regulations would be extended to organizations providing CWAs given statements in the “Background” section of the NPR.1 Statements as to the voluntary nature of the reporting provide little, if any, assurance, that the proposed regulations will not be extended to include CWAs. The Proposed Regulations Improperly Impinge Upon the Rights of the Donors to Engage in Anonymous Speech Requiring charities to disclose to the government their donors and the personal identifiers of those donors represents a significant threat to First Amendment private expression protections. Great works of literature have frequently been produced by authors writing under assumed names. Despite readers' curiosity and the public's interest in identifying the creator of a work of art, an author generally is free to decide whether or not to disclose her true identity. The decision in favor of anonymity may be motivated by fear of economic or official retaliation, by concern about social ostracism, or merely by a desire to preserve as much of one's privacy as possible. McIntyre v. Ohio Elections Commission, 514 U.S. 334 (1995). But First Amendment freedom of speech and association protections apply not only to literature, they apply also to all types of speech and association. It is beyond debate that freedom to engage in association for the advancement of beliefs and ideas is an inseparable aspect of the "liberty" assured by the Due Process Clause of the Fourteenth Amendment, which embraces freedom of speech Of course, it is immaterial whether the beliefs sought to be advanced by association pertain to political, economic, religious or cultural matters, and state action which may have the effect of curtailing the freedom to associate is subject to the closest scrutiny. NAACP v. Patterson, 357 U.S. 449, 460-461 (1958). The United States has a long history of private expression. For example, Thomas Paine wrote Common Sense anonymously, and his publisher, Benjamin Rush, also remained anonymous. In the context of anonymous political speech, donor privacy is fundamental to the American experiment. Anonymous speech was enshrined in the fabric of America as early as the Federalist Papers when Alexander Hamilton, James Madison and John Jay wrote under the name Publius. Today, activists on all sides of any given issue seek to target individuals as a means to chill speech and silence debate in the marketplace of ideas. ALEC has long been the target of such pressure tactics at the hand of groups like Common Cause and national 1 “In recent years, some taxpayers under examination for their claimed charitable contribution deductions have argued that a failure to comply with the CWA requirements of section 170(f)(8)(A) may be cured if the donee organization files an amended Form 990, ‘Return of Organization Exempt From Income Tax,’ that includes the information described in section 170(f)(8)(B) for the contribution at issue. These taxpayers argue that an amended Form 990 constitutes permissible donee reporting within the meaning of section 170(f)(8)(D), even if the amended Form 990 is submitted to the IRS many years after the purported charitable contribution was made. The IRS has consistently maintained that the section 170(f)(8)(D) exception is not available unless and until the Treasury Department and the IRS issue final regulations prescribing the method by which donee reporting may be accomplished. Moreover, the Treasury Department and the IRS have concluded that the Form 990 is unsuitable for donee reporting.”

- 3. elected officials like Senator Richard Durbin. Pressure groups often demand ALEC member and donor lists to in turn pressure those donors away from educational exchanges undertaken at ALEC meetings. Should the IRS mandate disclosure of individual donor information, the same approach will likely be employed. Given countless past examples of activist groups using donor information to silence differing views, the IRS should not assume a different outcome is possible. Storing and Reporting Donor SSNs Will Significantly Increase the Risk of Cyberattacks Targeting Charitable Organizations The IRS also requests comments regarding the risk of identity theft. Specifically, the NPR requests comments on “potential risk for identity theft involved with donee reporting given that donees will be collecting donors' taxpayer identification numbers and maintaining those numbers for some period of time. The Treasury Department and the IRS request comments on whether additional guidance is necessary regarding the procedures a donee should use in soliciting and maintaining a donor's taxpayer identification number and address to mitigate the risk.” NPR at Explanation of Provisions, Manner of Donee Reporting. The collection of donors’ SSNs will place charities at greater risk(s) of cyberattacks, increase costs, and scare donors away. According to the NPR, the proposed regulations “will not have a significant economic impact on a substantial number of small entities.” This statement fails to consider the total cost relating to the increased risk of cyberattacks, cybersecurity, and the loss of donations due to donor security concerns.2 Identity theft and cyberattacks are growing threats. Cybercriminals target institutions storing private information, such as Target, grocery stores, and other such merchants. The proposed regulations increase the amount of private information charities must store. Because of the increase in cyberattacks, charities are reticent to collect and store donors’ SSNs. Requiring charities, such as ALEC, whether on a voluntary or mandatory basis, to store and report donor SSNs will subject them to increased, and unnecessary, risks of cyberattacks.3 The costs of cybersecurity have been growing rapidly, in recent years. According to some experts, for profit corporations spend $77 billion a year for cybersecurity, and that figure is likely to rise to $170 billion by 2020.4 At least one expert estimates the average cost to charitable organizations for data breach is over $200 per compromised record.5 And this does not account for the time and expense necessary to recover, the loss of donor confidence, and the time spent away from the charitable organization’s mission.6 The proposed 2 See e.g. “Weak Cybersecurity Can Lead to Big Risks”, 2014 NonProft Trends Issue IV, WeiserMazars; available at http://www.weisermazars.com/uploads/src/uploads/NFP_Trends_2014_Issue_4.pdf (last accessed December 16, 2015) 3 E.g. Johnson, Harvey, “Cyber Security for Non-Profits”, May 11, 2015, Guidestar; available at http://trust.guidestar.org/2015/05/11/cyber-security-for-not-for-profits/ (last accessed December 16, 2015). 4 Yakowicz, Will, “Companies Lose $400 Billion to Hackers Each Year”, Sept. 8, 2015, Inc.com; available at http://www.inc.com/will-yakowicz/cyberattacks-cost-companies-400-billion-each-year.html (last accessed, December 16, 2015). See also “The Cost of Immaturity”, November 7, 2015, The Economist; available at http://www.economist.com/news/business/21677639-business-protecting-against-computer-hacking-booming-cost- immaturity (last accessed, December 16, 2015). 5 Bui, Anh, “A Look at Cyber Security and Its Impact on Nonprofit Enterprises”, November 2015, Calibre CPA Group, available at http://calibrecpa.com/wp-content/uploads/Cyber-Security-12-15.pdf (last accessed December 16, 2015). 6 Id.

- 4. regulations represent a significant threat that charities, such as ALEC, will be exposed to “legal action, trouble with regulators, and damage to their regulation”7 in the event of a data breach where donors’ SSNs are compromised. Similarly, charitable organizations cannot be assured the IRS will maintain either the secrecy of the donors’ information,8 or that it will be able to safeguard the information from cyberattacks.9 Conclusion For the reasons discussed in this Comment, the American Legislative Exchange Council opposes the proposed additions, changes, et cetera to 26 C.F.R. § 1.170A-13 (IRS REG-138344-13) and respectfully requests that the Internal Revenue Service conduct public hearings on the matter. Respectfully, /s/ Jonathon Paul Hauenschild, Esq. Legislative Analyst American Legislative Exchange Council 7 Yakowicz “Companies Lose $400 Billion to Hackers Each Year”. 8 E.g. Westwood, Sarah, “New Documents Show Justice Department Linked to IRS Scandal”, July 8, 2015, Washington Examiner (IRS shared “more than a million pages of confidential taxpayer information with the Justice Department ahead of the 2010 midterm election in violation of laws meant to protect such data”); available at http://www.washingtonexaminer.com/new-documents-show-justice-dept.-linked-to-irs-scandal/article/2567797 (last accessed December 16, 2015). See also Wyland, Michael “IRS Exposes Confidential Taxpayer Info Again”, July 9, 2013, NonProfit Quarterly, available at https://nonprofitquarterly.org/2013/07/09/irs-exposes-confidential-taxpayer-information- yet-again/ (last accessed December 16, 2015). 9 See e.g. Weise, Elizabeth, “IRS Hack Larger than First Thought”, August 18, 2015, USA Today, available at http://www.usatoday.com/story/tech/2015/08/17/irs-hack-get-transcript/31864171/ (last accessed December 16, 2015). See also, Meyer, Robinson “There are No Rules in Love and Taxes”, August 19, 2015, The Atlantic, available at http://www.theatlantic.com/technology/archive/2015/08/there-are-no-rules-in-love-and-taxes/401765/ (last accessed December 16, 2015).