Prime Bank Ltd - Earnings Call - January 2012

•

2 likes•465 views

A careful look at the Income Statement, Balance Sheet and Statement of Cash Flows to performance a historical and current earnings and valuation analysis of a leading commercial bank in Bangladesh, Prime Bank Limited (PBL)

Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (10)

Recently uploaded

Recently uploaded (20)

Prime Bank Ltd - Earnings Call - January 2012

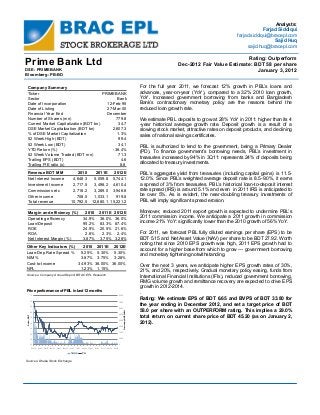

- 1. Analysts: Farjad Siddiqui farjad.siddiqui@bracepl.com Sajid Huq sajid.huq@bracepl.com For the full year 2011, we forecast 12% growth in PBL’s loans and advances, year-on-year (YoY), compared to a 32% 2010 loan growth, YoY. Increased government borrowing from banks and Bangladesh Bank’s contractionary monetary policy are the reasons behind the reduced loan growth rate. We estimate PBL deposits to grow at 28% YoY in 2011: higher than its 4 -year historical average growth rate. Deposit growth is a result of a slowing stock market, attractive rates on deposit products, and declining sales of national savings certificates. PBL is authorized to lend to the government, being a Primary Dealer (PD). To finance government’s borrowing needs, PBL’s investment in treasuries increased by 94% in 3Q11: represents 24% of deposits being allocated to treasury investments. PBL’s aggregate yield from treasuries (including capital gains) is 11.5- 12.0%. Since PBL’s weighted average deposit rate is 8.5-9.0%, it earns a spread of 3% from treasuries. PBL’s historical loan-to-deposit interest rate spread (IRS) is around 5.1% and even in 2011 IRS is anticipated to be over 5%. As is evident, the near-doubling treasury investments of PBL will imply significant spread erosion. Moreover, reduced 2011 export growth is expected to undermine PBL’s 2011 commission income. We anticipate a 2011 growth in commission income 21% YoY: significantly lower than the 2010 growth of 56% YoY. For 2011, we forecast PBL fully diluted earnings per share (EPS) to be BDT 5.15 and Net Asset Value (NAV) per share to be BDT 27.92. Worth noting that since 2010 EPS growth was high, 2011 EPS growth had to account for a higher base from which to grow — government borrowing and monetary tightening notwithstanding. Over the next 3 years, we anticipate higher EPS growth rates of 30%, 21%, and 20%, respectively. Gradual monetary policy easing, funds from International Financial Institutions (IFIs), reduced government borrowing, RMG volume growth and remittance recovery are expected to drive EPS growth in 2012-2014. . Rating: We estimate EPS of BDT 6.65 and BVPS of BDT 33.80 for the year ending in December 2012, and set a target price of BDT 58.0 per share with an OUTPERFORM rating. This implies a 29.0% total return on current share price of BDT 45.20 (as on January 2, 2012). Prime Bank Ltd DSE: PRIMEBANK Bloomberg: PB:BD Rating: Outperform Dec-2012 Fair Value Estimate: BDT 58 per share January 3, 2012 Company Summary Ticker PRIMEBANK Sector Bank Date of Incorporation 12-Feb-95 Date of Listing 27-Mar-00 Financial Year End December Number of Shares (mn) 779.8 Current Market Capitalization (BDT bn) 34.7 DSE Market Capitalization (BDT bn) 2,607.3 % of DSE Market Capitalization 1.3% 52 Week High (BDT) 99.4 52 Week Low (BDT) 34.1 YTD Return (%) -36.4% 52 Week Volume Traded (BDT mn) 71.3 Trailing EPS (BDT) 4.6 Trailing P/E ratio (x) 8.8 Revenue BDT MM 2010 2011E 2012E Net Interest Income 4,648.3 5,059.8 5,744.1 Investment Income 2,717.5 3,498.2 4,610.4 Commissions etc 2,718.2 3,289.0 3,946.8 Other income 708.5 1,033.1 919.8 Total revenue 10,792.5 12,880.1 15,221.2 Margin and efficiency (%) 2010 2011E 2012E Operating efficiency 34.9% 36.0% 36.0% Loan/Deposit 95.2% 83.3% 87.4% ROE 24.9% 20.5% 21.6% ROA 2.6% 2.3% 2.4% Net Interest Margin (%) 3.87% 3.75% 3.28% Other Key Indicators (%) 2010 2011E 2012E Loan-Dep Rate Spread % 5.25% 5.30% 5.30% NIM % 3.87% 3.75% 3.28% Cost-to-Income 34.93% 36.00% 36.00% NPL 1.23% 1.15% .0 100.0 200.0 300.0 400.0 500.0 600.0 700.0 800.0 30 35 40 45 50 55 60 65 70 75 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Oct-11 Nov-11 Dec-11 Turnover,BDTMM Price,BDT Turnover Price Sources: Company Annual Report, BRAC EPL Research Price performance of PBL in last 12 months Sources: Dhaka Stock Exchange

- 2. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 2 Growth in Loans and Advances (L&A): We expect L&A Growth Rate (GR) of 12% YoY in 2011, lower than 32.12% YoY growth in 2010, and 4-yr CAGR of 26.6% 2007-2010. L&A GR fell on spike in treasury investments as well as M2 contraction by the Bangladesh Bank (BB). Higher fiscal deficit financing (increased by 36x during the July– December 2011 YoY) will curb L&A growth for PDs such as PBL. Meanwhile, BoP pressure and increasing inflation prompted M2 contraction; BB raised repo rates multiple times and allowed large loans very selectively. Mandate to domestic private banks is to enable large loans to agriculture, SME, and export- oriented sectors, but restrict them in case of capital markets, real estate, and retail sectors. M2 GR fell from 23.5% to 19.6% during March-Sep11, nearing BB’s FY12 year- end target of 18%. We anticipate an M2 GR lower than BB-target, as BB tries to mitigate the inflationary effect of a BoP deficit and FX depreciation. Government borrowing is likely to drop in 1H12 with its impact becoming clearer in 2H12—on upward revision of energy prices. Figure 1: PBL L&A Growth Figure 2: PBL L&A Composition Sources: Company Annual Report, BRAC EPL Research Sources: Company Annual Report (As on 4Q10) Retail Loan, 8.36% SMELoan, 5.18% Corporate Loan, 84.86% Staff Loan, 1.13% Credit Card, 0.47% 28% 31% 19% 32% 12% 30% 25% 0% 5% 10% 15% 20% 25% 30% 35% 0 50,000 100,000 150,000 200,000 250,000 2007 2008 2009 2010 2011E 2012E 2013E L&AGR L&A(BDTMM) L & A (BDT MM) L & A GR (YoY)

- 3. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 3 Deposit growth and loan-to-deposit ratio (LDR): We anticipate a 28% YoY deposit growth in 2011, higher than 16.6% YoY in 2010, and 20.7% 4-year CAGR. From the demand viewpoint, deposits grew on attractive bank rates, 44% stock market correction, and declining savings certificate sales. From the supply end, deposit mobilization was stepped up to meet PD-mandate of financing government borrowing needs. Further, we estimate an LDR of 80% in 2011, far lower than 2010 LDR of 95%. This was likely to happen because of 2010’s historically high L&A GR; further precipitated by monetary tightening and government borrowing. As such—a projected 80% LDR—85% being the LDR upper-limit expected of PDs is testimony to PBL’s enduring return on equity (also keeping record deposit mobilization in mind). Figure 3: PBL Deposits Composition and GR Sources: Company Annual Report, BRAC EPL Research 70% 75% 80% 85% 90% 95% 100% 2007 2008 2009 2010 2011E 2012E 2013E LDR LDR Figure 4: PBL Loan-Deposit Ratio (LDR) Sources: Company Annual Report, BRAC EPL Research 29% 25% 22% 17% 28% 24% 24% 0% 5% 10% 15% 20% 25% 30% 35% 50,000 100,000 150,000 200,000 250,000 300,000 2007 2008 2009 2010 2011F2012F2013F DepositsGR Deposits(BDTMM) Current Deposits and other accounts Bills payable Savings bank Deposits Fixed Deposits Deposit Growth Rate

- 4. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 4 Net Interest Income (NII) Given L&A estimates and deposit outlook—we project 2011 NII GR of 8.85% YoY—dropping from that of 2010’s 89.5%, and 4-year CAGR of 21.8%. 2011 NIM should also decline to 3.75% from 3.9% in 2010. This was driven by loan diversion on account of high government borrowing. Non-Interest Income Non-interest income constitutes 61.6% of PBL’s expected 2011 EPS. As per 4- year average, its proportion rises to 63.5% of Total Operating Income, with investment income at 30.7% and commissions & fees income at 24.3%. Given that IRS and NIMs decline over time, PBL’s earnings drivers are diversified. Estimated 2011 non-interest income comprises 60% of Total Operating Income. Figure 5: PBL Net Interest Margin (NIM) Figure 6: PBL Interest Rate Spread and Inflation Sources: Company Annual Report, BRAC EPL Research 3.2% 3.2% 2.5% 2.7% 3.9% 3.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 2006 2007 2008 2009 2010 2011E NIM(%) InterestIncome(BDTMM) Interest Income NIM Figure 7: PBL Interest Income & NIM Sources: Company Annual Report, BRAC EPL Research 10% 7% 7% 9% 10% 7% 7% 0% 2% 4% 6% 8% 10% 12% 4.4% 4.5% 4.6% 4.7% 4.8% 4.9% 5.0% 5.1% 5.2% 5.3% 5.4% AvgInflationRate InterestRateSpread Interest Rate Spread Average Inflation Rate 0% 1% 1% 2% 2% 3% 3% 4% 4% 5% NIM NIM

- 5. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 5 We expect 2011 investment income to grow by 28.7% YoY, vs. -19.4% YoY in 2010. In 9M11, treasury earnings rose on 91% higher treasury investments (equaling 23% of total deposits). For 2011, we estimate 85% higher treasury investments YoY. Meanwhile, 2011 portfolio investments income (mainly dividend income) is expected to grow by 47% YoY from its lower base of 2010. In contrast, portfolio income declined by 75% in 2010 YoY. This is on account of decline in trading profit of portfolio shares. Figure 8: Comparison of Operating Income Composition Source: BRAC EPL Research (As on 2011 E) - 5,000 10,000 15,000 20,000 2007 2008 2009 2010 2011E 2012E 2013E NonInterestIncome(BDTMM) Net Interest Income Income from investmentsin securities/Shares Commission, Exchange &Brokerage Other Income Figure 9: PBL Operating Income Composition Sources: Company Annual Report, BRAC EPL Research 36% 40% 68% 43% 35% 29% 32% 24% 1% 24% 38% 42% 26% 18% 28% 28% 22% 23% 6% 18% 3% 6% 5% 6% 0% 20% 40% 60% 80% 100% Prime Bank National Bank Islami Bank Bangladesh Eastern Bank NCC Bank Southeast Bank Net interest Income Investment Income Fee Income Other Income

- 6. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 6 Moreover, we estimate 2011 commission income GR of 21% YoY, compared to 2010 GR of 51.67% YoY. The slower growth can be attributable to crowding out effect of government borrowing which reduces trade financing, slower export GR YoY, and dried up income from Merchant Bank Subsidiary. Higher cost-to-income ratio in comparison to historical average PBL has maintained an average cost-to-income ratio of 34% in 2007-2010. We expect the cost-to-income ratio to reach 36% by 2013-end. Higher costs are expected to emerge from an increased focus on human capital development, e.g. training, increments in salary and benefits, etc. 18% 26% 19% 16% 23% 20% 18% 0% 5% 10% 15% 20% 25% 30% 0 10,000 20,000 30,000 40,000 50,000 2007 2008 2009 2010 2011E 2012E 2013E InvestmenttoTotalDeposit InvestmentinTreasury(BDT MM) Investment in Treasury (BDTMM) Ratio of Investment to TotalDeposit Figure 11: PBL Commission & Fees Income Growth Sources: Company Annual Report, BRAC EPL Research Figure 10: PBL Investment in Treasury Sources: Company Annual Report, BRAC EPL Research 21% 21% 22% 52% 21% 20% 20% 0% 10% 20% 30% 40% 50% 60% - 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 2007 2008 2009 2010 2011E 2012E 2013E FeesIncomeGR(%) FeesIncome(BDTMM) Commission and Fees income (BDT MM) GR

- 7. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 7 Projected EPS growth amid macro shocks We estimate EPS of BDT5.15 for the full financial year of 2011, 10.3% higher YoY, against 24.5% YoY EPS GR in 2010. Four-year average EPS GR is 45.4% as of 2010. Year 2011 has been severe on the bank sector. High inflation and government borrowing cut spread income, whereas a 44% stock market correction eroded 2010 portfolio gains. Moreover, trade finance commissions are expected to fall on slowdown in Euro-zone demand. PBL’s projected EPS on a three-year horizon is as follows: A relatively lower 2011 EPS should enable a higher 2012 EPS growth rate. Moreover, macroeconomic fundamentals such as inflation rate and currency risks are expected to ease in 2012, on energy price revisions, lower government borrowing, and BoP support from the IMF. We forecast a 30% YoY growth rate for EPS by end of 2012. 2.0% 2.1% 2.2% 2.3% 2.4% 2.5% 2.6% 2.7% 2.8% 30% 31% 32% 33% 34% 35% 36% 37% 2007 2008 2009 2010 2011E 2012E 2013E CosttoAssets(%) CosttoIncome(%) Cost to Income Cost to Assets Figure 12: PBL Operating Efficiency Ratio Sources: Company Annual Report, BRAC EPL Research Figure 13: PBL EPS (Fully Diluted) Sources: Company Annual Report, BRAC EPL Research 1.79 1.60 3.75 4.67 5.15 6.65 8.05 0 2 4 6 8 10 2007 2008 2009 2010 2011E 2012E 2013E EPS(BDT) EPS(BDT)

- 8. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 8 Diverse Earnings Drivers to limit downside on Macro Shocks Below graphs indicate treasury investments GR to NII correlation coefficient (CC) of -0.7 vs. inflation to NII correlation of -0.02. Government borrowing more than inflation cut NII in 4Q11. Meanwhile, inflation to non-interest income CC is 0.17 vs. treasury to non-interest income CC of 0.03. The low CC between treasury investments GR and non-interest income bears out our thesis that PBL’s diversified earnings drivers protected their potential downside on high government borrowing. . Figure 14: Inflation and PBL Net Interest Income & Non Interest Income GR Sources: Company Annual Report, BRAC EPL Research Figure 15: PBL Treasury Investment, Net Interest Income & Non Interest Income GR 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% -20% 0% 20% 40% 60% 80% 100% 2007 2008 2009 2010 2011 NIIGR&NonInterestIncomeGR TreasuryIncomeGR GR in TreasuryInvestments GR in Net Interest Income GR in Non Interest Income Sources: Company Annual Report, BRAC EPL Research 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% -20% -15% -10% -5% 0% 5% 10% 2007 2008 2009 2010 2011 NIIGR&NonInterestIncomeGR Inflation(YoY) Inflation (YoY) GR in Net Interest Income GR in Non Interest Income

- 9. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 9 Comfortable capital adequacy ratio and relatively high asset quality The table below shows the capital adequacy positions of Prime Bank in 2009 and 2010. The minimum capital adequacy ratio prescribed by Bangladesh Bank is 5% for Tier-I and 10% for total capital. As on 4Q10, PBL exceeds these minimum ratio thresholds with a Tier-I capital ratio of 8.6% and total capital ratio of 11.7%. One of PBL’s key managerial strengths lies in its capacity to maintain below industry-average NPL ratios. In 2010, NPL ratio was 1.23% in comparison to 1.29% in 2009. In 2010, aggregate loans and advances increased 32.1%, while classified loans and advances decreased by 19%. We forecast an NPL ratio of 1.15% for 2011, a 6.5% decrease YoY. Table 1: Capital Position BDT MM Capital Adequacy Ratio (CAR) 2009 2010 Tier I 9,057 15,793 Tier II 3,112 5,692 Total Capital 12,169 21,485 Total Assets including Off Bal Sheet 169,910 242,832 Total Risk Weighted Assets 82,710 183,747 Required Ratio 10% 10% Required Capital 8,271 18,375 Surplus 3,898 3,110 CAR 9.81% 11.69% Source: Company Annual Report 9.50% 8.67% 10.95% 8.60% 2.00% 2.21% 3.76% 3.09% 0% 2% 4% 6% 8% 10% 12% 14% 16% 2007 2008 2009 2010 TierI&TierIICapital Tier I Tier II Source: Company Annual Report Figure 16: PBL Tier I & Tier II Capital

- 10. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 10 Relatively lower profitability We estimate PBL’s Return on Equity (ROE) and Return on Assets (ROA) at 20.5% and 2.3%, respectively, for 2011. Corresponding ratios for 2010 are 24.3% and 2.5%. Declining profitability is a result of the squeezed LDR, interest rate spread & NIM, relatively lower net yield from treasury investments, a stock market correction, and relatively lower commission income growth. However, we expect both ROE and ROA to improve in 2012. PBL in comparison to leading frontier market banks A quick look at the largest listed banks in frontier markets such as Vietnam, Sri Lanka, and Nigeria indicates how PBL fares in relation to its frontier market peers. Table 2: Asset Quality Asset Quality 2009 2010 NPLs to Total Loans and Advances 1.29% 1.23% Provision for Classified Loans, BDT MM 631 642 Source: Company Annual Report 30.7% 20.9% 31.6% 24.9% 20.5% 21.6% 21.4% 2.0% 1.3% 2.5% 2.6% 2.3% 2.3% 2.3% 0% 5% 10% 15% 20% 25% 30% 35% 2007 2008 2009 2010 2011E 2012E 2013E ROE&ROA ROE ROA Figure 17: PBL ROE & ROA Sources: Company Annual Report, BRAC EPL Research Table 3: Comparative Analysis of Frontier Market Banks Frontier Market Banks Country MCAP (USD MM) P/E P/B ROE ROA Prime Bank Ltd Bangladesh 414.89 10.20x 1.80x 19.17% 2.13% Vietcom Bank Vietnam 1,930.90 9.95x 1.71x 22.20% 1.50% Vietnam Joint Stock Commercial Bank For Industry And Trade Vietnam 1,387.79 9.83x 1.87x 16.80% 1.10% Commercial Bank of Ceylon PLC Sri Lanka 705.04 11.66x 2.07x 21.00% 2.00% Hatton National Bank PLC Sri Lanka 469.07 12.55x 1.89x 17.20% 1.70% First Bank of Nigeria PLC Nigeria 1,648.18 10.30x 0.90x 12.90% 1.50% Sources: BRAC EPL Research, Capital IQ (As on Dec 31, 2011)

- 11. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 11 PBL has lower P/E and P/B ratios than the median P/E and P/B ratios for the above six banks. PBL P/E (10.20x) is lower than the median P/E (10.25x), while PBL P/B (1.80x) is lower than the median P/B (1.84x). Profitability ratios RoE and RoA however are lower PBL than the median of the above group. Lower valuation multiples than the median but lower profitability ratios as well indicates markets’ consensus to reward higher profitability with higher price multiples and vice versa. Our rating and target price Considering the estimated EPS of BDT 6.65 and BVPS of BDT 33.80 for the year ending December 2012, we set a target price of BDT 58.0 per share with an OUTPERFORM rating. This implies 29% total return on the current share price of BDT 45.20 (as on 2nd January 2012). Prime Bank (Bangladesh) Vietcom Bank (Vietnam) Vietnam Joint Stock Bank (Vietnam) Commercial Bank of Ceylon (Sri Lanka) First Bank of Nigeria (Nigeria) 10% 12% 14% 16% 18% 20% 22% 24% 26% 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 ROE(%) ROA (%) (Size of bubble represents Volume/MCAP) Figure 18: Comparative Analysis of Volume to MCAP Sources: BRAC EPL Research, Capital IQ (As on Dec 31, 2011)

- 12. Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) 12 Balance Sheet, MM BDT 2008 2009 2010 2011E 2012E 2013E Property & Assets: Cash 7,199.9 10,252.3 9,576.9 16,746.2 17,447.0 25,184.2 Balance with Other Banks & F.I 2,042.6 833.9 1,397.0 1,746.2 1,833.5 1,925.2 Money at call .0 .0 .0 .0 .0 .0 Investment 23,103.1 19,933.9 22,198.5 39,779.6 41,888.9 46,013.2 Loan & Advance 75,602.5 89,946.0 118,837.3 133,097.8 173,027.1 216,283.9 Fixed Assets 1,380.1 1,577.9 1,743.7 4,010.4 5,614.6 6,176.0 Other Assets 1,188.5 2,440.8 1,779.5 2,580.2 3,612.3 4,154.1 Total Assets 110,516.6 124,984.7 155,532.8 197,960.5 243,423.3 299,736.7 Liabilities & Equities: Liabilities: Borrowing from other banks, F.I 11,397.9 86.5 5,214.5 6,778.8 7,456.7 7,829.6 Deposits 88,083.1 107,077.3 124,799.3 159,743.1 198,081.5 245,621.0 Other Liability 4,327.4 6,024.2 8,052.4 9,662.9 11,595.4 13,914.5 Total Liabilities 103,808.4 113,188.0 138,066.2 176,184.8 217,133.6 267,365.1 Shareholder's Equity: 6,708.2 11,796.7 17,466.6 21,775.7 26,289.7 32,371.6 Total Liabilities & Equities 110,516.6 124,984.7 155,532.8 197,960.5 243,423.3 299,736.7 Income Statement, MM BDT 2008 2009 2010 2011E 2012E 2013E Interest/Investment Income 9,107.9 10,881.2 12,695.4 17,217.8 20,440.5 25,549.5 Interest/profit paid on deposit 7,129.6 8,428.7 8,047.1 12,158.0 14,696.4 18,121.7 Net Interest Income 1,978.3 2,452.5 4,648.3 5,059.8 5,744.1 7,427.8 Income from investments 1,743.7 3,372.5 2,717.5 3,498.2 4,610.4 4,961.3 Commission, Excng & Brok 1,469.0 1,792.2 2,718.2 3,289.0 3,946.8 4,736.2 Other Income 628.3 673.8 708.5 1,033.1 919.8 957.9 Total Operating Income 5,819.2 8,290.9 10,792.5 12,880.1 15,221.2 18,083.2 Operating Expense 1,954.9 2,934.1 3,769.7 4,636.8 5,479.6 6,510.0 Profit Before Provision 3,864.4 5,356.8 7,022.8 8,243.3 9,741.6 11,573.3 Provision 1,383.5 624.0 551.0 1,184.6 951.6 937.2 Pre-Tax Profit 2,480.9 4,732.8 6,471.7 7,058.7 8,789.9 10,636.1 Tax 1,231.9 1,805.8 2,829.1 3,042.3 3,603.9 4,355.5 Profit After Tax 1,249.0 2,927.0 3,642.7 4,016.4 5,186.0 6,280.6 2008 2009 2010 2011E 2012E 2013E Total Assets Growth 48.95% 13.09% 24.44% 48.95% 48.95% 48.95% L & A Growth 30.84% 18.97% 32.12% 12.00% 30.00% 25.00% Deposit Growth 24.86% 21.56% 16.55% 28.00% 24.00% 24.00% EPS GR -10.71% 134.35% 24.45% 10.26% 29.12% 21.11%

- 13. IMPORTANT DISCLOSURES Analyst Certification: Each research analyst and research associate who authored this document and whose name appears herein certifies that the recommendations and opinions expressed in the research report accurately reflect their personal views about any and all of the securities or issuers discussed therein that are within the coverage universe. Disclaimer: Estimates and projections herein are our own and are based on assumptions that we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation of the purchase or sale of any security. As it acts for public companies from time to time, BRAC-EPL may have a relationship with the above mentioned company(s). This report is intended for distribution in only those jurisdictions in which BRAC-EPL is registered and any distribution outside those jurisdictions is strictly prohibited. Compensation of Analysts: The compensation of research analysts is intended to reflect the value of the services they provide to the clients of BRAC-EPL. As with most other employees, the compensation of research analysts is impacted by the overall profitability of the firm, which may include revenues from corporate finance activities of the firm's Corporate Finance department. However, Research analysts' compensation is not directly related to specific corporate finance transaction. General Risk Factors: BRAC-EPL will conduct a comprehensive risk assessment for each company under coverage at the time of initiating research coverage and also revisit this assessment when subsequent update reports are published or material company events occur. Following are some general risks that can impact future operational and financial performance: (1) Industry fundamentals with respect to customer demand or product / service pricing could change expected revenues and earnings; (2) Issues relating to major competitors or market shares or new product expectations could change investor attitudes; (3) Unforeseen developments with respect to the management, financial condition or accounting policies alter the prospective valuation; or (4) Interest rates, currency or major segments of the economy could alter investor confidence and investment prospects. BRAC EPL Stock Brokerage Capital Markets Group Sajid Huq Amit Senior Research Analyst sajid.huq@bracepl.com 01755 541 254 Parvez Morshed Chowdhury Research Analyst parvez@bracepl.com 01730 357 154 Ali Imam Investment Analyst imam@bracepl.com 01730 357 153 Khandakar Safwan Saad Research Associate safwan@bracepl.com 01730 357 779 Aasim Tajwaar Matin Research Associate tajwaar.matin@bracepl.com 01730 727 913 M M Shahnewaz Kabir Shawon Research Associate shahnewaz@bracepl.com 01730 727 918 Farjad Siddiqui Research Associate farjad.siddiqui@bracepl.com 01730 727 924 BRAC EPL Research www.bracepl.com 121/B Gulshan Avenue Gulshan-2, Dhaka-1212 Tel: +88 02 881 9421-5 Fax: +88 02 881 9426 E-Mail: research@bracepl.com Prime Bank Ltd (DSE: PRIMEBANK; Bloomberg: PB:BD) Institutional Sales and Trading Delwar Hussain (Del) Head of Institutional Sales and Trading del.hussain@bracepl.com 01755 541 252