2. 1

A. Executive Summary

Market Opportunity: The size of the online grocery market is estimated at $7,066,328,882. This is a

viable opportunity for Amazon. Adoption rate is the most influential variable and the most challenging to

predict because this service disrupts current consumer shopping behaviors.

Industry Profitability: Profitability in the online grocery space is low to medium. Competitive rivalry

and bargaining power of buyers are high due to a variety of substitutes including traditional grocers. The

grocery industry maintains very low profit margins, which is a significant challenge for new entrants.

Customer Analysis: Consumers have begun to transition their shopping behaviors to online platforms.

Increasingly time-pressed customers appreciate flexibility and convenience. Despite these trends, online

grocery is still not preferred. Consumer habits will be difficult to alter.

Competitive Analysis: Amazon Fresh would compete with a variety of firms that operate with several

different models. Its top competitors include Peapod, FreshDirect, Walmart, Instacart and traditional

grocers such as Safeway. Walmart and Instacart represent the greatest threats based on price, delivery

speed and product selection.

Company Analysis: Amazon’s distinct competency is operational excellence. Its large scale and efficient

distribution model for retailing hard goods is difficult to replicate, but many of these advantages will be

difficult to translate due to the unique nature of handling fresh and perishable food items.

Objectives: The total number of customers, which is determined by consumer adoption rates, is a primary

driver of revenue. The total number of service areas has important implications for both revenue and cost.

Operating margin is a key outcome measure. Profitability must be obtained by Year 5.

Year 1 Year 5

Total # of Customers 26,000 690,000

# of Service Areas 2 13

Operating Margin -7.00% 3.00%

Target Markets: 1) Households with two working parents, 2) high income singles, 3) households

without a vehicle and 4) consumers that prefer online shopping. The first two segments are most attractive

with respect to their profitability, size, fit and accessibility.

Value Proposition: The main benefits this service provides are convenience and efficiency from saving

some of the time, money and hassle associated with traditional grocery shopping. These benefits will

outweigh the costs (price, switching costs, risk, etc.) for the targeted consumers.

Distinct Competency: Amazon’s operational excellence has allowed it to win in several retail categories.

Although many of its warehousing and technological advantages are sustainable, the intricacies of

handling and delivering fresh foods require different capabilities that several other firms can develop

quickly.

Positioning: For busy consumers, Amazon Fresh is the most convenient way to shop among all grocery

providers because same-day home delivery saves you precious time, money and energy.

Marketing Mix: A skim approach to market will be supported by a differentiated product offering,

premium price structure, trial-inducing promotions and slow market entry.

Financial Analysis:

Year 1 Year 2 Year 3 Year 4 Year 5

Revenue $35,591,400.00 $100,977,880.39 $233,930,008.92 $579,519,585.83 $1,256,162,867.72

Var. Costs $31,688,434.44 $88,367,906.01 $201,225,006.78 $490,005,818.94 $1,044,047,849.87

Fixed Costs $6,515,054.00 $15,812,456.24 $35,171,601.07 $81,939,948.23 $175,201,172.80

Income -$2,612,088.44 -$3,202,481.87 -$2,466,598.9 $7,573,818.7 $36,913,845.0

Operating margin at maturity will approach 3.12% per transaction.

Conclusion: Amazon Fresh should proceed with caution and continuously reassess this opportunity.

3. 2

B. Situation Analysis

Market Opportunity

The online grocery opportunity is attractive due to the $568 billion size of the food retail market.

There is consumer need for a grocery provider that can reduce the amount of time and hassle involved in

visiting a traditional food retailer. 24/7 online ordering from a wide selection of grocery and other items

and home delivery provide convenience for increasingly busy consumers. The challenge for companies in

this space is to convince consumers to move their grocery shopping habits online. Many consumers are

hesitant to do so for fear of low product quality and an unwillingness to plan an order or wait for delivery.

Therefore, another unsolved need is risk reduction and assurance that the process will work for them.

Amazon Fresh has the ability to alleviate some of these apprehensions by targeting the right consumers

and leveraging the strength of the Amazon brand.

Market Size

A market size estimate over $7 billion indicates that this is a viable opportunity for Amazon.

However, this number reflects several assumptions with high levels of uncertainty. Adoption rate, order

frequency and average dollar amount per transaction are especially difficult to predict, but ideally,

pessimistic and optimistic assumptions have balanced each other out to produce a realistic forecast.

Population (# of U.S. Households) 117,538,000

Exclusions:

Rural Population 17,630,700

No Internet Access 2,350,760

Addressable Population 97,556,540

% Population % Adopt Frequency/Year Average $ / Trans.

Two Working Parents 13.25% 9% 30 99.00$ $3,455,184,366.32

No Vehicle Urbanites 9.29% 10% 28 78.00$ $1,979,359,760

Online Shoppers 25.00% 6% 24 69.00$ $58,392,878.40

High Income Singles 10.00% 8% 28 72.00$ $1,573,391,877.12

Estimated Market Size 7,066,328,882.25$

Assumptions:

2.6 people per household

Approximately 15% of U.S. households are in rural counties

Approximately 2% of U.S. households do not have Internet access

Approximately 14,921,568 U.S. households are married couples with children where both parents work

50% of the population has shopped online more than once. Half of those people shop online regularly.

Average $/Transaction is based on Peapod data/consumer behavior at traditional grocers

4. 3

For example, working couple with children households tend to visit traditional grocery stores 2-3

times per week. If these households migrated the majority of their grocery shopping online, average

frequency would likely be greater than 30 deliveries/year. Also, many of these assumptions are based on

today’s consumer environment, which will change drastically in a short period of time as Millennials

enter the workforce and increase their incomes. The dollar amounts per transaction appear to be overly

optimistic, but they were determined based on data from Peapod’s first few years of operation.

This exercise suggests that low adoption rates will be the biggest obstacle for Amazon Fresh. The

market segments that will find this service attractive are growing, but the disruptive behavioral changes

required of consumers create a barrier to profitability. These observations indicate that Amazon Fresh

should take a highly focused, niche approach to market entry until this model reaches a tipping point in

the mainstream population.

5. 4

Industry Profitability: Online Grocery

Force Level Effect on Exp. Profit

Threat of New Entrants Medium Medium

Intensity of Competitive Rivalry High Low

Threat of Substitute Products/Services Medium Medium

Bargaining Power of Buyers High Low

Bargaining Power of Suppliers Low High

Threat of New Entrants: The capital required to start an online grocery company only involves the

internet/e-commerce technology infrastructure, inventory, transportation and storage space. Barriers to

entry are increasing due to the rapid rate of technological change (especially within mobile) and

increasing federal regulations on food sale/shipment and e-commerce security. These factors will increase

operating costs and may prohibit smaller firms from entering.

Intensity of Competitive Rivalry: Competition in this industry is high and increasing. Currently, firms

primarily compete on the size of their customer base, regional presence, product variety, ability to offer

attractive deals and brand recognition. Also, consumers can easily compare prices across websites. This

forces retailers to offer discounts, promotions and loyalty programs on both products and delivery fees to

win business. In addition, firms in this space compete with physical food retailers. Although online

purchases of household items and packaged goods are expected to grow, many consumers still prefer to

shop for groceries at brick-and-mortar stores.

Threat of Substitute Products/Services: Every consumer must regularly purchase food, so the threat of

substitute products is limited unless a specific brand (i.e. private label) is offered in physical stores but not

by online grocers. The threat of substitute services is more substantial with the recent proliferation of

grocery models. In addition to shopping at traditional retailers, consumers can utilize personal shoppers or

online ordering for pick-up at physical locations.

Bargaining Power of Buyers: Consumers have a multitude of options for purchasing groceries. Almost

every retail format (supermarkets, mass merchandisers, club stores, discounters, etc.) sells some

assortment of grocery products. In addition, consumers use the Internet and mobile devices to price

discover and chase deals. Low switching costs increase competitive rivalry and squeeze industry margins.

6. 5

Bargaining Power of Suppliers: Online grocers must secure the support of grocery product

manufacturers to be successful in this industry. As both traditional retailers and e-tailers have grown their

unit and dollar sales, their power within the supply chain has increased accordingly. Online grocery

services, many of which were developed by the biggest retail players, will share in the benefits of high

price negotiating power, especially as their sales volumes increase.

Industry Margins:

The traditional grocery industry maintains extremely low profit margins. The industry standard

margin hovers around 1%. This presents a significant challenge for online grocers like Amazon Fresh

since high overhead costs for developing a grocery warehouse and delivery network will reduce initial

profitability. Peapod has struggled to turn a profit for most of its existence. It just recently started to make

money due to supply chain efficiencies, population density and its connection to brick and mortar stores.

The above analysis suggests that the online grocery industry has limited profit potential. Low

profit margins in the grocery industry will be squeezed further by the high investment required to

establish the necessary infrastructure. Amazon Fresh is not likely to be profitable in its first few years of

operation unless grocery delivery drives the sale of other high margin products for delivery at the same

time.

7. 6

Customer Analysis

Consumers will continue to transition their shopping behavior to online and mobile platforms. As

Millennials enter the scene and e-commerce technologies become even more user-friendly, the line

between the physical and digital world will continue to blur and increasingly time-pressed consumers will

expect 24/7 access to all shopping categories. Increasing mobile device ownership and app use and the

growing popularity of online shopping and social media has changed the way consumers cook and eat

food, and there is an opportunity to change the way they buy food too. Online grocery use is most popular

in households where both parents work, which highlights a consumer need for time savings and do-it-for-

me solutions. This is a need that Amazon Fresh can solve with one-stop shopping and quick delivery.

That being said, this industry has been limited by several consumer factors. Online grocery is still

not preferred, mostly due to limited experience with the model. Many consumers still appreciate the

ability to select their own fresh foods, especially in the produce department. Consumers who shop online

for groceries typically only do so when normal routines are interrupted. Furthermore, consumers might be

put-off by delivery fees as free shipping becomes an expectation with digital shopping. For these reasons,

online grocery service will be adopted slowly before it gains mass market appeal.

Growth in this industry will be driven by breaking the habit of spontaneous, in-store shopping and

helping consumers use the online grocery channel when their situation calls for it. That being said, a

complete shift from the physical channel to the digital channel is not required for online grocery to be

profitable. Consumers who have already adopted the online grocery model tend to shop in both channels

for greatest flexibility.1

Amazon Fresh can create value by using the online channel to provide a service

that conveniently fits into the evolving lifestyles of consumers.

1

"Amazon Fresh...Grocery Domination Ahead?" The Hartman Group. Feb. 2007. Web. 29 Nov. 2014.

http://www.hartman-group.com/hartbeat/amazonfresh-grocery-domination-ahead

8. 7

Competitive Analysis

Amazon Fresh competes directly with firms that use a warehouse to home business model, but it

also competes with traditional grocers and firms that have developed “substitute” approaches to online

grocery:

Warehouse to Home: FreshDirect has a strong presence on the East Coast1

. It targets working mothers

that benefit from the convenience of 24/7 online ordering and next day home delivery. The firm focuses

on operational excellence by continuously expanding its truck network and warehousing capabilities to

minimize cost per order. It offers local, gourmet and specialty products in addition to common brands to

urban consumers, but its selection and delivery speed is constrained by its centralized distribution model.

Peapod serves 13 East Coast and Midwest states. It targets busy families/singles and tech-savvy

shoppers. Its prices are slightly below FreshDirect2

. Peapod’s advantage lies within its climate-controlled

warehouses and partnerships with two brick-and-mortar retail chains, a physical infrastructure that is

difficult to replicate in the short-term. Peapod has the most user-friendly website and mobile app due to

its recent inventments in engineering talent, but competing firms can quickly imitate its digital strategies.

Store to Home: Walmart is the #1 food retailer with more than 4000 stores located within 5 miles of 2/3

the U.S. population. Its strategy is to treat its stores like distribution centers and provide same or next day

home delivery to local customers at low cost. Its national physical presence and experience with sourcing

and handling grocery products are highly advantageous, but it currently lacks the IT infastructure needed

for large-scale execution. Walmart is focused on repairing this disadvantage, so it is only temporary.

Prices are the same as in-store plus a $5-10 delivery fee. Free order pick-up is also available at stores, so

customers have a variety of shopping options to choose from.

Personal Shoppers: Instacart provides home delivery from several retailers including Whole Foods,

Costco and Safeway in 6 cities. It targets consumers who are willing to pay a premium price for delivery

within 2 hours. Instacart’s main advantage is its low overhead costs because no warehouse system is

required, but this model creates few barriers to entry for firms that might copy this model. It also has less

9. 8

control over service quality since its ‘shoppers’ are essentially self-motivated contract workers. These

shoppers also represent a high labor cost. Instacart has yet to establish a sustainable distinct competency,

but the firm recently received $44 million in venture capital.

Traditional Grocers: The majority of consumers still buy their groceries at brick-and-mortar retail

locations. In a 2014 survey of 1250 consumers, only 9% expressed a preference for online grocery

shopping3

. Many people prefer to select their own fresh foods, and others are turned off by the fees and

wait times involved with home delivery. Like Wal-Mart, traditional grocers have the advantage of an

established store network that can be leveraged if they choose to enter the online space. For example,

Safeway, the second largest supermarket chain in the U.S., now offers shipping services from 6am-10pm.

10. 9

The four attributes in these diagrams were selected because of their strong relationship with

customer experience. The firms that maximize consumer convenience by offering the most products, the

lowest prices, the quickest deliveries and the easiest order process will win.

Walmart and Instacart are Amazon Fresh’s greatest threats. Walmart’s store network represents a

physical proximity to consumers that is unmatched. Once Walmart discovers how to turn its stores into

pick and pack hubs, it will be in a position to rapidly enter new markets. Its customers will be able to

choose whether they want delivery, pick-up or the traditional store experience. Furthermore, Walmart can

provide a similar basket of low-priced goods. Instacart’s model is highly scaleable because warehouses or

stores are not required. Plus, they are able to deliver a broad selection of goods from third party retailers

within two hours of order—the lowest response time in the industry. Instacart demands a premium price

for this service, so Amazon can differentiate itself by offering a lower cost solution from a better known

brand.

11. 10

Company Analysis

Amazon sells millions of items such as books, electronics and home furnishings directly to

consumers through its website. In the last five years, Amazon has grown from a $15 billion company to a

$61 billion company. As of May 2014, Amazon had a total active user base of 244 million with 30

million new customers in 2013. Amazon has an opportunity to leverage its large customer base, especially

its loyal Prime members, to grow the grocery venture.

Amazon wins in the highly competitive retail space due to its operational excellence. Its large

scale, efficient distribution model and brick-and-mortar footprint are difficult to replicate. It has stayed on

top by offering customers the lowest prices among competitors such as Wal-mart and Best Buy while

charging little to nothing for shipping. Also, Amazon has demonstrated a willingness to sacrifice short-

term profits in order to achieve long-term goals. This strategy is consistent with the low-margin Amazon

Fresh venture.

Amazon has spent more than $1.4 billion in acquisitions over the past two years, which includes

the $678 million it spent on Kiva systems, a warehouse technology company. In line with its cost-cutting

strategy, Amazon’s recent focus has been on improving its automated fulfillment systems at the

warehouse level, reducing processing times and decreasing personnel expenses. Efficiencies in this area

will provide some advantages for grocery warehousing, but handling fresh and perishable food items

requires a more expensive labor base and skill set than Amazon currently possesses.

Amazon has a strong advantage in this space because it can offer over 500,000 other products for

delivery at the same time to make up for razor thin margins on grocery products. Therefore, the high

investment required to develop the infrastructure to source, warehouse and deliver perishable products

could be offset by more frequent orders and high customer density. This is an advantage that other

grocery firms could not replicate as easily.

Most likely, Amazon Fresh will utilize company-owned and operated trucks to delivery fresh

foods. This could make returns more efficient and allow a faster response time to customer orders, but it

will take a substantial amount of time and money to build this network. Also, refrigerated areas will have

12. 11

to be added to current warehouses and/or built into the design of new warehouses. These physical

considerations will limit Amazon’s speed to new markets.

Amazon has an existing presence in over 40 urban markets and same-day delivery operations in

13 of them. It has also gained experience in packaged food retailing through its Pantry service. Customers

in 48 states can fill up a 45lb. box and have it shipped to their door in two days for a flat rate of $5.99.

Although Amazon’s distinct competencies in fulfillment efficiency and service speed will benefit

Amazon Fresh, the grocery space represents a significant amount of uncharted territory. Some of their go-

to-market challenges will include pricing strategies, infrastructure costs, staffing complexities and

customer experience management. These decision areas remain outside of Amazon’s current strength set.2

2

"Amazon.com, Inc." Hoovers, 2014. Web. 29 Nov. 2014.

http://subscriber.hoovers.com.ezp2.lib.umn.edu/H/company360/overview.html?companyId=51493000000000

13. 12

C. Marketing Strategy

Objectives

Year 1 Year 5

Total # of Customers 26,000 690,000

# of Service Areas 2 13

Operating Margin (Year 5) -7.00% 3.00%

These three objectives were informed by the financial projections for this venture. According to a

sensitivity analysis (see appendix), the number of Year 1 customers in any given area is one of the most

influential variables on revenue. Therefore, a significant amount of marketing effort must be applied in

new service areas to ensure sufficient consumer adoption and growth. A skim approach, as described in

the marketing mix below, should be employed to ensure that consumers who highly value this service are

effectively targeted.

The total number of service areas and the rate at which service areas are added have important

implications for Amazon Fresh. A “big bang” approach is not recommended, but at least thirteen urban

markets should be entered by Year 5 to capture cost efficiencies through increased scale. These

efficiencies are required to achieve profitability. Also, the slow but consistent addition of service areas

will enable steady growth in the customer base, which is key to generating sufficient revenue and

accelerating adoption rates through word of mouth and imitation.

Operating margin is the most important performance indicator. Profitability must be established

by Year 5 to justify this venture. According to another sensitivity analysis, low order amounts, cost of

goods sold, overhead expenses and delivery cost per order are some of the items that could keep Amazon

Fresh from reaching this target. Therefore, these are the variables that must be diligently monitored and

controlled as the model is revised and expanded.

14. 13

Target Markets

Two Working Parents: According to the Bureau of Labor Statistics, the share of married-couple families

with children where both parents work has seen steady growth in recent years, and this trend is likely to

continue. Approximately 14,921,568 households fall into this category. These are time-starved consumers

that place a high value on convenience and do-it-for-me services. Amazon Fresh provides a great solution

for them because 24/7 ordering and quick home delivery saves them the time and hassle involved with

regular store visits. Plus, families with children typically spend more than $10,000 annually at

supermarkets. This suggests a larger average order size. We can also assume that families with two

incomes are not as price sensitive, so delivery fees and price premiums will be more acceptable to them.

Plus, there is an opportunity to provide busy households with non-grocery products that carry higher

margins. Some examples are diapers, laundry detergent and trash bags.

No Vehicle Urbanites: In 2012, 9.29% of households did not own a car, continuing an upward trend since

2007. Most consumers that do not have a vehicle live in a city. They either walk or use public

transportation to access groceries. Amazon Fresh is a great solution for these consumers because home

delivery removes the hassle involved with grocery shopping without a vehicle (travel time, carrying

heavy bags, etc.) These would be profitable consumers for Amazon Fresh because serving urban

consumers will increase market density and lower per order delivery costs.

Online Shoppers: The acceleration in online shopping and smartphone use indicates that the group of

consumers that prefers online to brick-and-mortar shopping is growing. This growth rate is likely to

increase as Millennials exit school and enter the workforce. More than 80% of the online population has

used the internet to purchase something. More than 50% of the online population has shopped online

more than once. The benefits of shopping online include time and gas savings, no crowd, access to variety

and easy price comparison and low prices. Amazon Fresh can create value for online shoppers by offering

groceries on their preferred platform—a product category that is currently underserved in the digital

space.

15. 14

High Income Singles: This segment includes high-income, single consumers that are young and tech-

savvy. Many of them work full-time and live in a city. These busy consumers are willing to pay a

premium for time savings. With Amazon Fresh, they will be free to migrate more of their shopping habits

online. They value the convenience of one-stop "anytime" shopping and home delivery. Cross-selling

hard goods with groceries will be a profitable marketing tactic with these consumers. Plus, Amazon

already has a best-in-class website and mobile app.

Two Working

Parents

No Vehicle

Urbanites

Online Shoppers High Income

Singles

Profitability

Size

Fit

Accessibility

All four segments are attractive with respect to their profitability, size, fit and accessibility.

"Online Shoppers" are a large consumer base, but it is difficult to assess their profitability and fit in terms

of order size and frequency because the grocery category is still new to this space. "Two Working

Parents" and "High Income Singles" represent the most profitable segments, and their needs are a perfect

fit for this value proposition. Generally, they spend more money more frequently than other households

due to higher incomes. This analysis confirms that Amazon Fresh should begin by targeting these two

consumer groups. I would focus on "High Income Singles" first because they are more likely to adopt a

disruptive, tech-enabled service. They are also more likely to live in cities, so they will be easier to serve.

16. 15

Value Proposition

Benefits Costs

Saves time/gas/hassle

Convenient 24/7 ordering

Reduces impulse purchases

Online specials

Removes social experience (gain

efficiency)

Door service

No vehicle required

Delivery fees / tipping

Delivery wait time

Lose ability to use certain coupons, ad

match and comparison shop

Lose ability to hand-pick each item

Removes social experience (lose

stimulation)

Premium pricing

Psychological switching costs (behavior

implications)

Fill-in trips to grocery store still required

Risk (late delivery, unattended groceries

& food safety implications)

Tipping

Requires planning

The diagram above displays both perceived and actual consumer costs and benefits of using

online grocery delivery. As you can see, there are many more costs than benefits associated with this

service, which explains why consumers have been slow to adopt this model where it is already available.

That being said, Amazon Fresh has an opportunity to target consumers who highly value the

major benefits of online grocery delivery. The strong benefits of convenience, efficiency and time savings

can outweigh the costs for a consumer depending on their current shopping behaviors, lifestyle, location

and income. This point emphasizes the strategic importance of focusing on the two target markets

recommended above. Initially, Amazon Fresh can offer a solution that best meets the needs of a specific

group of consumers that are pre-disposed to appreciate these benefits. These consumers will also be

willing to pay more for this service due to the high value they place on this benefit set. Furthermore, a

premium price aligns with the current operational capabilities and financial situation that characterizes the

phased installation of a new and expensive infrastructure. Therefore, Amazon Fresh must commit to and

communicate a focused value proposition to gain a niche foothold in a potentially large market. As

internal efficiencies and external awareness increase and prices decrease, Amazon Fresh will be in a

better position to serve the mass grocery market.

17. 16

The middle column in the marketecture below contains the three themes that should define the

Amazon Fresh value proposition. These are the key benefits that should be communicated to potential

customers.

18. 17

Distinct Competency

As previously discussed, Amazon’s distinct competency is operational excellence. Amazon

revolutionized the retail space by utilizing e-commerce and warehouse technology to provide a customer-

centric online shopping experience. Amazon’s tireless pursuit for efficiencies has given it the ability to

often offer lower prices than brick-and-mortar retail stores, and physical expansion has facilitated a

continuous increase in nationwide delivery speeds. Amazon’s strengths primarily exist within sourcing,

warehousing and shipping hard goods such as books and electronics.

Amazon can only leverage its operational excellence within warehousing and shipping to a

certain extent due to the unique nature of the grocery industry. Many of their advantages are lost because

of the intricacies of handling and delivering fresh foods, which requires additional infrastructure including

cold storage and a network of trucks. Historically, Amazon has used its operational excellence to compete

on price and merchandise selection, but this may not be possible with Fresh. Grocery delivery is a more

complex beast, and it will take a substantial amount of new resources to establish and roll-out effectively.

These fixed costs will further squeeze profitability out of an industry that already suffers from extremely

thin margins.

Competitors like Walmart that already have an established brick-and-mortar grocery network are

a major threat because they already deal with the sourcing, distribution and sale of fresh and perishable

foods. In many ways, they are in a better position to win in the online grocery space if they choose to

enter. Amazon Fresh will struggle to maintain market share if competitors are quick to imitate.

Positioning

For busy consumers, Amazon Fresh is the most convenient way to shop among all grocery providers

because same-day home delivery saves you precious time, money and energy.

This positioning statement incorporates the most important elements of the value proposition

according to the cost-benefit analysis and marketecture. Amazon’s distinct competency supports the

service speed required for same-day delivery.

19. 18

Marketing Mix

Products:

Amazon Fresh cannot compete with Wal-mart and other brick-and-mortar supermarkets on price

alone. Consumers in the target markets selected above tend to be more quality and health-

conscious and less price sensitive than other consumers. Therefore, Amazon Fresh should

differentiate itself by offering a product mix that includes specialty, local and gourmet products.

These products have higher margins and will increase average ticket size—two factors that

directly impact profitability. Plus, offering ‘higher end’ products in addition to staple brands will

give convenience-oriented consumers another reason to skip the store. Amazon Fresh has the

advantage of more warehousing space than brick-and-mortar stores have shelf space. This is the

merchandising strategy that FreshDirect has seen success with.3

Price:

Amazon Fresh should utilize a skim pricing strategy. Currently, the market size for online grocery

is a very small percentage of the total market size for grocery products, and there are high

variable costs per order, especially if deliveries are isolated. Charging a premium price to the

niche market of early adopters will help cover the initial costs associated with inefficiencies and

lack of scale.

An Amazon Fresh membership will cost $150 per year ($7.50 per delivery if they order 20

times). Like Amazon Prime members, these customers are likely to spend more per order and

buy more frequently than non-members. Initially, current Prime members are most likely to

commit to an Amazon Fresh membership because they trust Amazon and value the convenience

of one-stop shopping. Plus, they will be more profitable for Amazon because they are likely to

3

"Amazon Sets Its Sights on the Grocery Biz." TakePart. Web. 29 Nov. 2014.

20. 19

order other items with their groceries. Non-members will be charged 10% for delivery, which is

consistent with or lower than competing firms. This venture is not financially viable if Amazon

Fresh does not charge for delivery. It is assumed that 85% of customers will not have a

membership in Year 1.

From an industry perspective, competitors are less likely to react strongly to Amazon Fresh and

further reduce margins if they believe the company is not going after the mass market. After

some efficiencies have been developed, Amazon Fresh may be able to offer a more affordable

service that will appeal to a broader population segment. At that point, more consumers will be

aware of Amazon Fresh after the niche following produces word of mouth and truck visibility.

Promotion: Although Amazon Fresh will primarily target consumers that are predisposed to adopt this

service, many of them must still be enticed to shift their grocery habits from in-store to online.

$500,000 has been allocated for launch promotions in new service areas. Amazon Fresh should be

highlighted on Amazon.com’s homepage to build awareness. The Amazon Fresh trucks will also

generate awareness as consumers begin to see more of them on the road.

To reduce consumer risk and stimulate trial of this service, free delivery on first orders should be

offered. Marketing materials that call out this offer should be shipped within non-grocery orders

to generate interest.

Word of mouth will be an important marketing lever. Since this model is relatively new and

disruptive to the brick-and-mortar grocery industry, adoption rates will be low until consumers

become aware of the service, begin to understand how it works and see that other consumers have

benefitted from the convenience of home delivery. Social media should be utilized to engage with

the community, and customers should be encouraged to “share” their Amazon Fresh experiences

with friends and families. Social contests for a free membership or other prizes can be used to

generate buzz.4

4

Yarow, Jay. "Amazon Says It Has At Least 20 Million Prime Members."Business Insider. Business Insider, Inc, 06

Jan. 2014. Web. 29 Nov. 2014.

21. 20

Other online grocery companies such as Peapod and FreshDirect have seen success with referral

programs. After new customers set up an account, they are asked to invite others to try the service

at a discount ($10 off an order of $50 or free delivery). If any of their referees use the invitation

to create an account, the original customer will also receive a discount on their next order. This

strategy was also successful for Uber and Lyft, two companies that disrupted the taxi industry

with an innovative, tech-enabled model.

Place:

Amazon Fresh will use a direct-to-consumer model. Therefore, the distribution question is where

to locate warehouses to minimize infrastructure investment and delivery costs.

Consistent with the skim strategy described above, Amazon Fresh should not pursue a rapid entry

approach to expansion. Two markets in Year 1 is a sufficient start. Two of the thirteen cities

where Amazon currently offers same-day delivery of other products are recommended, because

warehouses that can serve these customers quickly are already located there. Perishable food

storage and staff can be added. See the appendix for a complete list of cities. Seattle and San

Francisco make sense from a geographical perspective because they are closest to Amazon’s

headquarters.

The number of service area launches can increase from two to three after Year 2, because the

process will be more mature and scale efficiencies will be needed.

Barr, Alistair. "Amazon Drops Low-price Strategy in Grocery Expansion."USA Today. Gannett, 11 Dec. 2013. Web.

29 Nov. 2014.

"Amazon Prime Members Spend Almost Twice as Much as Non-Members." (AMZN). Web. 29 Nov. 2014.

22. 21

D. Financial Analysis

Summary Numbers:

Year 1 Year 2 Year 3 Year 4 Year 5

Revenue $35,591,400.00 $100,977,880.39 $233,930,008.92 $579,519,585.83 $1,256,162,867.72

Var. Costs $31,688,434.44 $88,367,906.01 $201,225,006.78 $490,005,818.94 $1,044,047,849.87

Fixed Costs $6,515,054.00 $15,812,456.24 $35,171,601.07 $81,939,948.23 $175,201,172.80

Income -$2,612,088.44 -$3,202,481.87 -$2,466,598.9 $7,573,818.7 $36,913,845.0

Year 1 Year 5

Revenue ($) $35,591,400.00 $1,256,162,867.72

Gross Margin (%) 10.97% 16.89%

Operating Margin (%) -7.34% 2.94%

Operating Margin (%/Order) -- 3.12%

Although this venture is unlikely to be profitable in its first three years of operation, Amazon

Fresh is a viable opportunity for long-term profitability. A positive operating margin in its fourth and fifth

year and a per order operating margin of 3.12% at maturity indicate that this business model can reach

sustainability. In addition, delayed profitability is consistent with Amazon’s current investment

philosophy. That being said, the simplicity of these projections with respect to the complexity of this

model are worrisome. The success of this venture would depend on a near flawless execution of a

cohesive go-to-market strategy and rigorous cost control.

Challenges/Risks

The most significant challenges and risks for Amazon Fresh were revealed through two

sensitivity analyses (see appendix). The four most influential assumptions on Year 5 revenue include the

number of Year 1 customers in a given area, customer transactions per year, average dollar amount per

transaction and the number of service areas in Year 1. For example, the number of customers in a given

area in Year 1 represents a $1,352,790,781 swing in revenue. This re-emphasizes the risk of low adoption,

the importance of market selection and the need for a skim strategy. As mentioned previously, this service

is disruptive to current consumer shopping habits. Many consumers are hesitant to adopt for fear of low

product quality (they prefer to select their own items) and an unwillingness to plan an order or wait for

23. 22

delivery. The threat of low adoption rates can be addressed with marketing and service tactics that reduce

perceived risk, stimulate trial and encourage word of mouth such as no delivery fee on first orders, same-

day delivery and incentives for referral. In addition, selecting markets with a high concentration of target

consumers will increase adoption rates.

The greatest influencers of operating margin (as a percentage per order) include dollar amount per

transaction, annual increase in overhead, cost of goods sold and annual decrease in cost of goods sold.

Therefore, overhead expenses must be tightly controlled during expansion and bargaining power must be

established with producers to ensure a positive transaction margin. Bargaining power will be difficult to

obtain without purchasing higher quantities. The consistent addition of service areas (and new customers)

will provide economies of scale in this respect.

Additional Information

Again, these financial projections are based on several assumptions, so the feasibility of this

venture within the real-world business environment must remain under question. More information

should be gathered before moving forward. I would expect more analysis to be completed regarding

which markets (of the 13 cities suggested) to enter first based on consumer behavior and cost to establish

infrastructure. Some of these insights could be discovered with internal data (number of Prime members

in each area, warehouse capacity, proximity to producers, etc.). These cities should also be investigated

for target market prevalence and concentration.

Survey data could be collected in the two markets that Amazon Fresh will initially enter to

determine consumer willingness to adopt and their potential behaviors in terms of order frequency, order

spend and payment preference (10% fee per order vs. $150 annual membership). Customer growth rates

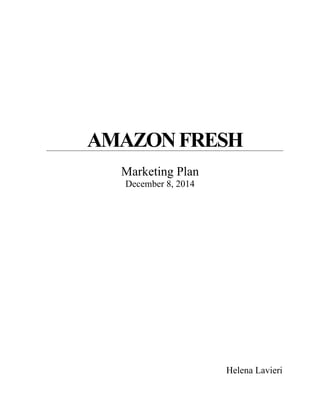

were based on Peapod’s service numbers from 1993-1997, so the relevance and accuracy of this data is

insufficient (see next page). Updated insights should be gathered indirectly through tools like choice

modeling and conjoint analysis because consumers will struggle to answer direct questions about this

model.

24. 23

See the appendix for growth rate calculations.

E. Conclusion

Grocery delivery is a viable market opportunity for Amazon Fresh, but there are several variables

that present significant challenges and risks. For example, low industry profitability will threaten the

success of this high investment venture. Also, the majority of consumers still prefer to shop for groceries

at traditional brick-and-mortar retailers. This service is disruptive to their current behaviors and likely to

suffer from low adoption rates. Amazon can leverage some of its strengths in operational excellence, but

several of its main advantages are difficult to translate to grocery handling. Furthermore, there are several

competitors that are in a strong position to imitate this service model quickly. If Amazon Fresh uses a

skim approach to market supported by a compelling marketing mix to target the four consumer segments

that will most highly value this offering, this venture will become profitable in Year 4. This opportunity

should be pursued with caution. A slow rollout with continuous reassessment is ideal.

3000

4900

7600

19700

36000

0

5000

10000

15000

20000

25000

30000

35000

40000

Year 1 Year 2 Year 3 Year 4 Year 5

#ofCustomers

Time

Peapod - # of Customers (in a given area)