Malaysia's Emerging Pharmacy Channel

•

1 like•949 views

The pharmacy channel in Malaysia has been growing faster than other healthcare channels since 2007, with a compound annual growth rate of 12.25% according to IMS Health data. The growth of pharmacies is due to an increasing number of retail outlets, more trained pharmacists, and patients becoming more comfortable obtaining medications directly from pharmacists. However, multinational pharmaceutical companies will need to adapt to Malaysia's changing healthcare landscape which includes a push to separate medication dispensing from physician offices to retail pharmacies. This will increase pressure on brand name drugs that traditionally relied on doctor prescriptions.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Malaysia's Emerging Pharmacy Channel

Similar to Malaysia's Emerging Pharmacy Channel (20)

More from QuintilesIMS Asia Pacific

More from QuintilesIMS Asia Pacific (20)

Recently uploaded

Recently uploaded (20)

Malaysia's Emerging Pharmacy Channel

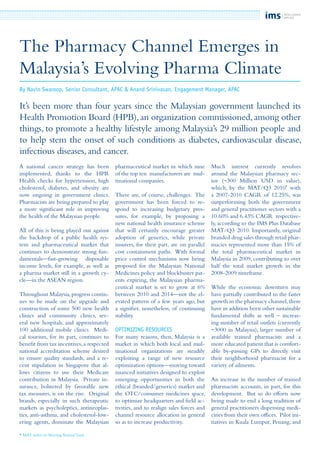

- 1. The Pharmacy Channel Emerges in Malaysia’s Evolving Pharma Climate A national cancer strategy has been implemented, thanks to the HPB. Health checks for hypertension, high cholesterol, diabetes, and obesity are now ongoing in government clinics. Pharmacists are being prepared to play a more significant role in improving the health of the Malaysian people. All of this is being played out against the backdrop of a public health sys- tem and pharmaceutical market that continues to demonstrate strong fun- damentals—fast-growing disposable income levels, for example, as well as a pharma market still in a growth cy- cle—in the ASEAN region. Throughout Malaysia,progress contin- ues to be made on the upgrade and construction of some 500 new health clinics and community clinics, sev- eral new hospitals, and approximately 100 additional mobile clinics. Medi- cal tourism, for its part, continues to benefit from tax incentives,a respected national accreditation scheme desired to ensure quality standards, and a re- cent stipulation in Singapore that al- lows citizens to use their Medicare contribution in Malaysia. Private in- surance, bolstered by favorable new tax measures, is on the rise. Original brands, especially in such therapeutic markets as psycholeptics, antineoplas- tics, anti-asthma, and cholesterol-low- ering agents, dominate the Malaysian pharmaceutical market in which nine of the top ten manufacturers are mul- tinational companies. There are, of course, challenges. The government has been forced to re- spond to increasing budgetary pres- sures, for example, by proposing a new national health insurance scheme that will certainly encourage greater adoption of generics, while private insurers, for their part, are on parallel cost containment paths. With formal price control mechanisms now being proposed for the Malaysian National Medicines policy and blockbuster pat- ents expiring, the Malaysian pharma- ceutical market is set to grow at 6% between 2010 and 2014—not the el- evated pattern of a few years ago, but a signifier, nonetheless, of continuing stability. Optimizing resources For many reasons, then, Malaysia is a market in which both local and mul- tinational organizations are steadily exploiting a range of new resource optimization options—moving toward nuanced initiatives designed to exploit emerging opportunities in both the ethical (branded/generics) market and the OTC/consumer medicines space, to optimize headquarters and field ac- tivities, and to realign sales forces and channel resource allocation in general so as to increase productivity. Much interest currently revolves around the Malaysian pharmacy sec- tor (~300 Million USD in value), which, by the MAT/Q3 2010* with a 2007-2010 CAGR of 12.25%, was outperforming both the government and general practitioner sectors with a 10.60% and 6.43% CAGR respective- ly, according to the IMS Plus Database MAT/Q3 2010. Importantly, original branded drug sales through retail phar- macies represented more than 15% of the total pharmaceutical market in Malaysia in 2009, contributing to over half the total market growth in the 2008-2009 timeframe. While the economic downturn may have partially contributed to the faster growth in the pharmacy channel,there have in addition been other sustainable fundamental shifts as well – increas- ing number of retail outlets (currently ~3000 in Malaysia), larger number of available trained pharmacists and a more educated patient that is comfort- able by-passing GPs to directly visit their neighborhood pharmacist for a variety of ailments. An increase in the number of trained pharmacists accounts, in part, for this development. But so do efforts now being made to end a long tradition of general practitioners dispensing medi- cines from their own offices. Pilot ini- tiatives in Kuala Lumpur, Penang, and By Navin Swaroop, Senior Consultant, APAC & Anand Srinivasan, Engagement Manager, APAC It’s been more than four years since the Malaysian government launched its Health Promotion Board (HPB),an organization commissioned,among other things, to promote a healthy lifestyle among Malaysia’s 29 million people and to help stem the onset of such conditions as diabetes, cardiovascular disease, infectious diseases, and cancer. * MAT refers to Moving Annual Total.

- 3. Johor are testing those waters. Messag- es are being sent to patients. Greater scrutiny is being paid to the physicians who have sought to benefit financially from overprescribing as well as to pa- tients, who, by virtue of moving from doctor to doctor, are confusing their own treatment plans and getting pre- scribed more medications than they should. One Ministry of Health of- ficial put it this way: “When you go to this clinic,the doctors will prescribe you something. You go to another clinic, you’ll probably get the same thing [...] they put you on overlapping prescriptions. We realize that, but un- til we get a system that can detect the moment you log in as a patient [you won’t know] that the patient has been supplied this. That is an issue we are trying to address.” It will, of course, take years—and the implementation of a national health insurance scheme that can offset the loss of general practitioner income— before a complete separation of dis- pensing channels can be achieved. Physicians are strongly opposed to any legislation that would limit their dispensing activities. The Malaysian Pharmaceutical Society, for its part, is arguing for separation, suggesting that it is time that community pharmacists be given more responsibility for pre- scription monitoring, patient educa- tion, and medicines management. Fi- nally, the draft master action plan for the National Medicines Policy has proposed a 2011 timeline for such a separation,except in those geographies where it is simply not yet feasible. The potential impact of such legisla- tion would, of course, be considerable. Suddenly there would be, in Malaysia, a new generation of stakeholders op- erating under different principles than existing norms—stakeholders invested with the power to switch prescriptions based on anticipated pharmacy profit margins. Succeeding in the new era No matter what the timeframe ulti- mately is, Malaysia is clearly entering a new era—one in which overprescrib- ing will diminish as individual hospitals closely scrutinize prescribing levels and in which increasing attention will be paid to the pharmacists employed by the country’s burgeoning network of retail and independent pharmacies. One obvious outcome of this shift- ing environment is the pressure that has been placed on branded original products, which doctors tend to pre- scribe with greater regularity than do the pharmacy outlets. Private sector doctors have not, heretofore, been bound to a set class of drugs; they have prescribed what their patients could afford. Public sector physicians,mean- while, have worked with an expansive formulary of both original and ge- neric products; in 2009, the Ministry of Health formulary contained 1,432 drugs, many of them innovator prod- ucts, along with pricing information. While the public hospital formular- ies apply some restrictions in terms of first-line use/specialist-only prescrib- ing of expensive drug classes, doctors in the public sector have maintained a reasonable degree of prescribing freedom when it came to brands. Pa- tients have trusted physicians to make the right choice, and, because co-pay- ments are either inapplicable or neg- ligible, have willingly accepted brand drug prices. Multinational companies that have re- lied on the sale of original products through physician offices must now re- assess their Malaysia strategy and forge new paths in the pharmacy channel. They must recognize, at the outset, the importance of building meaningful re- lationships with the right pharmacists. Turning challenges into opportuni- ties is vital into today’s pharmaceutical market place – and that is where the value of IMS Health lies - proven cli- ent success not text book theory. IMS Health-driven re-focusing of sales teams,identification of product oppor- tunities, competitive positioning op- tions and potential commercialization strategies all have proven successful. And with IMS Health as a partner, monitoring the market and reporting back on the results has been simply part of the benefit. PHARMACY CHANNEL HAS OUTPACED OTHER CHANNELS SINCE 2007 Sales Contribution by Sectors in Malaysia totalsales(consultantusd)(millions) 1400 1200 1000 800 600 400 200 0 MAT/Q3 ‘07 GOVERNMENT CLINIC HOSPITAL PHARMACY MAT/Q3 ‘08 MAT/Q3 ‘09 MAT/Q3 ‘10 457397 229 179 236227 180 235 410338 202 146 197 243 214 279 18% CAGR 09-10 20% 6% 15% © 2011 IMS Health Incorporated or its affiliates. All rights reserved. APAC Regional Office · 10 Hoe Chiang Road #23-01/02 Keppel Towers · Singapore 089315 · Tel: 65-6227 3006 · Email: info.sg@sg.imshealth.com