Periodic Inventory vs. Perpetual Inventory

•Download as ODP, PDF•

26 likes•46,778 views

Lesson in Bookkeeping

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Periodic Inventory vs. Perpetual Inventory

Similar to Periodic Inventory vs. Perpetual Inventory (20)

Recently uploaded

Recently uploaded (20)

Periodic Inventory vs. Perpetual Inventory

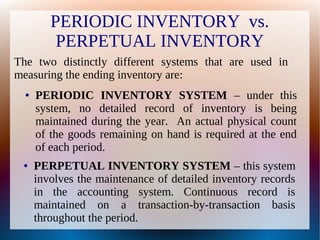

- 1. PERIODIC INVENTORY vs. PERPETUAL INVENTORY The two distinctly different systems that are used in measuring the ending inventory are: ● PERPETUAL INVENTORY SYSTEM – this system involves the maintenance of detailed inventory records in the accounting system. Continuous record is maintained on a transaction-by-transaction basis throughout the period. ● PERIODIC INVENTORY SYSTEM – under this system, no detailed record of inventory is being maintained during the year. An actual physical count of the goods remaining on hand is required at the end of each period.

- 2. DISADVANTAGES PERIODIC INVENTORYPERIODIC INVENTORY ● The necessity (and cost) to take a complete physical count of all merchandise on hand at the end of each period for which financial statements are to be prepared. ● Lack of inventory control (for purchasing purposes and measurement of theft). PERPETUAL INVENTORYPERPETUAL INVENTORY ● The maintenance of a separate inventory record for each type of goods stocked on a transaction- by transaction basis can be time consuming and costly. ● May involve a considerable amount of clerical effort.

- 3. PERIODIC INVENTORY SYSTEM COST OF GOODS SOLD MODEL: Cost of Goods Sold = Beg. Inventory + Purchases of the Period - Ending Inventory

- 4. PERPETUAL INVENTORY RECORD Item: Super x Unit Price P 200- Location Storage Rm Date Explanation Qty Pur- chased Cost Qty Sold Cost Balance on Hand Cost Jan 1 Beg. Inventory 8 1,600- Jan 31 Sold 5 1,000- 3 600- Feb 5 Purchases 10 2,000- 13 2,600- Mar 6 Return sales (1) (200-) 12 2,400- Recap: Total Purchases: 10 2,000- CGS: 4 800- End Inventory: 12 2,400-

- 5. RECORDING OUTLINE (PERIODIC) ● Record all purchases – During the period the purchase cost of all goods bought is accumulated in an account called Purchases. ● Record all sales – During the period, the sales price for all goods sold is accumulated in a Sales Revenue account. ● Count the number of units on hand – At the end of the period, the Inventory Account Balance still reflects the inventory amount carried over from the prior period since no entries are made to the Inventory account during the current period.

- 6. Thus, to measure the Ending Inventory for the current period, a physical inventory count must be made of all goods on hand. ● Compute the cost of the Ending Inventory – the amount of the ending inventory quantities is computed by multiplying the number of units found as determined by the inventory count to be on hand times to their unit purchase cost. ● Compute Cost of Goods Sold – After the ending inventory valuations is measured, cost of goods sold for the period must be computed as per cost of goods sold model presented on Slide no. 3.

- 7. RECORDING OUTLINE (PERPETUAL) ● Record all purchases – During the period, the purchase cost of each type of goods bought is entered in the Inventory ledger account as an increase and in a detailed perpetual inventory record as shown in the table under slide no. 4. ● Record all sales – During the period, each sales is recorded by means of two companion entries. One entry is to record the Sales Revenue at sales price, and the other entry is to record the Cost of Goods Sold at purchase cost.

- 8. ● Record all returns – During the period, Purchase Returns and Sales Returns are recorded in the Inventory account and on the perpetual inventory record at cost. ● Use Cost of Goods Sold and Inventory Amounts – At the end of the period, the balance in the Cost of Goods Sold accounts provides the total amount of that expense that is reported on the income statement.

- 9. DIFFERENCES BETWEEN PERIODIC AND PERPETUAL ● Inventory a. Periodic – During the period, the inventory account is not change; thus, it reflects the beginning inventory amount. During the period, each purchase is recorded in the Purchases account. As a consequence, the ending inventory eache period must be measured by physical count, then ”costed” at unit price cost. b. Perpetual - During the period, the Inventory account is increased for each purchase and decreased (at cost) for each sale. Thus, at the end

- 10. of the period, it measures ending inventory. ● Cost of Goods Sold a. Periodic – During the period, no entry is made for cost of goods sold. At the end of the period, after the physical inventory count, cost of goods sold is measured as: Beg. Inventory + Purchases – End. Inventory = Cost of Goods Sold b. Perpetual - During the period, cost of goods sold is recorded at the time of each sale and the Inventory account is reduced (at cost). Thus the system measure the cost of goods sold amount for the period.

- 11. ADVANTAGES OF PERPETUAL INVENTORY OVER PERIODIC INVENTORY● It provides continuous inventory amounts ● It provides the cost of goods sold amount without the necessity of taking a periodic inventory count. ● It provides continuing information necessary to maintain minimum and maximum inventory levels by appropriate timing of purchases. ● It provides continuing information about the quantity of goods on hand at various locations. ● It provides a basis for measuring the amount of theft.It provides cost of goods sold information needed to record sales at both selling price and cost. ● It is readily adaptable to use of computers to process quickly large quantities of inventory data.