Wealth management the next frontier of disruption | afr.com

1. 18/09/2015 10:35 amWealth management the next frontier of disruption | afr.com

Page 1 of 5http://www.afr.com/business/banking-and-finance/financial-servic…ealth-management-the-next-frontier-of-disruption-20150318-1m2kph

Home / Business / Banking & Finance / Financial Services

Safari Power Saver

Click to Start Flash Plug-in

Mar 22 2015 at 12:49 PM | Updated Mar 22 2015 at 7:49 PM

Wealth management the next frontier of disruption

|SAVE ARTICLE PRINT REPRINTS & PERMISSIONS

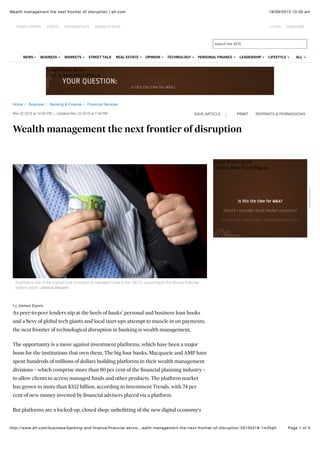

Australia is one of the highest cost providers of managed funds in the OECD, according to the Murray financial

system report. Jessica Shapiro

by James Eyers

As peer-to-peer lenders nip at the heels of banks' personal and business loan books

and a bevy of global tech giants and local start-ups attempt to muscle in on payments,

the next frontier of technological disruption in banking is wealth management.

The opportunity is a move against investment platforms, which have been a major

boon for the institutions that own them. The big four banks, Macquarie and AMP have

spent hundreds of millions of dollars building platforms in their wealth management

divisions – which comprise more than 80 per cent of the financial planning industry –

to allow clients to access managed funds and other products. The platform market

has grown to more than $332 billion, according to Investment Trends, with 74 per

cent of new money invested by financial advisers placed via a platform.

But platforms are a locked-up, closed shop, unbefitting of the new digital economy's

Safari Power Saver

Click to Start Flash Plug-in

Advertisement

search the AFR

STREET TALKNEWS BUSINESS MARKETS REAL ESTATE OPINION TECHNOLOGY PERSONAL FINANCE LEADERSHIP LIFESTYLE ALL

TODAY'S PAPER VIDEOS INFOGRAPHICS MARKETS DATA LOGIN SUBSCRIBE

2. 18/09/2015 10:35 amWealth management the next frontier of disruption | afr.com

Page 2 of 5http://www.afr.com/business/banking-and-finance/financial-servic…ealth-management-the-next-frontier-of-disruption-20150318-1m2kph

RELATED ARTICLES

|

Turnbull coup resets a government

that had stopped working

Canning now a test for Malcolm

Turnbull

Tax is Turnbull's boat problem

Retirees can't afford not to take risks

Get 'micro' reform right and

prosperity will follow

LATEST STORIES

4 mins ago

NSW mulls sale of property data

agency

7 mins ago

Is this $10m watch the world's

most complex?

8 mins ago

Europe's open borders under

threat

openness and transparency. Access to these proprietary technology systems is tightly

controlled by the banks, dealer groups and superannuation funds. It is a classic

example of bundled product: investments, administration, broking, trustee services,

cash management, product distribution and asset consulting are all on a platform

investment menu.

All these bells and whistles come at a high cost: institutionally-owned platforms

roughly charge between 50 basis points and 70 basis points in fees of assets under

administration.

The financial system inquiry chaired by David Murray was critical of high

superannuation costs. Australia is one of the highest cost providers of managed funds

in the OECD, the report said, despite Australian having the highest managed fund

balances in the world. These costs can be partly explained by high transaction costs

from the bundling of advice, trading and platforms.

Enter Mike Ghenta, a former McKinsey consultant who says the current managed

fund distribution model is broken and primed for digital disruption. An American

resident in Australia for a decade, Ghenta says two new technological developments

over the past year will radically change the way in which financial advice is delivered.

The first is the Australian Securities Exchange's new mFund Settlement

Service, allows any consumer with a broker to buy and sell managed funds directly on

the ASX in the same way and for the same cost as they buy and sell ASX shares,

without having to use a financial planner or a platform.

The second development is the arrival of "robo advice", where computer

algorithms help determine investor risk tolerance and decide on asset allocation that

are implemented in an automated, low cost process.

Ghenta says mFunds has the opportunity to disrupt the way managed funds are

offered in Australia by unbundling advice, distribution and trading by providing a

much more effective distribution model to one of the most popular investment

products in Australia, being managed funds, at a significantly lower cost. For fund

managers, it opens up a new distribution channel and can provide a lower cost

compared to platform distribution. There are also efficiency gains from the

automated ASX processing.

Trading on mFund began 10 months ago. The ASX is not making its transaction

volumes public. There are now 77 funds managed by 23 fund managers on the service,

including offerings from AMP, PIMCO, Aberdeen, Platinum, UBS, Lonsec

Stockbroking, Bell Direct, CMC Markets, Baillieu Holst, Burrell Stockbroking and

Pershing Securities are all linked into mFund but the ASX says two-thirds of all

transactions are originating from financial planners, suggesting the brokers are

largely feeding wholesale clients into the service rather than targeting retail clients

with a direct offering.

Despite the establishment of online equities trading websites to link retail investors

Advertisement

3. 18/09/2015 10:35 amWealth management the next frontier of disruption | afr.com

Page 3 of 5http://www.afr.com/business/banking-and-finance/financial-servic…ealth-management-the-next-frontier-of-disruption-20150318-1m2kph

with the stockmarket, when it comes to mFund, the big four banks are all sitting on

the sidelines. Ghenta says this cannot be surprising given the incentives in the

vertically integrated banking model, where banks seek to sell wealth management

services to other customers, and the incentives – including platform fees – which are

built into the system. "By adopting mFund, banks also risk cannibalising their existing

financial planning clients," he says.

An engineer turned investment banker, Ghenta has an impressive track record in the

markets. He was on trading desk of First Boston during the 1987 stockmarket crash,

and rode the dot com boom at Doubleclick (now part of Google). He had an eight-year

stint at McKinsey, where he worked alongside Adair Turner, now chairman of the UK

Financial Services Authority, restructuring the Romanian banking system after the

collapse of Communism, and with Roger Ferguson, the ex vice-chairman of the US

Federal Reserve. He also launched the first online trading platform for private clients

globally under Jamie Dimon at Smith Barney.

After moving to Australia in 2004, he working with the Grattan Institute's John Daley

at eTrade and was chief executive of Rockwell Financial, a private equity firm, which

he left earlier this year to pursue a launch of a company that provides "affordable

managed funds to the masses", as he describes it. "I see a significant opportunity for

this in Australia, given the structural inefficiencies of our financial advice industry,

some of which have been highlighted in David Murray's FSI report."

David Murray found in his December report that "the high concentration and steadily

increasing vertical integration" in the wealth management sector "has the potential to

limit the benefits of competition in the future". Restoring trust in the financial advice

industry will be a key theme of the annual Australian Securities and Investments

Commission Forum in Sydney, which begins on Monday and concludes on Tuesday. It

also comes as the Australian Prudential Regulation Authority sent a letter to

superannuation funds last week warning them that management of conflicts of

interest in superannuation needed to be improved.

But perhaps the more ominous for banks' wealth management operations is not the

focus of the FSI on advice in particular but technology in general. Ghenta met on

Friday with inquiry panel member Craig Dunn, who is also the new chair of Stone and

Chalk, a hub for fintech players that is being built in Sydney at Level 26, at 45 Clarence

Street. Dunn encouraged Ghenta to move into the incubator, which may also attract

start-ups working in robo advice.

When mFund is overlaid with a robo advisor, Ghenta says his model becomes even

more powerful – as the robo advisor automates independent research at a low cost.

Under this model, computers are programmed to trawl thousands of sources and can

determine when fund portfolios might be rebalanced, to account for changing

personal circumstances, asset allocation recommendations or changes in fund

ratings. The automated process addresses concerns about vertical integration,

including conflict of interest and the cost and quality of advice, issues that have

plagued the industry.

4. 18/09/2015 10:35 amWealth management the next frontier of disruption | afr.com

Page 4 of 5http://www.afr.com/business/banking-and-finance/financial-servic…ealth-management-the-next-frontier-of-disruption-20150318-1m2kph

Recommended by

RECOMMENDED

Why your diversified portfolio is no longer safe

The looming debt mining services companies

don't want you to see

CBA joins global banks in project to explore

bitcoin model

Banks target young with P2P lending for

weddings, parties, anything

The emerging threat to Bill Shorten and unions

FROM AROUND THE WEB

Eddie McGuire’s latest $12 million Toorak

purchase

News

Over 1/3 Australian women expect they won't

have enough money to fund a…

MLC

Extremely Brilliant Way To Pay Next To Nothing

For iPads

LifeFactopia

How far does $1 million get you in retirement?

AMP

These Are the Dumbest Presidents in History

InsideGov

LOGIN

TOOLS

Markets Data

Australian Equities

World Equities

Commodities

Currencies

Derivatives

Interest Rates

Share Tables

FAIRFAX BUSINESS MEDIA

The Australian Financial Review Magazine

BOSS

Chanticleer

Luxury

Rear Window

The Sophisticated Traveller

CONTACT & FEEDBACK

FAQ

Contact us

Letters to the Editor

Give feedback

Advertise

Reprints & Permissions

CONNECT WITH US

YOUR OPINION IS IMPORTANT TO US

CHOOSE YOUR READING EXPERIENCE

SUBSCRIBE

BRW

Smart Investor

GIVE FEEDBACK

Investors with super portfolios under $100,000 would have the most to gain from

accessing managed funds directly via the ASX given, Ghenta says, given they are not

large enough to provide diversification through individual holdings, while the quality

of advice for small portfolios is variable and fees are relatively higher. It could also be

compelling for nigh net worth investors and self managed superannuation funds.

He also reckons offshore players would be scouting for opportunity in the space; their

potential arrival would put banks and dealer groups on the back foot given their

recalcitrance at becoming early movers.