1. Compiled by Prof. M.B. Thakoor

RESIDENTIAL STATUS

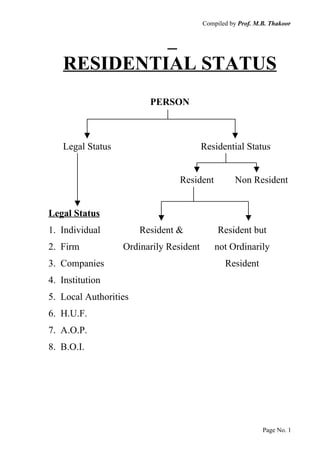

PERSON

Legal Status Residential Status

Resident Non Resident

Legal Status

1. Individual Resident & Resident but

2. Firm Ordinarily Resident not Ordinarily

3. Companies Resident

4. Institution

5. Local Authorities

6. H.U.F.

7. A.O.P.

8. B.O.I.

Page No. 1

2. Compiled by Prof. M.B. Thakoor

RESIDENTIAL STATUS: SEC. 6 (1)

After determining the legal status of an Assessee u/s. 2 (31)

the Residential Status of an Assessee is to be determined.

1. Determined of every PREVIOUS YEAR:

Residential Status is determined for every previous year.

It depends on the number of days a person is in India

during the concerned previous year.

2. Different terms of Citizenship

An Individual may be a Citizen of Britain, but a resident

in India. In the same way a Citizen of India may be a

non-resident of India.

3. Residential Status is important in deciding whether

Foreign Income of a person is Taxable or not.

TEST OF RESIDENCE

1. For an INDIVIDUAL

Basic 2 conditions

An Individual is said to be resident when he satisfies

any one of the basic 2 conditions.

1. He must be in India for 182 days or more in that

relevant pervious year.

OR

2. a. He must be in India for 365 days or more

during 4 previous year immediately preceeding

the relevant previous year.

AND

b. He must be in India during that relevant

previous year for a period of 60 day or more.

Page No. 2

3. Compiled by Prof. M.B. Thakoor

EXCEPTION: FOLLOWING ARE THE TWO

EXCEPTIONS TO RULE OF STAY IN INDIA

FOR A PERIOD OF 60 DAYS IN THE SECOND

CONDITION ABOVE.

1. If a citizen of India or a member of a crew of an Indian

ship leaves India in the previous year for the purpose of

employment then he becomes resident if the 60 days are

replaced by 182 days.

Employment : Self Employment

Salaried Employed

Professional

Non-professional

i.e. he becomes resident only if he stays in India for 182

days or more and not 60 days or more.

2. A citizen of India or a person of Indian Origin staying

outside India, come on a visit to India in the previous

year, then the 60 days must be replaced by 182 days.

i.e. he become resident only if he stay’s in India for 182

days and not 60 days.

Note: A person is deemed to be of an Indian origin, if he or

his parents or any of his grand parents were born in

Undivided India. (i.e. India, Pakistan, Bangladesh)

For Current ASSESSMENT YEAR

An Individual will become a resident in India in the P.Y.

2006-2007 i.e. for current assessment year 2007-2008 if he

satisfies any one of the following 2 basic conditions.

1. He is in India for 182 days or more in the previous year

2006-2007.

OR

Page No. 3

4. Compiled by Prof. M.B. Thakoor

2. He is in India for 365 days or more during the period

1.04.2002 to 31.03.2006

AND

He is in India for 60 days or more in the pervious year

2006-2007.

EXCEPTIONS

1. If a citizen of India, or a member of crew of Indian ship,

leaves India in 2006-2007 for the purpose of employment

will became a resident only if he stays in India for 182

days or more & not 60 days during 2006-2007 and he

must be in India for 365 days or more during 4 pervious

years preceeding the P.Y. 2006-2007 i.e. He must be in

India for 365 days or more from 01/04/2002 to

31/03/2006.

2. A citizen of India or a person of Indian Origin, who is

staying outside India comes on a visit to India in

2006-20074 becomes a resident only if he stays in India

for 182 days or more (and not 60 days) during 2006-2007

and he must be in India for 365 days or more during 4

previous year preceeding the previous year 2006-2007

i.e. He must be in India for 365 days or more from

1.04.2002– 31.03.2006.

NON-RESIDENT FOR AN INDIVIDUAL

Non-resident is a person who is not a resident. An Individual

who does not satisfy the test laid down in Sec (1) above is

called a non-resident i.e. An individual who do not satisfy any

of the basic conditions above is called a non-resident.

Page No. 4

5. Compiled by Prof. M.B. Thakoor

RESIDENT & ORDINARILY RESIDENT - Sec 6 (6)

If an Individual satisfies the test of Resident then further 2

tests are to be made i.e. If an Individual is a Resident in India,

he may be either Resident and Ordinarily Resident or

Resident but not ordinarily resident.

An Individual may be Resident and Ordinarily Resident if he

satisfies following 2 conditions.

1. He has been resident in India for at least 2 out of 10

years immediately preceeding the previous year.

AND

2. He has been present in India for a period of 730 days or

more during 7 years immediately preceding the

previous year.

Current A.Y. 2007-2008

Thus during the current Assessment Year 2007-2008 a

Resident Individual is tested as an Ordinary resident. If

1. He has been a resident in India for at least 2 out of 10

years immediately preceeding the P.Y. 2006-2007.

1. 1996-1997

2. 1997-1998

3. 1998-1999

4. 1999-2000

5. 2000-2001

6. 2001-2002

7. 2002-2003

8. 2003-2004

9. 2004-2005

10. 2005-2006

i.e. from 1st April 1996 to 31st March 2006 for these 10 years

he must have been a resident for 2 years i.e. from

1.04.1996-31.03.2006.

Page No. 5

6. Compiled by Prof. M.B. Thakoor

2. He has been physically present in India for a period of

730 days or more during 7 years immediately preceeding

the previous year 2006-2007.

1. 1999-2000

2. 2000-2001

3. 2001-2002

4. 2002-2003

5. 2003-2004

6. 2004-2005

7. 2005-2006

i.e. He must have stayed in India physically for 730 days from

1.04.1999 – 31.03.2006.

If both the above conditions are satisfied then the Individual is

Resident and Ordinarily Resident. But if the additional 2

tests are not satisfied by an Individual then he is said to be

Resident but not Ordinarily Resident.

Counting of Days

While counting of number of days in all the above cases the

following points are to be noted.

1. The stay need not be at the same place.

2. The stay need not be continuous.

3. Where the stay is for part of the day, physical presence

should be calculated on timely basis. Stay of 24 Hrs.

will be counted as stay for 1 day. Where such

information is not available, both the days of entry and

exit will be counted as full days.

4. A stay in a boat anchored in territorial area of India, is

treated as stay in India.

Page No. 6

7. Compiled by Prof. M.B. Thakoor

RESIDENTIAL STATUS FOR HUF SEC 6 (2)

A Hindu Undivided Family (HUF), is said to be resident in

India IF ITS CONTROL AND MANAGEMENT IS

SITUATED IN INDIA either WHOLLY OR PARTLY during

that PREVIOUS YEAR.

A Resident HUF is an ORDINARILY RESIDENT if the

KARTA or MANAGER of the Family is a Resident and

Ordinarily Resident.

A Hindu Undivided Family (HUF), is said to be ‘NON

RESIDENT’ in India. IF ITS CONTROL AND

MANAGEMENT IS SITUATED WHOLLY OUTSIDE

INDIA during that PREVIOUS YEAR.

CONTROL AND MANAGEMENT IS SITUATED AT A

PLACE WHERE THE HEAD/BRAIN, THE SEAT OF THE

DIRECTING POWER IS SITUATED.

RESIDENT BUT NOT ORDINARY RESIDENT Sec.(6) (g)

A HINDU UNDIVIDED FAMILY IS SAID TO BE ‘NON

ORDINARILY RESIDENT IN INDIA in any previous year if

its Manager is treated as an ‘NOT ORDINARILY

RESIDENT’ in India during that previous year.

Page No. 7

8. Compiled by Prof. M.B. Thakoor

RESIDENTIAL STATUS FOR A COMPANY Sec. 6 (3)

A COMPANY SAID to be ‘Resident in India’ in any previous

year if –

1) It is an INDIAN COMPANY

OR

2) DURING THAT YEAR THE CONTROL AND

MANAGEMENT OF ITS AFFAIRS IS SITUATED

WHOLLY IN INDIA.

THUS AN INDIA COMPANY IS ALWAYS RESIDENT IF

CONTROL & MANAGEMENT IS IN INDIA OR OUTSIDE

INDIA.

FOREIGN COMPANY IS ALWAYS RESIDENT IF

CONTROL & MANAGEMENT OF ITS AFFAIRS IS

SITUATED WHOLLY IN INDIA, DURING THAT YEAR.

CONTROL & MANAGEMENT indicates THE HEAD AND

BRAIN WHICH DIRECT THE AFFAIR OF THE

COMPANY IN RESPECT OF ITS POLICY, FINANCE,

DISPOSAL OF PROFIT, MANAGEMENT ETC. i.e. PLACE

WHERE THE MEETING OF ITS BOARD OF DIRECTOR

ARE HELD.

Page No. 8

9. Compiled by Prof. M.B. Thakoor

RESIDENTIAL STATUS OF A FIRM OR AN ASSOCIATION

OF PERSON EVERY OTHER PERSON S 6(4)

A PARTNERSHIP FIRM OR AN ASSOCIATION OF

PERSONS (AOP) OR EVERY OTHER PERSON IS SAID

TO BE A RESIDENT IN INDIA IF THE CONTROL AND

MANAGEMENT OF ITS AFFAIRS ARE SITUATED IN

INDIA EITHER WHOLLY OR PARTLY during that

pervious year.

A PARTNERSHIP FIRM OR AN ASSOCIATION OF

PERSONS (AOP) or every other person is SAID TO BE

NON RESIDENT IN INDIA IF ITS CONTROL AND

MANAGEMENT IS SITUATED WHOLLY OUTSIDE

INDIA during THAT PREVIOUS YEAR.

“CONTROL AND MANAGEMENT IS SITUATED AT A

PLACE WHERE THE HEAD/BRAIN THE SEAT OF THE

DIRECTING POWER IS SITUATED”.

Page No. 9