For major deals where access to international liquidity and post-closing debt circulation on secondary marked are important, the main alternatives are bank debt (with the support of a fronting structure) and listed bonds. We tried to summarize the main issues. Any solution has to be identified on a case-by-case basis after a careful analysis of the transaction.

GIFT City Overview India's Gateway to Global Finance

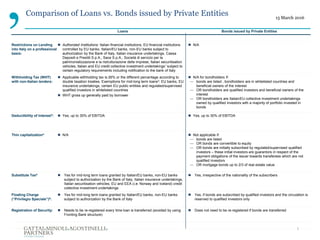

Comparison of Loans vs. Bonds issued by Private Entities

1. 15 March 2016

1

Loans Bonds issued by Private Entities

Restrictions on Lending

into Italy on a professional

basis:

Authorized Institutions: Italian financial institutions, EU financial institutions

controlled by EU banks, Italian/EU banks, non-EU banks subject to

authorization by the Bank of Italy, Italian insurance undertakings, Cassa

Depositi e Prestiti S.p.A., Sace S.p.A., Società di servizio per la

patrimonializzazione e la ristrutturazione delle imprese, Italian securitisation

vehicles, Italian and EU credit collective investment undertakings1 subject to

certain regulatory requirements including notification to the bank of Italy

N/A

Withholding Tax (WHT)

with non-Italian lenders:

Applicable withholding tax is 26% or the different percentage according to

double taxation treaties. Exemptions for mid-long term loans2: EU banks, EU

insurance undertakings, certain EU public entities and regulated/supervised

qualified investors in whitelisted countries

WHT gross up generally paid by borrower

N/A for bondholders if:

— bonds are listed , bondholders are in whitelisted countries and

beneficial owners of the interest

— OR bondholders are qualified investors and beneficial owners of the

interest

— OR bondholders are Italian/EU collective investment undertakings

owned by qualified investors with a majority of portfolio invested in

bonds

Deductibility of Interest3: Yes, up to 30% of EBITDA Yes, up to 30% of EBITDA

Thin capitalization4 N/A Not applicable if:

— bonds are listed

— OR bonds are convertible to equity

— OR bonds are initially subscribed by regulated/supervised qualified

investors – these initial investors are guarantors in respect of the

payment obligations of the issuer towards transferees which are not

qualified investors

— OR mortgage bonds up to 2/3 of real estate value

Substitute Tax5 Yes for mid-long term loans granted by Italian/EU banks, non-EU banks

subject to authorization by the Bank of Italy, Italian insurance undertakings,

Italian securitisation vehicles, EU and EEA (i.e. Norway and Iceland) credit

collective investment undertakings

Yes, irrespective of the nationality of the subscribers

Floating Charge

(“Privilegio Speciale”)6:

Yes for mid-long term loans granted by Italian/EU banks, non-EU banks

subject to authorization by the Bank of Italy

Yes, if bonds are subscribed by qualified investors and the circulation is

reserved to qualified investors only

Registration of Security: Needs to be re-registered every time loan is transferred (avoided by using

Fronting Bank structure)

Does not need to be re-registered if bonds are transferred

Comparison of Loans vs. Bonds issued by Private Entities

2. 15 March 2016

2

1) With respect to EU credit collective investment undertaking specific legislation is expected soon

2) Loans having a duration longer than 18 months

3) Interest payments are deductible up to a threshold of 30% EBITDA

4) “Thin Capitalization” limits borrowing in the bond market for private entities to 2x Net Worth

5) The optional 0.25 substitute tax (“imposta sostitutiva”) regime (calculated on the aggregate principle amount of that issuance), previously

available for mid-long term bank loans and corporate bonds, is extended to the security package for mid-long term loans granted by EU

insurance undertakings, Italian securitisation vehicles and EU and EEA (i.e. Norway and Iceland) credit collective investment undertakings.

Please consider that the substitute tax now also covers assignments of loans, related receivables and security package

6) The “privilegio speciale” can cover several types of corporate assets, such as plants, equipment and machinery, raw materials and inventory,

finished products, commodities, assets acquired using the proceeds of the mid-long term bank loans/corporate bonds or receivables deriving

from the sale of any of the foregoing assets. It cannot cover real estate or registered movable assets (airplanes, ships or cars)

Comparison of Loans vs. Bonds issued by Private Entities

Footnotes