The World in 2013 : ICTFacts and Figures

•

1 like•9,191 views

Les données de l’IUT (International Telecoms Union), l’Union Internationale des télécommunications montre la croissance de l'utilisation du mobile dans le monde. Retrouvez mon billet dédié sur http://marketing-webmobile.fr

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (16)

Similar to The World in 2013 : ICTFacts and Figures

Similar to The World in 2013 : ICTFacts and Figures (20)

More from Thierry Pires

More from Thierry Pires (20)

Recently uploaded

Recently uploaded (20)

The World in 2013 : ICTFacts and Figures

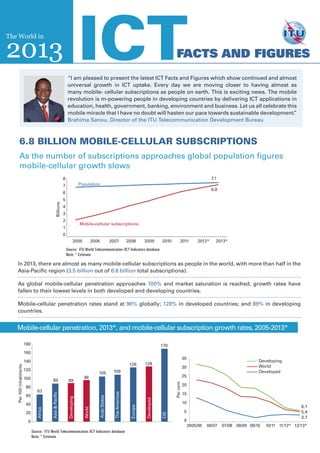

- 1. 6.8 billion mobile-cellular subscriptions As the number of subscriptions approaches global population figures mobile-cellular growth slows The World in 2013 ICTFacts and Figures In 2013, there are almost as many mobile-cellular subscriptions as people in the world, with more than half in the Asia-Pacific region (3.5 billion out of 6.8 billion total subscriptions). As global mobile-cellular penetration approaches 100% and market saturation is reached, growth rates have fallen to their lowest levels in both developed and developing countries. Mobile-cellular penetration rates stand at 96% globally; 128% in developed countries; and 89% in developing countries. Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate Billions 7.1 6.8 8 7 6 5 4 3 2 1 0 2005 2006 2007 2008 2009 2010 2011 2012* 2013* Population Mobile-cellular subscriptions Mobile-cellular penetration, 2013*, and mobile-cellular subscription growth rates, 2005-2013* 180 160 140 120 100 80 60 40 20 0 63 89 89 96 105 109 126 128 Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate 2005/06 06/07 07/08 08/09 09/10 10/11 11/12* 12/13* 35 30 25 20 15 10 5 0 6.1 5.4 3.7 __ Developing __ World __ Developed 170 Africa Asia&Pacific Developing World ArabStates TheAmericas Europe Developed CIS Percent Per100inhabitants “I am pleased to present the latest ICT Facts and Figures which show continued and almost universal growth in ICT uptake. Every day we are moving closer to having almost as many mobile- cellular subscriptions as people on earth. This is exciting news. The mobile revolution is m-powering people in developing countries by delivering ICT applications in education, health, government, banking, environment and business. Let us all celebrate this mobile miracle that I have no doubt will hasten our pace towards sustainable development.” Brahima Sanou, Director of the ITU Telecommunication Development Bureau

- 2. 2.7 billion people – almost 40% of the world’s population – are online In developing countries, 16% fewer women than men use the Internet Internet users by development level, 2003-2013*, and by region, 2013* The gender gap: men and women online, totals and penetration rates, 2013* In 2013, over 2.7 billion people are using the Internet, which corresponds to 39% of the world’s population. In the developing world, 31% of the population is online, compared with 77% in the developed world. Europe is the region with the highest Internet penetration rate in the world (75%), followed by the Americas (61%). In Africa, 16% of people are using the Internet – only half the penetration rate of Asia and the Pacific. Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate Per100inhabitants Africa Asia Arab CIS The Europe & Pacific States Americas 16 32 52 38 61 75 80 70 60 50 40 30 20 10 0 80 70 60 50 40 30 20 10 0 Per100inhabitants __ Developed __ World __ Developing 2003 04 05 06 07 08 09 10 11 12* 13* 74% 80% 29% 37% 41% 33% Women Men Women Men Women Men Developed Developing World 1.4 1.2 1.0 0.8 0.6 0.4 0.2 0.0 Billionsofpeople Internet users % all of men/women More men than women use the Internet: globally, 37% of all women are online, compared with 41% of all men. This corresponds to 1.3 billion women and 1.5 billion men. The developing world is home to about 826 million female Internet users and 980 million male Internet users. The developed world is home to about 475 million female Internet users and 483 million male Internet users. The gender gap is more pronounced in the developing world, where 16% fewer women than men use the Internet, compared with only 2% fewer women than men in the developed world. 77 39 31

- 3. Households with Internet access, 2013* Households with Internet access, by region 750 million households – 41% globally – connected to the Internet In 2013, 41% of the world’s households are connected to the Internet. Half of them are in the developing world, where household Internet penetration has reached 28%. In the developed world, 78% of all households are connected to the Internet. 90% of the 1.1 billion households not connected to the Internet are in the developing world. Europe and Africa are the regions with the highest and the lowest levels of household Internet penetration respectively: 77% in Europe, compared with 7% in Africa. The majority of households in the Americas are online (61%), compared with around one third of households in the Arab States and Asia and the Pacific. Between 2009 and 2013, Internet penetration in households has grown fastest in Africa, with annual growth of 27%, followed by 15% annual growth in Asia and the Pacific, the Arab States and the CIS. C 10Y 100 M 75 K 15 C 74Y 45 M 0 K 27 C 70Y 15 M 0 K 12 C 50Y 10 M 100 K 0 C 0Y 50 M 100 K 0 MAIN COLOURS SECONDARY COLOURS Developing countries Developed countries Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate __Europe __The Americas __CIS __Arab States __Asia & Pacific __Africa 2005 2006 2007 2008 2009 2010 2011 2012* 2013* PercentageofhouseholdswithInternetaccess 77 61 46 34 33 7 90 80 70 60 50 40 30 20 10 0 Households without Internet 960 million 108 million 376 million Households with Internet 373 million

- 4. Fixed-broadband prices drop by 82% between 2008 and 2012 Over the past five years, fixed-broadband prices as a share of GNI per capita dropped by 82%. By 2012, fixed- broadband prices represented 1.7% of monthly GNI p.c. in developed countries. In developing countries, fixed- broadband services remain expensive, accounting for 30.1% of average monthly incomes. In 95 countries – including 48 developing countries – the price of a monthly fixed-broadband subscription represented 5% or less of monthly GNI p.c. in 2012. As services are becoming more affordable, fixed-broadband uptake has shown strong growth and by 2013, there are almost 700 million fixed-broadband subscriptions, corresponding to a global penetration rate of 9.8%. In 2013, the total number of fixed-broadband subscriptions in developing countries surpasses those in developed countries. But there is still a wide gap when it comes to fixed-broadband penetration rates, with 6.1% in developing countries (and less than 1% in Sub-Saharan Africa), compared with 27.2% in developed countries. Fixed-broadbandsub-basket as%ofGNIp.c. Fixed-broadbandpenetration Source: ITU World Telecommunication /ICT Indicators database Note: Simple averages. † Preliminary result. * Estimate 2008 2009 2010 2011 2012† 2008 2009 2010 2011 2012* 2013* 2.5 2.0 1.7 1.7 1.7 120 100 80 60 40 20 0 30 25 20 15 10 5 0 115.1 164.6 85.1 59.4 40.359.7 41.8 28.5 21.5 30.1 __ Developing __ World __ Developed __ Developed __ World __ Developing 26 11 1 18 6 19 4 4 7 19 36 Developed Developing 60 50 40 30 20 10 0 22 As fixed-broadband services become more affordable, penetration increases Source: ITU World Telecommunication /ICT Indicators database Note: † Preliminary result, based on 173 countries Fixed-broadband sub-basket value 2012† Numberofcountries By 2012, the majority of countries have reached the Broadband Commission target of offering basic fixed-broadband services at below 5% of monthly GNI p.c. 0-2 2-5 5-8 8-10 10-20 20-30 30-40 40-50 >50 27 10 6

- 5. High-speed access to the internet Differences in broadband speed persist Uptake of high-speed broadband (at least 10 Mbit/s) is highest in some Asian economies, including the Republic of Korea, Hong Kong (China) and Japan, and in several European countries, such as Bulgaria, Iceland and Portugal. In Africa, less than 10% of fixed (wired) broadband subscriptions offer speeds of at least 2 Mbit/s. This is also the case of several countries in Asia and the Pacific, the Americas and some Arab States. CIS Asia & Pacific Americas Africa Arab States 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% ≥10 Mbit/s ≥2 to <10 Mbit/s ≥256 kbit/s to <2 Mbit/s Source: ITU World Telecommunication/ICT Indicators database Note: Refers to advertised speeds. * Data correspond to speed intervals slightly different from the ones defined by ITU. ** Breakdown by speed available only for a part of the total fixed (wired)-broadband subscriptions. † Data include fixed wireless broadband subscriptions Europe Fixed-broadband subscriptions, by speed, early 2012 Korea (Rep.) Hong Kong, China Japan Singapore Macao, China Bangladesh Iran (I.R.) Bhutan Bulgaria Iceland** Portugal United Kingdom Belgium Andorra Denmark Romania Netherlands France Greece Spain Hungary Switzerland Czech Republic Norway*† Israel Finland† Slovenia Slovak Republic Ireland Germany Austria Malta Poland** Estonia Croatia Cyprus† Italy Turkey Bosnia and Herzegovina United States*† Canada*† Brazil Trinidad & Tobago Chile Colombia Ecuador Belize Venezuela Guyana Georgia Russia Azerbaijan Armenia United Arab Emirates Saudi Arabia* Oman Morocco Jordan Tunisia Qatar Egypt Uganda Senegal Namibia Côte d’Ivoire Mauritius Kenya Benin

- 6. Mobile-broadband subscriptions have climbed from 268 million in 2007 to 2.1 billion in 2013. This reflects an average annual growth rate of 40%, making mobile broadband the most dynamic ICT market. In developing countries, the number of mobile- broadband subscriptions more than doubled from 2011 to 2013 (from 472 million to 1.16 billion) and surpassed those in developed countries in 2013. Africa is the region with the highest growth rates over the past three years and mobile-broadband penetration has increased from 2% in 2010 to 11% in 2013. Active mobile-broadband subscriptions, 2007-2013* Continuous high growth of mobile broadband More than 2 billion subscriptions worldwide by end 2013* Denom and classifications employed in these maps do not imply any opinion on the part of the ITU concerning the legal or other status of any territory or any endorsement or acceptance of any boundary. Americas 460 million subscriptions 48% penetration 28% CAGR (2010-2013) CIS 129 million subscriptions 46% penetration 27% CAGR (2010-2013) Europe 422 million subscriptions 68% penetration 33% CAGR (2010-2013) Arab States 71 million subscriptions 19% penetration 55% CAGR (2010-2013) Africa 93 million subscriptions 11% penetration 82% CAGR (2010-2013) Asia-Pacific 895 million subscriptions 22% penetration 45% CAGR (2010-2013) Per100inhabitants Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate Source: ITU World Telecommunication /ICT Indicators database Note: * Estimate 80 70 60 50 40 30 20 10 0 __ Developed __ World __ Developing 20 75 30 2007 2008 2009 2010 2011 2012* 2013*

- 7. By early 2013, the price of an entry-le- vel mobile-broadband plan represents between 1.2-2.2% of monthly GNI p.c. in developed countries and between 11.3- 24.7% in developing countries, depen- ding on the type of service. However,indevelopingcountries,mobile- broadbandservicescostconsiderablyless than fixed-broadband services: 18.8% of monthly GNI p.c. for a 1 GB postpaid computer-based mobile-broadband plan compared to 30.1% of monthly GNI p.c. for a postpaid fixed-broadband plan with 1 GB of data volume. Among the four typical mobile-broad- band plans offered in the market, post- paid handset-based services are the cheapest and prepaid computer-based services are the most expensive, across all regions. A regional comparison highlights that mobile-broadband services remain largely unaffordable in Africa, where the price of a computer-based plan with 1GB of data volume represents on average more than 50% of GNI p.c. Services are most affordable in Europe, where they represent on average less than 2% of GNI p.c. In the Arab States and Asia and the Pacific region, postpaid handset-based services are relatively affordable, accounting for 2.2% and 3.5% of monthly GNI per capita, respectively; prices in the Americas and CIS remain relatively high (5% or above of monthly GNI p.c.) for all mobile-broadband services. Price of mobile-broadband services by region, early 2013† Mobile broadband much more expensive in developing countries But considerably cheaper than fixed-broadband services Price of mobile-broadband services, early 2013† Postpaid handset-based (500 MB) Prepaid handset-based (500 MB) Postpaid computer-based (1 GB) Prepaid computer-based (1 GB) 0 5 10 15 20 25 1.2 7.5 11.3 1.3 11.4 15.7 1.4 2.2 12.7 18.8 17.7 24.7 Price of service as a % of GNI per capita† Source: ITU World Telecommunication /ICT Indicators database Note: Simple averages. † Preliminary result Europe Arab States CIS The Americas Asia & the Pacific Africa Prepaid handset-based (500 MB) 1.1 5.7 5.7 5.9 5.9 38.8 Postpaid handset-based (500 MB) 1.1 2.2 5.6 5.0 3.5 36.2 Prepaid computer-based (1 GB) 1.9 7.4 7.6 11.1 12.6 58.3 Postpaid computer-based (1 GB) 1.2 2.5 7.4 8.0 10.6 54.6 Developed World Developing Source: ITU World Telecommunication /ICT Indicators database Note: Simple averages. † Preliminary result % of GNI per capita

- 8. Bangkok, Thailand 25-27September 2012 10th World Telecommunication/ ICTi n d i c a t o r s MEETING www.itu.int/ict/wtim12 Hosted by Organized by YEARBOOK Telecommunication/ICT Indicators2002–2011 STATISTICS OF I n t e r n a t i o n a l T e l e c o m m u n i c a t i o n U n i o n 2012 YEARBOOKOFSTATISTICS2002–2011 ITU-D Printed in SwitzerlandGeneva – December 2012 ISBN 92-61-00000-0 *00000* Handbookfor the collection of administrative data on Telecommunications/ICT 2011 Printed in Switzerland International Telecommunication Union Telecommunication development Bureau Place des Nations cH-1211 Geneva 20 Switzerland www.itu.int I n t e r n a t i o n a l T e l e c o m m u n i c a t i o n U n i o n HandbookforthecollectionofadministrativedataonTelecommunications/IcT 2011 I n t e r n a t i o n a l T e l e c o m m u n i c a t i o n U n i o n Measuring the Information Society 2012 MeasuringtheInformationSociety 2012 Printed in Switzerland Geneva, 2012 ISBN 978-92-61-14071-7 Photo credits: Shutterstock *37354* For more information: ICT Data and Statistics Division Telecommunication Development Bureau International Telecommunication Union Place des Nations 1211 Geneva 20 - Switzerland indicators@itu.int www.itu.int/ict Printed in Switzerland Geneva, February 2013 © International Telecommunication Union Printed in Switzerland Geneva - April 2011 ISBN 00-00-00000-0 P A R T N E R S H I P O N M E A S U R I N G I C T F O R D E V E L O P M E N T