1. Quarterly Result Update

Infosys Ltd.

Concerns on volume growth and disappointing outlook for FY13

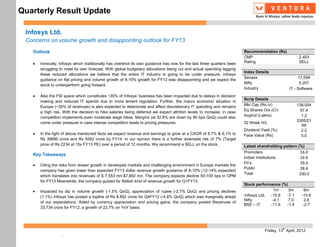

Outlook Recommendation (Rs)

CMP 2,403

Ironically, Infosys which traditionally has overshot its own guidance has now for the last three quarters been Rating SELL

struggling to meet its own forecast. With global budgetary allocations being cut and actual spending lagging

Index Details

these reduced allocations we believe that the entire IT industry is going to be under pressure. Infosys

Sensex 17,094

guidance on flat pricing and volume growth of 8-10% growth for FY13 was disappointing and we expect the

Nifty 5,207

stock to underperform going forward.

Industry IT - Software

Also the FSI space which constitutes ~35% of Infosys’ business has been impacted due to delays in decision

Scrip Details

making and reduced IT spends due to more lenient regulation. Further, the macro economic situation in

Europe (~30% of revenues) is also expected to deteriorate and affect discretionary IT spending and remains Mkt Cap (Rs cr) 138,004

a high risk. With the decision to hike salaries being deferred we expect attrition levels to increase, in case Eq Shares O/s (Cr) 57.4

competition implements even moderate wage hikes. Margins (at 32.8% are down by 90 bps QoQ) could also AvgVol (Lakhs) 1.2

3305/21

come under pressure in case intense competition leads to pricing pressures. 52 Week H/L

69

Dividend Yield (%) 2.2

In the light of above mentioned facts we expect revenue and earnings to grow at a CAGR of 8.7% & 6.1% to Face Value (Rs) 5.0

Rs 39680 crore and Rs 9362 crore by FY14. In our opinion there is a further downside risk of 7% (Target

price of Rs 2234 at 15x FY13 PE) over a period of 12 months. We recommend a SELL on the stock. Latest shareholding pattern (%)

Promoters 16.0

Key Takeaways

Indian Institutions 16.6

FII’s 39.0

Citing the risks from slower growth in developed markets and challenging environment in Europe markets the

Public 28.4

company has given lower than expected FY13 dollar revenue growth guidance of 8-10% (12-14% expected)

Total 100.0

which translates into revenues of $ 7,553 mn-$7,692 mn. The company expects decline 50-100 bps in OPM

for FY13 Meanwhile, the company guided for flattish kind of revenue growth for Q1FY13.

Stock performance (%)

Impacted by dip in volume growth (-1.5% QoQ), appreciation of rupee (-2.7% QoQ) and pricing declines 1m 3m 6m

(1.1%) Infosys has posted a topline of Rs 8,852 crore for Q4FY12 (-4.8% QoQ) which was marginally ahead Infosys Ltd. -15.6 -7.1 -10.8

Nifty -4.1 7.0 2.6

of our expectations. Aided by currency appreciation and pricing gains, the company posted Revenues of

BSE – IT -11.6 -1.4 -2.7

33,734 crore for FY12, a growth of 22.7% on YoY basis.

th

Friday, 13 April, 2012

.

2. Quarterly Result Update

Operating margins during the current quarter remained under pressure at 32.8% (-90 bps QoQ). This was

largely attributable to currency losses, pricing decline and lower utilisation rates. Considering the macro

environment the company has delayed wage hike decision to second half of FY13. Loss on operating front

was compensated by higher other income which grew by 47.5% on sequential quarter basis to Rs 662 crore

on account of higher interest income. As result of this Net Profit for the current quarter declined by 2.4% QoQ

to Rs 2,316 crore.

In terms of industrial segments the growth of BFSI segment (-4.6% QoQ) remained under pressure on

account of slow decision making and relaxation of banking regulatory norms especially in European

region.Driven by strong execution from Auto segment Manufacturing posted a QoQ growth of 2.2%.

Meanwhile Retail, Logistics, CPG & Life Sciences segments degrew by 2.9% on sequential quarter basis.

Energy & Utilities, Communications and Services also remained subdued with sequential degrowth of 0.3%.

With addition of 52 new clients, the number of active clients has reached 694 by end of Q3FY12. During the

current quarter company signed 5 large deals which also included 3 deals from North American geography.

Utilization rate excluding trainees stood at 67.2%, a decline 220bps on sequential quarter basis. Hiring at

gross level for FY12 stood at 45,605, which was aggressive as compared against guidance of 45,000.

Attrition rate also improved by 70 bps on sequential quarter basis to 14.7%which is encouraging sign for the

company.

th

Friday, 13 Apr, 2012

7. Quarterly Result Update

Revenue Break up by Industry Verticals

Quarter ended 12 Months

Revenue by Industry Mar 31, 2012 Dec 31, 2011 Mar 31, 2011 Mar 31, 2012 Mar 31, 2011

% % % % %

Insurance, banking & financial

Services 34.3 35.3 35.7 35.1 35.9

Banking & financial services 27.4 27.9 28.5 27.9 27.8

Insurance 6.9 7.4 7.2 7.2 8.1

Manufacturing 21.3 20.4 20.4 20.5 19.6

Retail & Life Sciences 22.9 23.1 21.4 23 20.5

Retail & CPG 15.8 15.2 14.5 15.7 14.2

Transport & Logistics 1.6 2 2.1 1.8 1.9

Life Sciences 3.9 4.1 3.7 3.9 3.4

Healthcare 1.6 1.8 1.1 1.6 1

Energy & Utilities Communication

Services 21.5 21.2 22.5 21.4 24

Energy & Utilities 6.1 6 5.8 5.9 6.1

Telecom 10.1 9.8 11.9 10.2 12.9

Others 5.3 5.4 4.8 5.3 5

Total 100 100 100 100 100

th

Friday, 13 Apr, 2012

8. Quarterly Result Update

Break up of Onsite & Offsite Revenues and Utilization levels

Quarter ended 12 Months

Effort and Utilization Mar 31, 2012 Dec 31, 2011 Mar 31, 2011 Mar 31, 2012 Mar 31, 2011

% % % % %

Effort

Onsite 24.6 24.8 24.6 25.0 24.2

Offshore 75.4 75.2 75.4 75.0 75.8

Revenue

Onsite 49.6 49.5 49.3 49.9 49.2

Offshore 50.4 50.5 50.7 50.1 50.8

Utilization

Including trainees 67.2 69.9 68.4 69.2 72

Excluding trainees 73 77.4 75.2 75.6 78.9

Break up of revenues by Service Verticals

Quarter ended 12 Months

Revenue by Service offering Mar 31, 2012 Dec 31, 2011 Mar 31, 2011 Mar31, 2012 Mar31, 2011

% % % % %

Services

Business IT Services 62.7 63.6 61.8 63 62.8

Application Development 16.9 17.1 16.1 16.8 16

Application Maintenance 20.9 21.8 22 21.6 22.9

Infrastructure Management Service 6.2 6.1 6.1 6.0 6.3

Testing Services 7.8 7.9 7.3 7.9 7.5

Business Process Management Service 3.4 3.6 2.4 3.4 2.4

Product Engineering Services 4.8 4.4 4.9 4.6 4.9

Others 2.7 2.7 3 2.7 2.8

Consulting & System Integration 31.1 30.6 31.7 31.2 31.2

Products, Platforms and Solutions 6.2 5.9 6.5 5.8 6

Products 4.4 4.8 5.4 4.6 4.9

BPM Platform 1.4 0.8 0.7 0.9 0.7

Others 0.4 0.3 0.4 0.3 0.4

Total 100 100 100 100 100

th

Friday, 13 Apr, 2012

9. Quarterly Result Update

Ventura Securities Limited

Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079

This report is neither an offer nor a solicitation to purchase or sell securities. The information and views expressed herein are believed to be reliable, but no

responsibility (or liability) is accepted for errors of fact or opinion. Writers and contributors may be trading in or have positions in the securities mentioned in their

articles. Neither Ventura Securities Limited nor any of the contributors accepts any liability arising out of the above information/articles. Reproduction in whole or

in part without written permission is prohibited. This report is for private circulation.

th

Friday, 13 Apr, 2012