Alternative credit scoring of underbanked consumers

Lending solutions leverage on emerging technologies to simplify the lending process and to increase the accessibility of lending services. Lending solution encompasses functions like credit scoring, AI deployment, alternative lending solutions and intuitive mobile solutions for lending. The solution enables lending companies to perform credit scoring through the consumer’s digital footprint, allowing the financial institution to create accurate scorecards of consumers that the financial institution have limited information on. The solution increases the loan approval rate to 48% higher than traditional loan processing at 39% less risk, allowing financial institution to optimize their lending portfolio. The credit rating process is also shortened, from days to minutes, increasing the speed of loan approvals. Find out more at www.ey.com/sg/fintechhub. For enquiries, contact us via email at fintech@sg.ey.com.

Recommended

Recommended

More Related Content

More from EY

More from EY (20)

Recently uploaded

Recently uploaded (20)

Alternative credit scoring of underbanked consumers

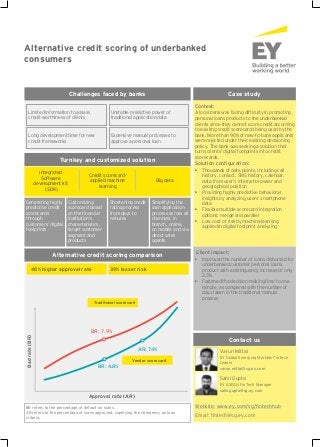

- 1. Alternative credit scoring of underbanked consumers Case study Context: A local bank was facing difficulty in promoting personal loans products to the underbanked clients since they cannot score credit according to existing credit scorecards being used by the bank. More than 90% of new-to-bank applicants were rejected under their existing decisioning policy. The bank was seeking a solution that turns clients' digital footprints into credit scorecards. Solution configuration: • Thousands of data points, including call history, contact, SMS history, calendar, data from user’s internet browser and geographical position • Providing highly predictive behavioral insights by analyzing users’ smartphone data • Flexible multiple scorecard integration options: merge and parallel • Low cost of risk by machine learning applied in digital footprint analyzing Client impact: • Improved the number of loans disbursed for underbanked customer personal loans product with a delinquency increase of only 2.3% • Fastened the decision-making time to one minute, as compared with the number of days taken in the traditional manual process Contact us Varun Mittal EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com Challenges faced by banks Limited information to assess credit-worthiness of clients Unstable predictive power of traditional application data Long development time for new credit frameworks Expensive manual processes to approve a personal loan Turnkey and customized solution Integrated Software development kit (SDK) Credit scorecard- applied machine learning Big data Generating highly predictive credit scorecards through customers’ digital footprints Customizing scorecard based on the financial institution’s characteristics, target customer segment and products Shortening credit rating process from days to minutes Simplifying the loan application process across all channels, in branch, online, on mobile and via direct sales agents BR refers to the percentage of default on loans. AR refers to the percentage of loans approved, signifying the stringency on loan criteria. Alternative credit scoring comparison 48% higher approval rate 39% lesser risk Approval rate (AR) Badrate(BR) BR: 7.9% BR: 4.8% AR: 74% Traditional scorecard Vendor scorecard Website: www.ey.com/sg/fintechhub Email: fintech@sg.ey.com Sahil Gupta EY ASEAN FinTech Manager sahil.gupta@sg.ey.com

- 2. EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. © 2018 EYGM Limited. All Rights Reserved. EYG no. 011378-18Gbl ED None. This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice. ey.com