EY Studie: Top F&E-Unternehmen in Osterreich

•

0 likes•285 views

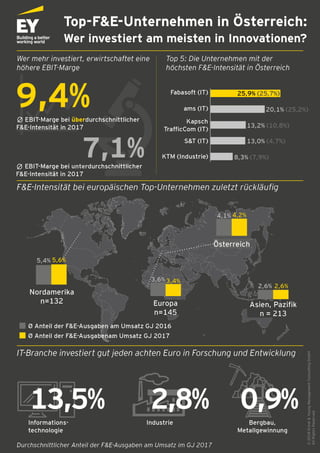

Welche Unternehmen investieren am meisten in Innovationen?

Report

Share

Report

Share

Download to read offline

Recommended

Recommended

More Related Content

More from EY

More from EY (20)

EY Price Point: global oil and gas market outlook (Q4, October 2020)

EY Price Point: global oil and gas market outlook (Q4, October 2020)

Liquidity for advanced manufacturing and automotive sectors in the face of Co...

Liquidity for advanced manufacturing and automotive sectors in the face of Co...

IBOR transition: Opportunities and challenges for the asset management industry

IBOR transition: Opportunities and challenges for the asset management industry

Fusionen und Übernahmen dürften nach der Krise zunehmen

Fusionen und Übernahmen dürften nach der Krise zunehmen

EY Price Point: global oil and gas market outlook, Q2, April 2020

EY Price Point: global oil and gas market outlook, Q2, April 2020

Trotz Rekordumsätzen ist die Stimmung im Agribusiness durchwachsen

Trotz Rekordumsätzen ist die Stimmung im Agribusiness durchwachsen

Deutschlands börsennotierte Unternehmen werden weiblicher

Deutschlands börsennotierte Unternehmen werden weiblicher

Paradigm shift in supply chain management for chemical operating models

Paradigm shift in supply chain management for chemical operating models

Bezpieczny Podatnik - Bezpieczne ulgi podatkowe 2019.pdf

Bezpieczny Podatnik - Bezpieczne ulgi podatkowe 2019.pdf