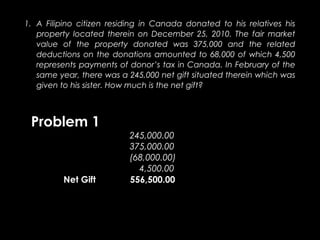

1. 1. A Filipino citizen residing in Canada donated to his relatives his

property located therein on December 25, 2010. The fair market

value of the property donated was 375,000 and the related

deductions on the donations amounted to 68,000 of which 4,500

represents payments of donor’s tax in Canada. In February of the

same year, there was a 245,000 net gift situated therein which was

given to his sister. How much is the net gift?

Problem 1

245,000.00

375,000.00

(68,000.00)

4,500.00

Net Gift 556,500.00

2. 2. Calonzo, Filipino, widower, residing in Lucena City made the

following donations:

June 4- to his sister,Cabaroray, properties worth 125,000. Cabaroray is

now an American citizen residing in Los Angeles, California.

To the Philippine National Library, hidden treasure with interest to

arts, worth 300,000.

July 4- to the University of the Philippines, cash of 160,000 for

scholarship to deserving students.

To Cababaero, legitimate son, 2,000 shares of Benguet

Consolidated Mining which was bought at 100 per share but

having a book value of 75 per share, average price of 110, now

selling at 80, lowest price 105 and highest price 135.

Compute for the donor’s tax due on the July 4 donation.

3. Problem 2

Jun 4 Cabaroray 125,000.00

Nat'l Lib 300,000.00

Gross Gift 425,000.00

Deductions (300,000.00)

Net Gift 125,000.00

Tax at 100,000 -

Excess at @% 500.00

Donor's Tax 500.00

Jul 4 UP 160,000.00

Cababaero

2,000 @ 80 160,000.00

Gross Gift 320,000.00

Deductions -

Net Gift 320,000.00

Net Gift, Previous 125,000.00

Aggregate Net Gift 445,000.00

Tax at 200,000 2,000.00

Excess at 4% 9,800.00

Donor's Tax, Total 11,800.00

Donor's Tax, Previous (500.00)

Donor's Tax, Current 11,300.00

4. 3. Mr. and Mrs. Pano donated the following communal properties

(unless otherwise specified)

April 12- to Wilda, legitimate child, on account of marriage. The

property with a fair market value of 800,000 is located in Naga City.

To Acuna, capital property located in the United States valued at

150,000. The donor’s tax paid in U.S was 7,000.

Sept 7- to Sigue, legitimate chld, property in Manila worth 175,000

Required: Compute the donor’s taxes payable by each spouse.

5. Problem 3

Mr. Pano Mrs. Pano

April 12 400,000.00 400,000.00

150,000.00

Gross Gift 550,000.00 400,000.00

Deductions (10,000.00) (10,000.00)

Net Gift 540,000.00 390,000.00

Tax at 200,000 2,000.00

Excess at 4% 7,600.00

Donor's Tax 9,600.00

Tax at 500,000 14,000.00

Excess at 6% 2,400.00

Donor's Tax 16,400.00

Tax Credit

(150/540 ) x 16,400

vs 7, 000 (4,556.00)

Donor's Tax Payable 11,844.00

Sep 7 Gross Gift 87,500.00 87,500.00

Deductions - -

Net Gift 87,500.00 87,500.00

Net Gift, Previous 540,000.00 390,000.00

Aggregate Net Gift 627,500.00 477,500.00

Tax on 500,000 & 200,000 14,000.00 2,000.00

Excess at 6% and 4% 7,650.00 11,100.00

Donor's Tax, Total 21,650.00 13,100.00

Donor's Tax, Previous (11,844.00) (9,600.00)

Donor's Tax, Current 9,806.00 3,500.00

6. Problem 3

Mr. Pano Mrs. Pano

April 12 400,000.00 400,000.00

150,000.00

Gross Gift 550,000.00 400,000.00

Deductions (10,000.00) (10,000.00)

Net Gift 540,000.00 390,000.00

Tax at 200,000 2,000.00

Excess at 4% 7,600.00

Donor's Tax 9,600.00

Tax at 500,000 14,000.00

Excess at 6% 2,400.00

Donor's Tax 16,400.00

Tax Credit

(150/540 ) x 16,400

vs 7, 000 (4,556.00)

Donor's Tax Payable 11,844.00

Sep 7 Gross Gift 87,500.00 87,500.00

Deductions - -

Net Gift 87,500.00 87,500.00

Net Gift, Previous 540,000.00 390,000.00

Aggregate Net Gift 627,500.00 477,500.00

Tax on 500,000 & 200,000 14,000.00 2,000.00

Excess at 6% and 4% 7,650.00 11,100.00

Donor's Tax, Total 21,650.00 13,100.00

Donor's Tax, Previous (11,844.00) (9,600.00)

Donor's Tax, Current 9,806.00 3,500.00