212MTAMount Durham University Bachelor's Diploma in Technology

Týdenní přehled J&T Banky (16. - 20. května 2011)

1. WEEKLY SUMMARY

May 16 - 20, 2011

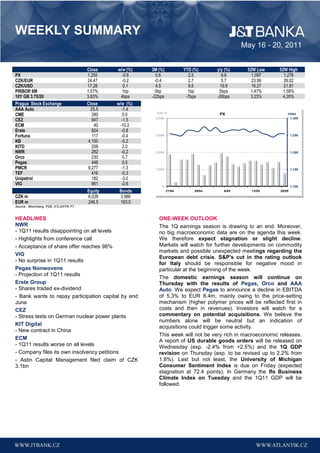

Close w/w (%) 3M (%) YTD (%) y/y (%) 52W Low 52W High

PX 1,255 -0.8 0.6 2.5 9.9 1,097 1,276

CZK/EUR 24.47 -0.2 -0.4 2.7 5.7 23.99 26.02

CZK/USD 17.28 0.1 4.5 9.5 19.9 16.27 21.81

PRIBOR 6M 1.57% 1bp 0bp 1bp 5bps 1.47% 1.58%

10Y GB 3.75/20 3.83% 4bps -22bps -7bps -26bps 3.23% 4.35%

Prague Stock Exchange Close w/w (%)

AAA Auto 25.5 -1.4

CME 390 0.0 CZK m PX Index

CEZ 947 -1.5 4,000 1,300

ECM 40 -10.2

Erste 824 -0.8

Fortuna 117 -0.4 3,000 1,250

KB 4,150 -0.2

KITD 208 2.0

NWR 282 -0.2 2,000 1,200

Orco 230 0.7

Pegas 446 0.5

PMCR 9,277 -1.3 1,000 1,150

TEF 416 -0.3

Unipetrol 182 -3.0

VIG 961 -2.6 0 1,100

Equity Bonds 21/04 29/04 6/05 13/05 20/05

CZK m 6,026 3,986

EUR m 246.5 163.0

Source: Bloomberg, PSE, ATLANTIK FT

HEADLINES ONE-WEEK OUTLOOK

NWR The 1Q earnings season is drawing to an end. Moreover,

- 1Q11 results disappointing on all levels no big macroeconomic data are on the agenda this week.

- Highlights from conference call We therefore expect stagnation or slight decline.

- Acceptance of share offer reaches 98% Markets will watch for further developments on commodity

markets and possible unexpected meetings regarding the

VIG

European debt crisis. S&P's cut in the rating outlook

- No surprise in 1Q11 results

for Italy should be responsible for negative mood in

Pegas Nonwovens particular at the beginning of the week.

- Projection of 1Q11 results

The domestic earnings season will continue on

Erste Group Thursday with the results of Pegas, Orco and AAA

- Shares traded ex-dividend Auto. We expect Pegas to announce a decline in EBITDA

- Bank wants to repay participation capital by end of 5.3% to EUR 8.4m, mainly owing to the price-setting

June mechanism (higher polymer prices will be reflected first in

CEZ costs and then in revenues). Investors will watch for a

- Stress tests on German nuclear power plants commentary on potential acquisitions. We believe the

numbers alone will be neutral but an indication of

KIT Digital

acquisitions could trigger some activity.

- New contract in China

This week will not be very rich in macroeconomic releases.

ECM A report of US durable goods orders will be released on

- 1Q11 results worse on all levels Wednesday (exp. -2.4% from +2.5%) and the 1Q GDP

- Company files its own insolvency petitions revision on Thursday (exp. to be revised up to 2.2% from

- Astin Capital Management filed claim of CZK 1.8%). Last but not least, the University of Michigan

3.1bn Consumer Sentiment Index is due on Friday (expected

stagnation at 72.4 points). In Germany the Ifo Business

Climate Index on Tuesday and the 1Q11 GDP will be

followed.

2. EQUITY MARKET – PRAGUE STOCK EXCHANGE

MARKET NEWS

The week No. 20 was marked by volatile trading. The PX Index closed the week at 1,255 points, down 0.8%. Media

reports were all about commodities again, although the commodity markets got relatively stabilized. We must not forget the

arrest of IMF chief Strauss-Kahn, which could complicate things are regards the voting on another rescue package for

relevant European countries, favoured by Strauss-Kahn, and investors' perception of this development. Last but not least,

the IPO of LinkedIn is worth mentioning as its shares posted an increase of over 100% on their first trading day.

KIG Digital was the star of the week (+1.2%, CZK 207.5) on the PSE, still influenced by earnings results and positive

commentaries of the management on future consolidation. In addition, KITD got a large contract in China. By contrast,

ECM was the most declining stock (-11.1%, CZK 40.2). The insolvency proceeding against the company is in progress.

Further steps, taken with an aim to restructure the company, will probably continue to put pressure on the stock.

Index Close w/w (%) 3M (%) YTD (%) y/y (%) 52W Low 52W High

PX 1,255 -0.8 0.6 2.5 9.9 1,097 1,276

Wien (ATX) 2,768 -1.1 -7.2 -4.7 16.1 2,217 3,001

Warsaw (WIG 20) 2,829 0.2 4.7 2.6 23.7 2,270 2,933

Budapest (BUX) 22,625 -3.1 1.1 6.2 3.0 20,221 24,451

Euro Stoxx50 2,854 -1.4 -5.8 1.7 11.1 2,489 3,068

Dow Jones 12,512 -0.7 2.3 8.1 24.3 9,686 12,811

S&P500 1,333 -0.3 0.4 6.0 24.4 1,023 1,364

Nasdaq 2,803 -0.9 0.0 5.3 27.2 2,092 2,874

REPORTED EARNINGS RESULTS

NWR

The earnings results for 1Q11 reported last Wednesday fell short of market expectations on all levels and we expect a

negative market reaction. Only sales came in as expected by market. Since NWR had already published production

volumes and prices in April, the sales were not surprising. In year-on-year comparison, sales were up 17.1% y/y at EUR

384.8m, boosted by growing prices of coal and coke. The price of coking coal reached EUR 159/t in 1Q11 (+62.2% y/y)

and steam coal was sold at EUR 70/t (+11.0% y/y). The price of coke even surged by 74.6% to EUR 337/t. The negative

factor was the proportion of coking coal and steam coal volumes, when the company produced more steam coal at the

expenses of the coking coal, its main commodity.

Operating costs increased to EUR 335.4m (+10.8% y/y), less in comparison with our projection, as we had calculated with

higher personnel costs. Material and energy costs were up 11.1% y/y at EUR 99m, service expenses up 17.2% y/y at

EUR 90.9m and personnel costs increased by 3.5% y/y to EUR 96m.

EBITDA came in at EUR 81.6m (+42.3% y/y), falling short of market expectations of EUR 48.3m by 11.5% and almost in

line with our projection (+2.4%). EBIT of EUR 37.6m (+110% y/y) was below market expectations by 22.1%. We had

expected EBIT of 33.5m due to higher expected costs. The company generated net income of EUR 3.4m, after a loss of

EUR 15.6m in 1Q10, falling short of expectations of EUR 20.8m by 85.6%. We had expected EUR 7.9m. The notable

difference between the market consensus and the actual figure can be ascribed to the items described above. The

difference compared to our estimate is due to higher-than-expected tax.

The management repeated production and sales goals for 2011.

EUR thousand 1Q11 1Q10 y/y cons. J&T

Sales 384,799 328,563 17.1% 384,300 384,576

EBITDA 81,583 57,324 42.3% 92,200 79,683

EBIT 37,644 17,907 110.2% 48,300 33,534

Net income 3,437 -15,635 n.a. 20,800 7,900

Source: NWR, J&T Banka, market

NWR held a conference call to discuss 1Q11 earnings results. The highlights are as follows:

NWR sees strong demand in the region and expects prices of coal to be at high levels in 3Q11.

The trend of lower volumes of coking coal should reverse in the second half of the year when the company

expects a rise in production volumes, in particular in the fourth quarter. The full-year production target of 11mt

3. EQUITY MARKET – PRAGUE STOCK EXCHANGE

coal (the same volumes of steam and coking coal) remains unchanged. In the subsequent year (2012) the

proportion should change to 60:40 in favour of the coking coal.

The Debiensko project in Poland is underway as expected. Mining should be launched in 2015/2016 (2.5mt), and

it is expected that most (80%) of the coal will be coking coal. More information about the project will be

announced in June.

After its reincorporation in Great Britain, NWR should be included in the FTSE index in June as expected.

As to potential acquisitions, NWR is monitoring mostly Polish and Ukrainian markets. The IPO of JSW, the

largest miner of coking coal in the EU, will be the nearest event.

The management also provided information about the outlook. It is confident that the goals for this year are achievable.

Nothing major was said.

VIG

Last Tuesday Vienna Insurance Group (VIG) published its consolidated earnings results for 1Q 2011, which are in

line with our expectations on all levels. Net profit reached EUR 109m, i.e. 7.8% y/y. Gross written premiums increased

by 2.9% to EUR 6,603m, mostly thanks to growth in the non-life insurance segment. Regarding earnings guidance the

company reiterated that this year it expects pre-tax profit to grow by 10% and written premiums to grow in the low single

digits. Overall, we rate the results as neutral. The company again confirmed the stability of its performance. We consider

the affirmed guidance for this year quite conservative and the company should not have any difficulty beating it.

EUR m 1Q 2011 y/y 1Q 2010 J&T Banka e Market

Gross written premiums 2,603 2.9% 2,531 2,620 2,601

Net earned premiums 2,079 1.5% 2,047 2,097 2,170

Investment income 253 -18.4% 310 265 273

Expenses for claims incurred -1,680 -2.8% -1,728 -1,731 -

Operating expenses -457 2.1% -448 -456 -

Profit before tax 143 7.0% 133 138 139

Net profit* 109 7.8% 101 107 106

Source: VIG, projection of J&T Banka; *after minorities

EXPECTED EARNINGS RESULTS

Pegas Nonwovens

Manufacturer of nonwoven textiles Pegas Nonwovens will report 1Q11 results on Thursday 26 May.

Earnings will be significantly impacted by a major increase in polymer price indices. We expect the higher prices to be

reflected in operating expenses at once while the prices of final production should lag behind. Given the firming of the

koruna against the euro we expect a profit on the financial level.

Total sales should be up 19.2% at EUR 41m compared to the same period a year ago. Sales volumes should stay about

the same but we expect increased product prices.

Operating expenses will be affected by higher prices of polymers, the key raw material used by the company. Their price

grew by about 14% in 1Q11. EBITDA should show a decline of 5.3% y/y to EUR 8.4m. Depreciation charges should be

down in comparison with previous quarters (approx. EUR 4m) at EUR 2.5m as Pegas extended the life-span of

manufacturing assets effective from 1 January 2011, thus reducing depreciation and amortisation costs. That should

boost EBIT, which we expect at EUR 5.9m (+23.3% y/y).

Financial items should have a positive impact on the final result, mainly thanks to the FX effect. Thanks to the

appreciation of the koruna against the euro we expect a gain from the revaluation of the euro-denominated debt (EUR

2.5m). Debt service costs should reach EUR 0.9m. The company is projected to post net income of EUR 6.7m in 1Q11.

The 12.0% y/y decline is due to a considerable increase in currency gains in 1Q10.

Besides the earnings figures, investors will be interested in information about a potential acquisition. The management

is expected to cast more light on that during 2Q11 and it could do so at the time of the earnings release.

The target for full-year EBITDA of 2 – 7% should be confirmed.

4. EQUITY MARKET – PRAGUE STOCK EXCHANGE

IFRS cons. (EUR thousand) J&T e1Q11 y/y 1Q10

Sales 41,010 19.2% 34,399

EBITDA 8,372 -5.3% 8,837

margin 20.4% -5.3pps 25.7%

EBIT 5,872 23.3% 4,763

margin 14.3% 0.5pps 13.8%

Net income 6,729, -12.0% 7,650

Source: Pegas Nonwovens, J&T Banka

COMPANY NEWS

NWR

NWR announced that another 2,769,054 shares accepted the share offer. The total rate of acceptance is 259,549,442

of existing A shares, i.e. more than 98% of the A shares issued. Trading in the new shares commenced last Friday (20

May) in London and Prague and today (23 May) in Warsaw. Note that the offer is related to reincorporation to UK and the

subsequent qualification for the FTSE index. We consider the news neutral.

Erste Group

Erste Group's shares went ex-dividend last Tuesday (EUR 0.7 per share; gross div. yield of 2%).

According to Andreas Treichel (CEO of Erste Group), the bank is aiming to repay EUR 1.2bn in state participation

capital by the end of June. In our view, this step should not significantly compromise the bank’s capitalization. However,

given the fact that Erste has had lower capital adequacy than most competitors in the region, the step may slightly

increase market fears from a future capital increase due to Basel III requirements.

CEZ

German environment minister Norbert Roettgen presented a report on the safety of nuclear power plants. Politicians will

base their decision regarding the future of nuclear energy in Germany on this report and the decision should be

made on 6 June. According to the document, Germany needs to improve security at its nuclear plants against external

flooding and airplane crash. The results of stress tests performed on reactors that had been switched off (8 out of 17)

were less favourable than in the case of newer reactors. According to the minister, the results do not give grounds for an

immediate exit from nuclear industry. In our opinion, market has already priced in that the switched-off reactors will not be

restarted. The question whether Germany will fully exit atomic energy by 2022 as announced remains open.

KIT Digital

The company announced that it had signed a contract with a consortium of Chinese televisions to provide a platform

for distributing video content. More details or the size of the transaction were not released. However, we assume that the

contract is quite large enabling the company to penetrate more the Chinese market.

ECM

ECM REI filed its own bankruptcy petition, according to the company's statement. This comes after the insolvency

petitions filed by Ceska sporitelna and Volksbank on grounds of unpaid obligations of ECM were joined by Glancus

Investments and Conseq. ECM said that reorganization through insolvency proceedings would speed up some

transactions and negotiations with creditors. This step is one of the possibilities presented with the release of 2010

results. Please note that trading in shares of a company in insolvency proceedings may be suspended or terminated by

the Prague Stock Exchange.

ECM REI published 1Q11 earnings results last Wednesday before market close. In comparison with 1Q10, the results

further deteriorated on all levels. The operating loss deepened from EUR 2m to EUR 7.1m and the net loss more than

doubled from EUR -6m to EUR -12.4m. The value of assets further declined compared to the end of 2010 while

obligations of the company rose, and therefore the equity value further fell from EUR -73m to EUR -85m. No commentary

on the ongoing insolvency proceedings was given. We consider the results negative.

IFRS, EUR m 1Q11 y/y 1Q10

Net rental and related income -0.8 - 2.0

Income from sales of investment property 0.0 0% 0.0

Revaluation on investment prop. -1.8 - -0.9

Net operating result -7.1 - -2.0

Net financial result -10.5 - -5.0

5. EQUITY MARKET – PRAGUE STOCK EXCHANGE

Net profit -12.4 - -6.0

Source: ECM REI

Astin Capital Management filed a claim totalling CZK 3.1bn against ECM on Friday. ECM was to pay Astin Capital

Management interest of CZK 116m last October and the principal became due last week. Other creditors include Ceska

sporitelna (CZK 194m), Glancus Investments (CZK 140.8m) and Volksbank (CZK 104.8m). ECM wants to resolve its

indebtedness by restructuring. Last week, ECM joined other creditors and filed an insolvency petition against itself.

MARKET IN FIGURES

Market Volume (CZK m) Change (%) (EUR m) Change (%) (USD m) Change (%)

6,026.1 -23.8 246.5 -23.6 350.8 -21.2

Note: Percentage change relative to the average weekly volume over the past six months

Close w/w 3m y/y 52W Weekly volume

(%) (%) rel. (%)* (%) rel. (%)* Low High CZK m rel. (%)

AAA Auto 25.5 -1.4 1.9 1.2 53.7 39.9 15 28 2 -61

CME 390 0.0 16.4 15.7 -19.9 -27.1 311 575 124 -73

CEZ 947 -1.5 17.6 16.9 6.4 -3.2 736 967 2,327 -27

ECM 40 -10.2 -53.8 -54.1 -81.0 -82.7 37 224 4 1

Erste 824 -0.8 -11.0 -11.6 9.8 0.0 642 965 922 5

Fortuna 117 -0.4 13.9 13.2 n.a. n.a. 84 120 85 -90

KB 4,150 -0.2 -5.0 -5.6 23.9 12.7 3,193 4,600 1,372 -30

KITD 208 2.0 -18.5 -19.0 -11.7 -19.6 163 318 54 194

NWR 282 -0.2 1.8 1.2 31.3 19.5 200 313 11 -99

Orco 230 0.7 14.1 13.4 36.6 24.3 110 252 10 -57

Pegas 446 0.5 0.0 -0.6 3.5 -5.8 410 475 39 16

PMCR 9,277 -1.3 -6.8 -7.3 16.7 6.2 7,913 10,801 47 -98

TEF 416 -0.3 2.8 2.2 1.5 -7.7 369 452 347 -48

Unipetrol 182 -3.0 1.6 0.9 -5.5 -14.0 170 229 56 -98

VIG 961 -2.6 -7.6 -8.2 14.1 3.8 790 1,067 16 -49

Note: *Percentage change relative to the index PX.** Percentage change relative to the average weekly volume over the past six months.

Ratios P/E P/Sales EV/EBITDA EV/ Sales Target LT ST

2010 2011e 2010 2011e 2010 2011e 2010 2011e Price Recomm. Outlook

AAA Auto 13.9 n.a. 0.3 n.a. 8.9 n.a. 0.5 n.a. Not rated

CME 14.4 -12.9 1.9 1.8 23.8 12.8 3.5 3.3 USD 25 Buy Neutral

CEZ 10.9 12.2 2.6 2.5 7.8 7.9 3.4 3.3 CZK 940 Buy Neutral

ECM -0.9 n.a. 1.4 n.a. 2.8 n.a. 1.4 n.a. Not rated

Fortuna 14.2 14.3 3.1 3.0 9.7 9.4 3.1 3.0 CZK 127 Buy Neutral

KITD n.a. n.a. 1.2 n.a. 0.0 n.a. 1.2 n.a. Not rated

NWR 13.8 9.4 1.9 1.6 6.6 4.6 1.9 1.6 CZK 308 Buy Buy

Orco 12.9 n.a. 8.0 n.a. 74.0 n.a. 8.0 n.a. Not rated

Pegas 7.9 6.8 1.4 1.2 4.8 4.0 1.4 1.2 CZK 488 Buy Neutral

PMCR 11.4 10.7 2.3 2.0 7.8 7.4 2.3 2.0 Pending Pending Neutral

TEF 10.6 15.7 2.4 2.5 5.8 6.1 2.4 2.5 CZK 430 Hold Neutral

Unipetrol 31.7 11.2 0.4 0.5 6.3 4.3 0.4 0.5 Pending Pending Pending

Ratios P/E P/BV Target LT ST

2010 2011e 2010 2011e Price Recomm. Outlook

KB 11.8 11.2 2.1 2.0 CZK 4,441 Hold Neutral

Erste 12.5 9.5 0.9 0.9 EUR 34.0 Hold Neutral

VIG 12.6 10.5 1.1 1.0 EUR 46.5 Buy Neutral

6. EQUITY MARKET – BRATISLAVA STOCK EXCHANGE

Weekly volume

Close w/w (%) 3M (%) y/y(%) 52W Low 52W High

(EUR ths)

VUB 81.0 1.3 -11.0 -3.2 65.0 95.0 5

SES Tlmače 14.0 0.0 -3.5 -18.8 13.0 17.5 0

OTP 4.00 0.0 -2.4 33.3 2.01 4.10 0

Biotika 18.9 -10.0 -10.1 107.5 9.1 23.2 0

Slovnaft 45.5 0.0 -2.1 -18.7 40.0 58.3 0

BHP 11.2 0.2 1.0 8.0 10.3 11.2 291

TMR 42.3 0.7 3.2 6.3 39.7 42.5 634

SAX Index 230.59 0.0 -2.1 3.4 201 248.53 931

MARKET COMMENT

In the third week of May trading activity in VUB picked up. The shares found support at EUR 80 and most trades were

executed well above it. After climbing to EUR 85 on

SAX Index

Thursday the stock closed the week at EUR 81, i.e. up 255

1.25% w/w. At that price, the P/E multiple is 7, which is 250

quite attractive.

245

TMR added 0.7% last week, closing at EUR 40.30. BHP

gained 0.2% to EUR 11.18. After a recent decline, 240

Slovnaft's shares are still seeking a new market price and

235

no trade was executed last week. Biotika grew by 10% to

EUR 18.90. 230

The SAX Index closed the week at 230.59 points, flat 225

week-on-week. Traded volumes reached EUR 930

thousand. The most traded stock was TMR, followed by 220

22/04 29/04 6/05 13/05 20/05

BHP and VUB.

EUR TMR - Tatry Mountain Resorts EUR BHP - Best Hotel Properties

11.20

42.6

42.4

11.16

42.2

42.0

11.12

41.8

41.6

11.08

41.4

41.2 11.04

22/04 29/04 6/05 13/05 20/05 22/04 29/04 6/05 13/05 20/05

8. FOREX

CZK/EUR USD Koruna EUR

16.0 23.7

The koruna continued weakening against the euro last

week, moving from 24.4 to a 6-week low of 24.51 on Friday. 16.2

Other regional currencies more or less stagnated, not 24.0

16.4

responding to the released macroeconomic data (PPI, current

account). The increased nervousness on financial market was 16.6

probably the decisive factor. 24.3

16.8

We still expect rather calm and stable trading, and the

koruna could weaken further in the short term (24.6). By the 17.0

24.6

end of the summer the koruna could get stabilized around 17.2 USD

24.2-24.6. The long-term outlook remains unchanged and we EUR

expect to see the Czech currency firm to 23.8 by the end of 17.4 24.9

22/04 29/04 6/05 13/05 20/05

the year.

CZK/USD

The koruna was hovering around 17.20 per USD all week. It stopped weakening in connection with only a minimum

change in CZK/EUR and stabilization on the euro-dollar market.

Higher volatility will probably continue and the dollar could continue correcting its losses (17.80?). In the long term

(months) rather than a clear trend we expect to see higher volatility within CZK 16-20 per USD.

USD/EUR

The euro went through certain consolidation after the previous depreciation and moved from 1.410 to 1.434. However,

at the end of the week nervousness returned to financial markets, fuelled by another cut in Greece's rating by Fitch and a

cut in a rating outlook for Italy by S&P. Euro weakened to 1,415, erasing previous weekly gains.

The continuing technical correction and renewed risk regarding the eurozone debt crisis may continue to put pressure

on the euro. The next important level will be 1.38. Data from German economy due on Tuesday (GDP structure, Ifo index)

may be important.

Exchange Rates Close w/w 3M YTD y/y 52W Forward Forward

(%) (%) (%) (%) Low High 1M 6M

CZK/EUR 24.47 -0.2 -0.4 2.7 5.7 24.0 26.0 24.5 24.4

CZK/USD 17.28 0.1 4.5 9.5 19.9 16.3 21.8 17.3 17.3

CZK/GBP 28.06 -0.2 3.8 4.0 6.0 26.9 31.9 28.1 28.1

USD/EUR 1.416 -0.3 -4.8 -6.1 -11.8 1.19 1.48 1.42 1.41