1. Understanding ULIPs and Mutual Funds

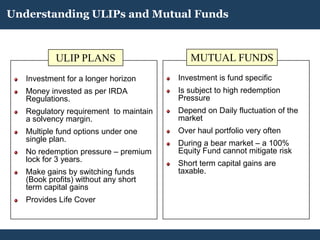

ULIP PLANS MUTUAL FUNDS

Investment for a longer horizon Investment is fund specific

Money invested as per IRDA Is subject to high redemption

Regulations. Pressure

Regulatory requirement to maintain Depend on Daily fluctuation of the

a solvency margin. market

Multiple fund options under one Over haul portfolio very often

single plan. During a bear market – a 100%

No redemption pressure – premium Equity Fund cannot mitigate risk

lock for 3 years. Short term capital gains are

Make gains by switching funds taxable.

(Book profits) without any short

term capital gains

Provides Life Cover

2. What you can sell?

Investment plans

Life Insurance plans

Health Insurance plans

Pension plans

Child Education/Marriage plans

3. Investment business is all about…

• It is all about HEART

• It is all about RELATIONSHIPS

• It is all about BUILDING AWARENESS

• It is all about PATIENCE & PERSISTENCE

• It is all about THINKING LONG-TERM

• It is all about GETTING OFF-TO-FLIER

4. Investment business is not all about…

• It is not about LOGIC

• It is not about HARD-SELLING

• It is not about SEASONAL CYCLES

• It is not about TANGIBLE

• It is not about SALES

6. Life Expectancy in India

The average LIFE EXPECTANCY of

• Indian Men = 63.9 years (from 59.7 in 1991)

• Indian Women = 66.9 years (from 60.9 in 1991)

Most of the insurance companies are pricing their premium based on

decade old mortality tables of LIC (since it has longer history of claims)

and their own claim ratios. The mortality calculations were last revised

in 1995-96.

8. Investments in Equity Market in FY 07-08

Life Insurance Companies = Rs. 55,000 crore

Foreign Institutional Investors = Rs. 53,403 crore

Mutual Funds = Rs. 16,305 crore

9. Health Insurance in India

There are 2 types of health Insurance products now available in India

- Reimbursement Products

- Lump sum Benefit Products

Reimbursement Products Lump sum Benefit Products

You need to incur the expense, which Pays the full sum assured, regardless of the

will be reimbursed. actual expense incurred.

The claim amount is equal to or less than The claim amount is likely to be more than the

the actual expenses actual expenses incurred.

Can be used to pay additional expenses eg

You get what you have spent for the hospital related travel expenses, hospital stay

treatment. for caretaker

Example - Mediclaim Health Investor / Protector / First are Lump

sum Benefit Product.

10. Savings Rate of over 30% of GDP.

Nearly 40% of Household Savings in the form of Physical Assets (residential

houses and white goods)

Gold and Jewellery is not included in the physical assets

Average household savings has gone up from 6.6% in the 50’s to 23.2% in

00’s.

Investments in financial products rose from 1.9% of GDP to 10.8%

The Premium foregone by Policyholders due to lapses was around Rs. 20,500

crore during 02-03 to 06-07.

The industry paid Rs. 20,000 crore in Insurance Commissions on new policies

last year.

14. FHB (Features, How it works and

Benefits)

Selling is based on the concept of FHB.

F H B

What? It does. For me

If need is a problem statement, Benefit is the

solution provided by the product

15. Life Stage and needs at each stage

18-25 25-35 35-45 45-55 55…..

• Money for

• Money for • Money for

child’s

• Money for purchase of providing • Money for

marriage.

purchase of house, assets, children with a child’s higher

• Money for

small assets furniture, vehi good primary education

comfortable

cle. education

retired life

Protection and Protection and Protection and Protection and Protection and

Savings. Savings. Investments. Investments. Pension.

Living Benefits

(protection from health and disabilities)

Tata AIG Life has the right solutions to help customers achieve their goals.

16. Objection vs. Query

Objection Query

An objection is A query is just a

anything the prospect question about the

says which causes a product. It is merely a

roadblock in closing request for more

the sale. information.

Understanding the difference is a key to

successful closing