LEAST-COST-&-RISK LIFECYCLE DELIVERED ENERGY SERVICES

•

3 likes•915 views

147-slide deck used in seminar at the Inter-American Development Bank (IDB), Nov. 12, 2014, Energy Training Workshop. Whereas the IDB has skewed investment and financial support to South and Central American and Caribbean nations into large-scale hydrodams, and large-scale fossil fuel projects (power plants, pipelines), this presentation focuses on the superior least-cost-and-risk strategy based on end-use efficiency gains, onsite and distributed microgrids, powered with solar and wind power.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Similar to LEAST-COST-&-RISK LIFECYCLE DELIVERED ENERGY SERVICES

Similar to LEAST-COST-&-RISK LIFECYCLE DELIVERED ENERGY SERVICES (20)

More from Michael P Totten

More from Michael P Totten (20)

Recently uploaded

Recently uploaded (20)

LEAST-COST-&-RISK LIFECYCLE DELIVERED ENERGY SERVICES

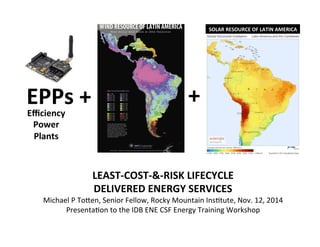

- 1. SOLAR RESOURCE OF LATIN AMERICA LEAST-‐COST-‐&-‐RISK LIFECYCLE DELIVERED ENERGY SERVICES Michael P To,en, Senior Fellow, Rocky Mountain Ins:tute, Nov. 12, 2014 Presenta:on to the IDB ENE CSF Energy Training Workshop EPPs + + Efficiency Power Plants

- 2. Summary of Key Points 1. Least-‐Cost-‐and-‐Risk Lifecycle PorLolio of Delivered Energy Services top priority 2. Risks include intrinsic uncertain:es and surprises – climate disrup:on costs, price vola:li:es of fuel, water, pollu:on and emissions, catastrophic accident fat-‐tail probabili:es, destruc:on of ecosystem services, cultural disrup:on 3. End-‐use efficiency gains (Eta, η) vast pool capable of delivering 50 to 75% of new energy services for decades, far cheaper than any supply op:on – integrated design intelligence/knowledge displacing energy resources & materials. 4. Wind power now cheapest supply op:on in countries and regions with wind resources. 5. Solar Photovoltaics (PV) systems now equal to or less than the grid electricity from other sources in 79 countries. Within 60 months (by 2020) – as the scale of deployments grows and the costs con:nue to decline – more than 80% humanity will live in regions where solar will be compe::ve with electricity from other sources. 6. Efficiency, Wind & Solar, once installed, are risk-‐free from price vola:lity over lifecycle given no fuel demand, virtually no water, no pollu:on, waste or emissions in genera:ng and delivering electricity services.

- 3. Natural Gas provides fuel for transportation, electricity, and heat Telecom provides SCADA and communications technologies Transportation provides fuel transport and shipping Electric Power provides energy to support facility operations Water provides water for production, cooling, and emissions reductions Oil provides fuel and lubricants Figure 3. Examples of Critical Infrastructure Interdependencies Adapted from: Rinaldi, Peerenboom, and Kelly (2001)”Identifying, Understanding, and Analyzing Critical Infrastructure Interdependencies” IEEE Control Systems Magazine, December. Available at: http://www.ce.cmu.edu/~hsm/im2004/readings/CII-Rinaldi.pdf. CriZcal Infrastructure Interdependencies Cybersecurity and the North American Electric Grid: New Policy Approaches to Address an Evolving Threat, Bipar:san Policy Center, Feb. 2014

- 4. Threats Landscape: ELECTRIC POWER SECTOR Spectrum of Threats do today. The Chertoff Group was biological, or radiological attacks). As F I G U R E 1 THREAT LANDSCAPE: ELECTRIC POWER SECTOR Source: The Chertoff Group, December 2013 Cyber Attack Physical Attack / Theft Coordinated Physical and Cyber Attack Insider Threat Electromagnetic Interference / EMP Natural Disasters Pandemic Supply Chain Compromise Chemical, Biological or Radiological Attack Nuclear Attack LIKELIHOOD CONSEQUENCE

- 5. UglyGorilla (Chinese) Hack of U.S. UZlity Exposes Cyberwar Threat “This is as big a naZonal security threat as I have ever seen in the history of this country that we are not prepared for,” said U.S. Congressman Mike Rogers (R-‐MI) , chairman, USHR intelligence commiaee. “Your palms get a liale sweaty thinking about what the outcome of those aaacks might have been and how close they actually came.”

- 6. National Security and the Accelerating Risks of Climate Change Military Advisory Board General Paul Kern, USA (Ret.) Brigadier General Gerald E. Galloway Jr., USA (Ret.) Vice Admiral Lee Gunn, USN (Ret.) Admiral Frank “Skip” Bowman, USN (Ret.) General James Conway, USMC (Ret.) Lieutenant General Ken Eickmann, USAF (Ret.) Lieutenant General Larry Farrell, USAF (Ret.) General Don Hoffman, USAF (Ret.) General Ron Keys, USAF (Ret.) Rear Admiral Neil Morisetti, British Royal Navy (Ret.) Vice Admiral Ann Rondeau, USN (Ret.) Lieutenant General Keith Stalder, USMC (Ret.) General Gordon Sullivan, USA (Ret.) Rear Admiral David Titley, USN (Ret.) General Charles “Chuck” Wald, USAF (Ret.) Lieutenant General Richard Zilmer, USMC (Ret.) Pentagon Report: U.S. Military Considers Climate Change a 'Threat MulZplier' That Could Exacerbate Terrorism

- 7. BUILDING A RESILIENT POWER GRID Industry and government are working together to ensure necessary investments—not only to anticipate and prevent possible harm to critical energy supply—but also to ensure a constant focus on building a more resilient grid.

- 8. ENERGY STRATEGIES FOR NATIONAL SECURITY (and profits, jobs, nature and climate) Funded by Dept Defense Civil Defense Preparedness Agency Funded by Department of Defense 1980 2005

- 9. Main Utility Grid PCC Household appliances and electronics DC Coupled Subsystem Modes of Operation: ISLANDED US Dept of Defense Mandated Islandable Microgrids at Military Bases to operate even if Grid Collapses

- 10. RANKING LEAST-‐COST-‐RISK (LCR) DELIVERED ENERGY SERVICES (DES)

- 12. CORE: Efficiency, ProducZvity, IntegraZve Design

- 13. Energy ConsumpZon in the U.S. economy, 2010-‐2050

- 14. Ken Caldeira

- 15. η Eta Efficiency Power Plants (EPPs)

- 16. You’re Telling Me An EE Power Plant Is Just Like A Fossil Power Plant? . 7 • Yes, and it’s less expensive, removes more pollutants, and saves water • Answer these questions to build an EE power plant: – How many MW and MWh? – When and where? – Quantity of tons needed to be removed? Building Energy Efficiency Power Plants: Cu^ng Through the Fog or Why EE Advocates Should Engage Air Regulators, Christopher James, Principal, Regulatory Assistance Project (RAP), ACEEE Summer Study, August 2014

- 17. Efficiency Power Plant (EPP) calculator, Regulatory Assistance Project, h,p://www.raponline.org/featured-‐work/cu^ng-‐ through-‐the-‐fog-‐to-‐build-‐energy-‐efficiency Efficiency Power Plant (EPP) Calculator

- 18. Building Energy Efficiency Power Plants: Cu^ng Through the Fog or Why EE Advocates Should Engage Air Regulators, Christopher James, Principal, Regulatory Assistance Project (RAP), ACEEE Summer Study, August 2014 same principles as our demonstration tool, that could potentially be used by states as part of their future plans. Indeed, many existing tools used by efficiency program administrators would require only modest modifications (and perhaps no modifications in some cases) to provide such functionality. Figure 2. Efficiency power plant planning tool inputs. 17 "End Use" (what the electricity is being used for) Representative installed equipment (also called "Measure") Unit of installed equipment (what are you counting?) Quantity of installed equipment (how many will be installed?) Savings per Unit (kWh/yr) Total Savings (MWh/yr) RESIDENTIAL Residential Cooling ENERGY STAR Central A/C Air Conditioner 756 150 113 Cooking & Laundry CEE Tier 3 Washer Washing Machine 6,830 237 1,619 Lighting CFL Light Bulb 981,130 35 34,340 Refrigeration Recycled Refrigerator Refrigerator 2,127 720 1,531 Space Heating Weatherization One Home 542 1,500 813 Water Heating Low Flow Showerhead Showerhead 3,530 260 918 Other Custom Projects One Home 3,257 1,000 3,257 Total Residential 42,591 COMMERCIAL & INDUSTRIAL A/C Project One C&I Project 623 5,505 3,429 Hot Water Project One C&I Project 139 1,000 139 Industrial Process Project One C&I Project 73 140,000 10,220 Interior Lighting Project One C&I Project 2,621 16,000 41,936 Motors VFD<= 10 HP One C&I Project 1,509 5,400 8,149 Refrigeration Project One C&I Project 147 17,500 2,573 Space Heating Project One C&I Project 112 4,250 476 Ventilation Project One C&I Project 73 13,400 978 Compressed Air Project One C&I Project 62 29,187 1,810 Other Project One C&I Project 540 2,000 1,080 Total Commercial & Industrial 70,789 Enter the quantity for each row in the bright yellow cell in Column E Only change the savings per unit in the light yellow cells in Column F if you have savings estimates that are specific to the service territory you are analyzing What Might an Efficiency Power Plant Look Like?

- 19. EE Power Plant Output by Month 12 Building Energy Efficiency Power Plants: Cu^ng Through the Fog or Why EE Advocates Should Engage Air Regulators, Christopher James, Principal, Regulatory Assistance Project (RAP), ACEEE Summer Study, August 2014 MWh savings 12,000 10,000

- 20. EE Power Plant for a July Day 13 MWhSavings Building Energy Efficiency Power Plants: Cu^ng Through the Fog or Why EE Advocates Should Engage Air Regulators, Christopher James, Principal, Regulatory Assistance Project (RAP), ACEEE Summer Study, August 2014 MWh savings

- 21. Reducing Greenhouse Gases and Improving Air Quality Through Energy Efficiency Power Plants: Cu^ng Through the Fog to Help Air Regulators “Build" EPPs, Chris James and Ken Colburn, Regulatory Assistance Project Chris Neme and Jim Greva,, Energy Futures Group, ACEEE Summer Study, August 2014 Figure 1. Ozone design values 2009-11. Source: EPA 2014b Opportunities to Include Energy Efficiency in Clean Air Act Requirements The EE community can help spur the inclusion of EE in new and revised air quality rules, and promote EE’s role in helping states and air pollution sources comply with such rules, in two principal areas. First, the EE community should assure that EPA rules explicitly include EE as a compliance option. Because many states are expressly prohibited by their state constitutions LocaZons with Air PolluZon Exceeding Clean Air Standards OpportuniZes to include Energy Efficiency in Clean Air Requirements

- 22. New York California USA minus CA & NY Per Capital Electricity Consumption 165 GW Coal Power Plants Californian’s have net savings of $1,000 per family [EPPs] For delivering least-cost & risk electricity, natural gas & water services Integrated Resource Planning (IRP) & Decoupling sales from revenues are key to harnessing Efficiency Power Plants California 30 year proof of IRP value in promoting lower cost efficiency over new power plants or hydro dams, and lower GHG emissions. California signed MOUs with Provinces in China to share IRP expertise (now underway in Jiangsu). Net Savings $165 per capita

- 23. 14 Annual Energy Savings from Efficiency Programs and Standards 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 GWh/year Appliance Standards Building Standards Utility Efficiency Programs at a cost of ~1% of electric bill ~15% of Annual Electricity Use in California in 2003 Arthur H. Rosenfeld, Commissioner California Energy Commission, Successes of Energy Efficiency: The United States and California, Na:onal Environmental Trust, May 2, 2007

- 24. COOL CITIES BENIGN GEOENGINEERING Over 4000 Walmart stores with white roofs, and standard practice since 1990 Reflects away 80% of solar heat SOLAR REFLECTORS

- 25. A Real-‐World Example of Cooling 25 The whitewashed greenhouses of Almeria, Spain have cooled the region by 0.8 degrees Celsius each decade compared to surrounding regions, according to 20 years of weather station data. Source: Google Earth

- 26. Hashem Akbari Arthur Rosenfeld and Surabi Menon, Global Cooling: Increasing World-wide Urban Albedos to Offset CO2, 5th Annual California Climate Change Conference, Sacramento, CA, September 9, 2008, http://www.climatechange.ca.gov/events/2008_conference/presentations/index.html World of Solar Reflecting Cities $2+ Trillion Global Savings Potential, 59 Gt CO2 Reduction 100 m2

- 27. 27 White roofs, cool-‐colored roofs save money and can even avoid the need to air condi:on flat, white pitched, white pitched, cool & colored OLD NEW AC savings ≈ 15% AC savings ≈ 10% AC savings ≈ 5% AC savings ≈ 15% AC savings ≈ 10%

- 28. Temperature and Smog Forma:on 28 Source: Maryland Commission on Climate Change EPA Compliance Std = 75 TransiZon Zone

- 29. Calif Title 24 “Cool Roof” standards • In 2005, California’s “Title 24” energy efficiency standards prescribed white surfaces for low-‐sloped roofs on commercial and large residen:al buildings (apartments, hotels, etc.). Several hot states are following. • In 2008, California prescribed “cool colored” surfaces for steep residen:al roofs in its 5 ho,est climate zones, but not yet Los Angeles. • Other U.S. states & all countries with hot summers ought to follow. 29

- 30. Resources on the web LBNL – Heat Island Group HeatIsland.LBL.gov Global Cool Ci:es Alliance www.GlobalCoolCi:es.org Cool Roofs and Cool Pavements Toolkit www.CoolRoofToolkit.org Art Rosenfeld’s website www.ArtRosenfeld.org 30 Figure 6: Two Cool Roof Installations A cool coating is applied to a dark roof (top), and a cool single-ply membrane roof is unrolled (bottom). Image Source: DIY Advice or coated to make them reflective. Built-Up Roofs consist of a base sheet, fabric reinforcement layers, and a protective surface layer that is traditionally dark. The surface layer can be made in a few different ways, and each has cool options. One way involves embedding mineral aggregate (gravel) in a flood coat of asphalt. By substituting reflective marble chips or gray slag for dark gravel you can make the roof cool. A second way built-up roofs are finished is with a mineral surfaced sheet. These can be made cool with reflective mineral granules or with a factory-applied coating. Another surface option involves coating the roof with a dark asphaltic emulsion. This type can be made cool by applying a cool coating directly on top of the dark emulsion. Modified Bitumen Sheet Membranes are composed of one or more layers of plastic or rubber material with reinforcing fabrics, and are surfaced with mineral granules or with a smooth finish. A modified bitumen sheet can also be used to surface a built-up roof, and this is called a “hybrid” roof. Modified bitumen surfaces can be pre- coated at the factory to make them cool. Spray Polyurethane Foam roofs are constructed by mixing two liquid chemicals together that react and expand to form one solid piece that adheres to the roof. Since foams are highly susceptible to mechanical, moisture, and UV damage, they rely on a protective coating. These coatings are traditionally reflective and offer cool roof performance. Steep Sloped Roofs Shingled Roofs consist of overlapping panels made from any of numerous materials. Fiberglass asphalt shingles, commonly used on homes, are coated with granules for protection. Cool asphalt shingles are use specially coated granules that provide better solar reflectance. While it is possible to coat existing asphalt shingles to make them cool, this is not normally recommended or approved by shingle manufacturers. Other shingles are made from wood, polymers, or metals and these can be coated at the factory or in the field to make them more reflective. Metal shingles are described in the Metal Roofs section that follows. x EPDM stands for ethylene propylene diene M-class, a kind of synthetic rubber. Cool Policies for Cool Cities: Best Practices for Mitigating Urban Heat Islands in North American Cities Virginia Hewitt and Eric Mackres, American Council for an Energy-Efficient Economy Kurt Shickman, Global Cool Cities Alliance June 2014 Report Number U1405 © American Council for an Energy-Efficient Economy and Global Cool Cities Alliance 529 14th Street NW, Suite 600, Washington, DC 20045 Phone: (202) 507-4000 Twitter: @ACEEEDC Facebook.com/myACEEE www.aceee.org www.globalcoolcities.org Best Practices for Mitigating Urban Heat Islands in North American Cities Virginia Hewitt and Eric Mackres, American Council for an Energy-Efficient Economy Kurt Shickman, Global Cool Cities Alliance June 2014 Report Number U1405 © American Council for an Energy-Efficient Economy and Global Cool Cities Alliance 529 14th Street NW, Suite 600, Washington, DC 20045 Phone: (202) 507-4000 Twitter: @ACEEEDC Facebook.com/myACEEE www.aceee.org www.globalcoolcities.org

- 31. HVAC & Electric Motors TUNNELING THROUGH TO LOW-‐E

- 32. Now use 1/2 global power 30-50% efficiency savings achievable w/ high ROI ELECTRIC MOTOR SYSTEMS

- 33. Improvement Over Time 10 0 10 20 30 40 50 60 70 80 90 100 110 1970 1980 1990 2000 2010 2020 2030 NormalizedEUI(1975Use=100) Year Improvement in ASHRAE Standard 90.1 (Year 1975-2013) 90-1975 90A -1980 90.1-1989 90.1- 1999 90.1- 2007 90.1- 2010 90.1-2004 14% 4.5% 0.5% 12.3% 4.5% 18.5% 90.1-2001 90.1- 2013 18.5% 6~8% Improvement in ASHRAE Standard 90.1 (1975-‐2013) PNNL, Building Codes Commercial Landscape, PNNL-‐SA-‐103479, June 2014

- 34. 10 Source: David Goldstein New United States Refrigerator Use v. Time and Retail Prices 0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000 1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 AverageEnergyUseorPrice 0 5 10 15 20 25 Refrigeratorvolume(cubicfeet) Energy Use per Unit (kWh/Year) Refrigerator Size (cubic ft) Refrigerator Price in 1983 $ $ 1,270 $ 462 Arthur H. Rosenfeld, Commissioner California Energy Commission, Successes of Energy Efficiency: The United States and California, Na:onal Environmental Trust, May 2, 2007

- 35. ASHRAE Standard 90.1 Projections 11 Heating and cooling use index based on weighted equipment efficiency requirement changes; Envelope based on typical medium office steel frame wall and window areas with U-factor changes; Lighting power based on building area allowances weighted for U.S. building floor area; Overall Standard 90.1 progress based on PNNL’s analysis. ASHRAE Standard 90.1 ProjecZons to 2030 PNNL, Building Codes Commercial Landscape, PNNL-‐SA-‐103479, June 2014

- 36. Interrelationships IECC adopts 90.1 by reference – designer choice which to use but cannot ‘pick and choose’, must use one or the other only IgCC adopts the IECC by reference but adds criteria to address addiZonal items not covered in the IECC or increases stringency of the IECC IgCC adopts 189.1 by reference – designer choice which to use but cannot ‘pick and choose’, must use one or the other only ASHRAE 189.1 adopts 90.1 by reference but adds criteria to address addiZonal items not covered by 90.1 or increases stringency of 90.1 InterrelaZonships Building Energy Commercial Codes ASHRAE 189.1 ASHRAE 90.1

- 37. ASHRAE--Chiller Plant Efficiency 0.5 (7.0) 0.6 (5.9) 0.7 (5.0) 0.8 (4.4) 0.9 (3.9) 1.0 (3.5) 1.1 (3.2) 1.2 (2.9) NEEDS IMPROVEMENTFAIRGOODEXCELLENT AVERAGE ANNUAL CHILLER PLANT EFFICIENCY IN KW/TON (C.O.P.) (Input energy includes chillers, condenser pumps, tower fans and chilled water pumping) New Technology All-Variable Speed Chiller Plants High-efficiency Optimized Chiller Plants Conventional Code Based Chiller Plants Older Chiller Plants Chiller Plants with Correctable Design or Operational Problems Based on electrically driven centrifugal chiller plants in comfort conditioning applications with 42F (5.6C) nominal chilled water supply temperature and open cooling towers sized for 85F (29.4C) maximum entering condenser water temperature and 20% excess capacity. Local Climate adjustment for North American climates is +/- 0.05 kW/ton kW/ton C.O.P. 0.59 typical Trane Guaranty Source: LEE Eng Lock, Singapore 0.49 Infosys, Bangalore, India 0.59 Trane, Singapore Sources: LEE Eng Lock, Trane, Singapore; Punit Desai, Infosys, Bangalore, India; Tom Hartman, TX, h,p://www.hartmanco.com/

- 38. Source: LEE Eng Lock, Singapore Typical Chiller Plant -- Needs Improvement (1.2 kW per ton)

- 39. Source: LEE Eng Lock, Singapore High Performance Chiller Plant (0.56 kW/t)

- 40. Source: LEE Eng Lock, Singapore HOW? Bigger pipes, 45° angles, Smaller chillers

- 41. Financial Benefits Before After Cooling TonHr/Week 80,000 80,000 System kWH/Week 152,000 47,200 kWh/TonH 1.90 0.59 Energy Savings in % Energy Savings in kWH / Year Energy Savings in $/Year @ $0.20/KWH Water usage per year (M3) 0 34,682 Water Charge per year (New Water @ $1.0/M3) Estimated Total $ Savings per Year Annual Reduction in Carbon Emission per year (Tones) $34,682 $1,055,238 2,724,800 68.95% 5,449,600 $1,089,920 ROI = 29%. Energy Savings over 15 years = S$15M

- 42. ! Making pipes just 50% fatter reduces friction by 86% Pipe%Dia%in% inch% Flow%in% GPM% Velocity% Ft%/sec% Head%loss% S/100S% 6% 800% 8.8% 3.5% 10% 800% 3.2% 0.3% Big Pipe, small pumps Punit Desai, Environmental Sustainability at Infosys Driven by values, Powered by innova:on, InfoSys, presenta:on to RMI, Sept 15, 2014

- 43. 1. Ask for 0.60 kW/RT or better for chiller plant. 2. Ask for performance guarantee backed by clear financial penalties in event of performance shortfall. 3. Ask for accurate Measurement & Verification system of at least +-5% accuracy in accordance to international standards of ARI-550 & ASHRAE guides 14P & 22. 4. Ask for online internet access to monitor the plant performance. 5. Ask for track record. Source: LEE Eng Lock, Singapore Simple Guide to retrofit success 0.50

- 44. design temperature, thus reducing pump system opportunities. Figure 4: US Pumping System Efficiency Supply Curve Cost effective energy saving potential 0 50 100 150 200 250 300 350 400 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000 55,000 CostofConservedElectricity(US$/MWh-saved) Annual Electricity Saving Potential (GWh/yr) Pump System Efficiency Supply Curve for U.S. Industry Average Unit Price of Electricity for U.S Industr in 2008:70.1 US$/MWh* 5 6 8 7 9 10 Cost effective electricity savingpotential: 36,148 GWh/yr Technicalelectricity savingpotential: 54,023 GWh/yr 4 2 1 3 * The dotted lines represent the range of price from the sensitivity analysis- see Section 4.5. NOTE: this supply curve is intended to provide an indicator of the relative cost-effectiveness of system energy efficiency measures at the national level. The cost-effectiveness of individual measures will vary based on site-specific conditions. US Pumping System Efficiency Supply Curve Annual Electricity Saving PotenZal (GWh/yr) Cost of Conserved Electricity ($US/MWh-‐saved) * The do,ed lines represent the range of price from the sensi:vity analysis-‐ see Sec:on 4.5. NOTE: this supply curve is intended to provide an indicator of the rela:ve cost-‐effec:veness of system energy efficiency measures at the na:onal level. The cost-‐effec:veness of individual measures will vary based on site-‐specific condi:ons. Motor Systems Efficiency Supply Curves, UNIDO, UN Industrial Development Organiza:on, December 2010 Equal to 14 natural gas power plants (500MW each)

- 45. RESULTS AND DISCUSSION No. Energy Efficiency Measure Cumulative Annual Electricity Saving Potential in Industry (GWh/yr) Final CCE (US$/MWh- Saved) Cumulative Annual Primary Energy Saving Potential in Industry (TJ/yr) Cumulative Annual CO2 Emission Reduction Potential from Industry (kton CO2 /yr) 1 Isolate flow paths to non-essential or non-operating equipment 10,589 0.0 116,265 6,382 2 Install variable speed drive 23,295 44.5 255,784 14,040 3 Trim or change impeller to match output to requirements 33,279 57.0 365,405 20,057 4 Use pressure switches to shut down unnecessary pumps 36,148 65.7 396,905 21,786 5 Fix leaks, damaged seals, and packing 37,510 84.1 411,855 22,607 6 Replace motor with more energy efficient type 39,084 116.9 429,138 23,555 7 Remove sediment/scale buildup from piping 42,523 126.3 466,906 25,628 8 Replace pump with more energy efficient type 48,954 132.2 537,516 29,504 9 Initiate predictive maintenance program 52,302 189.0 574,280 31,522 10 Remove scale from components such as heat exchangers and strainers 54,023 330.9 593,171 32,559 Table 14: Cumulative Annual Electricity Saving and CO2 Emission Reduction for Pumping System Efficiency Measures in the US Ranked by their Final CCE Table 15: Total Annual Cost-effective and Technical Energy Saving and CO2 Emission Reduction Potential for US Industrial Pumping Systems CumulaZve Annual Electricity Saving and CO2 Emission ReducZon for Pumping System Efficiency Measures in the US Ranked by their Final CCE Motor Systems Efficiency Supply Curves, UNIDO, UN Industrial Development Organiza:on, December 2010

- 46. Hidden treasure: Why energy efficiency deserves a second look Germany introduced an energy tax (the “eco-tax”) in 1999 to encourage energy savings in the private, public Switzerland’s Energy Strategy 2050 framework propo- ses similar measures with compulsory efficiency targets Note: * Estimation for industrial companies, where direct energy costs account for ~5% of total costs Sources: US Department of Energy; Energy Tax Advisory Case Studies; Lawrence Berkeley National Laboratory; Bain analysis Energy consumption Taxes and incentives Operational non-energy costs Input material costs Own generation/load balancing EE invest/ spend Improved profit margin Sales leverage 2.5 2.0 1.5 1.0 0.5 0 ~ 1% ~ 0.5% ~ 0.5% ? ~ 0.5% ~ 0.5% 2% SALESCOST REDUCTION Percentage of net income (averaged over three years) 10%-30% savings in energy costs for typical IG&S companies In most OECD countries, tax measures typically add 30%-50% on top of the expected energy gains Non-energy costs savings typically amount to an additional 50% of energy savings Not quantified 10-30% reduction in suppliers’ energy costs, 50% pass- through Energy efficiency measures with average investment payback of ~1.5 years, when measured against direct energy savings Figure 2: Typical manufacturing companies* can improve their profit margins by 2% within three years Typical manufacturing companies* can improve their profit margins by 2% within 36 months

- 47. LighZng TUNNELING THROUGH TO LOW-‐E

- 48. • 1/4th Total USA Electricity Consumed For LighZng (and associated Cooling to remove heat from lights) • Equivalent to Nearly Half of U.S. Coal Plants • High-‐efficiency LED Luminaires Can Deliver Beaer Quality Light While EliminaZng Need for Half of Coal Plants at a LCOE [Levelized Cost Of Electricity] Lower than current coal plant operaZng costs IlluminaZon Services 1 LED lamp provides life3me light output of more than 1 million candles at frac3on of cost

- 49. Candle consumes about 80 waas (W) of chemical energy to emit 12 lumens of light for about seven and a half hours. Carbon-‐filament bulb used ¼ less energy (60 W), emiaed 15 Zmes as much light (180 lumens), and lasted 133 Zmes as long as the candle. Tungsten filament replaced the carbon one, efficiency soared 4-‐ fold . Tungsten bulb now matched lifeZme output of 8,100 candles, yet the lamp and electricity cost only as much as 14 candles. CFL same lumen output as incandescent, but consumes 75% less electricity & lasts 10 Zmes longer. One CFL now displaces the need for 500,000 candles. LED (Light-‐Emi{ng Diode) lamp provides same lumen output as CFL, but consumes 1/3rd less electricity & lasts 10 Zmes longer. One LED now displaces need for more than 1 million candles.

- 50. 4 Assuming constant lumen demand per square Residential Commercial Industrial Outdoor General Service Incandescent Sectors Decorative Directional Linear Low / High Bay Street / Roadway Parking Building Exterior Submarkets Technologies Incandescent Reflector Halogen CFL Reflector CFL Pin T5 Metal Halide High Pressure Sodium Mercury Vapor LED Lamp LED Luminaire Halogen Reflector CFL T8 T12 Energy Savings Forecast of Solid-‐State Ligh:ng in General Illumina:on Applica:ons, U.S. Department of Energy August 2014 LighZng Landscape

- 51. Energy Savings Forecast of Solid-‐State Ligh:ng in General Illumina:on Applica:ons, U.S. Department of Energy August 2014 BR=Bulged Reflector MR=Mul:faceted Reflector PAR=Parabolic Aluminized Reflector

- 52. © 2012 Strategies Unlimited 27 LED Lighting Market Segmentation LED Lighting Market Luminaires Replacement Lamps A19 /Standard PARS MR16 Candelabras /Globes/ Decorative L F T June13, 2012 The lamp technologies have been categorized as displayed below in Figure 2-1. The categories are based on those used in the 2001 LMC, the categories used in the various data sources, as well as input from members of the technical review committee. Descriptions of each lamp technology can be found in Appendix A. Figure 2-1 Lamp Classification6 Incandescent General Service - A-type General Service - Decorative Reflector Miscellaneous Halogen General Service Reflector LowVoltage Display Miscellaneous Compact Fluorescent General Service – Screw General Service – Pin Reflector Miscellaneous Fluorescent T5 T8 less than 4 foot T8 4 foot T8 greater than 4 foot T8 less than 4 foot T8 4 foot T8 greater than 4 foot T8 U-shaped T12 U-shaped Miscellaneous High Intensity Discharge LED Lamp Miscellaneous Mercury Vapor Metal Halide High Pressure Sodium LowPressure Sodium Other SMART LED DIVERSITY OF LIGHTING APPLICATIONS A-type - Incandescent lamps PARS - parabolic aluminized reflector lamps MR16 - multifaceted reflector halogen bulbs LFT- Linear Fluorescent tubes LED Replacement of: Luminaire

- 53. http://www.lrc.rpi.edu/programs/nlpip/lightinganswers/hwcfl/HWCFL-efficacy.asp Hi-Wattage CFL (55-200 watts) CFL (27-40 watts) Compact Fluorescent Lamp (CFL) (5-26 watts) Mercury Vapor Halogen Infrared Reflecting Tungsten Halogen Incandescent Fluorescent (full-size & U-tube) Electrodeless fluorescent Metal halide High-Pressure Sodium (HPS/HID) White Sodium Smart LEDs (tunable color spectrum) Efficacy of Various Light Sources 1 1 1 1 1 1 1 1 1 2 Low-Pressure Sodium (yellow-orange color) Lumens per Watt ! (lamp plus ballast)

- 54. = Smart! LED 1! 80 watt! LED Smart LED Advantages! Higher Lumens & lower Watts from Fewer lamps Smart LED other benefits - longer lifespan, no mercury, fully dimmable, instant start/restart, less heat, tunable colour spectrum 100k hrs 20k hrs 2k hrs 10k to 20k hrs Luminaire

- 55. Energy Savings Forecast of Solid-‐State Ligh:ng in General Illumina:on Applica:ons, U.S. Department of Energy August 2014 U.S. LighZng Service Forecast 2013 to 2030 (Trillions of Lumen-‐hours) Fluorescent High-‐Intensity Discharge (HID) LED Luminaires LED lamps CFLs

- 56. SEM oF ROD (blue) and CONE (green) cells of the re:na. ROD cells are sensi:ve to low light levels and produce low-‐clarity black and white vision. CONE cells are sensi:ve to higher levels of light and produce sharp, high-‐clarity trichroma:c color Cone Rod LIGHT FACTORY -‐-‐ ReZnal Rods and Cones Cone Rod top-‐down view

- 57. 3 types of light-‐sensi:ve CONE cells create TRI-‐CHROMATIC (or TRI-‐STIMULUS) color – blue, green & red – or short-‐wavelength, medium-‐wavelength and long wavelength sensi:vity, respec:vely. ROD cells mediate no color vision. Mesopic Vision RODs CONEs RODs & CONEs ReZnal SensiZvity ReZnal SensiZvity

- 58. Our visual system consists of a 2-‐receptor system: CONE cells providing vision in bright light (PHOTOPIC vision) ROD cells providing vision in very low levels of light (SCOTOPIC vision) RODS & CONES func:on together at :mes like dusk (MESOPIC vision). 3 types of CONE cells, red, green & blue (TRI-‐ STIMULUS), provide wide range color percep:on in bright light.

- 59. MESOPIC region is where both the rods and cones are func:oning. The lower light level allows the ROD to replenish the light sensi:ve rhodopsin and begin func:oning. The TRI-‐STIMULUS CONE receptors s:ll have enough light to provide some amounts of color vision.

- 60. SCOTOPIC region occurs in very dim light like viewing grass in a moonless night. Here only the RODS are func:oning. The chemicals in the CONES no longer have enough light to respond, thus we no longer see color.

- 61. PHOTOPIC, MESOPIC & SCOTOPIC together allow us to see over a wide range of ligh:ng levels with about 1 or 2 billion :mes (109, nine orders of magnitude) range from the dimmest to the brightest image we can see. Luminous Intensity (Candela per sq meter) 1 Candela =

- 62. Reliance on the lumen (lm) as the sole measure of ligh3ng benefits (lm/m2 and lm/W) can unnecessarily waste energy, increase costs, and reduce safety, security and visibility. U3liza3on of analogous benefit metrics in ligh3ng standards that characterize human visual responses would increase the value of ligh3ng for many applica3ons. BETTER LIGHTING METRICS OpportuniZes with LEDs for Increasing the Visual Benefits of LighZng Mark S. Rea, LighZng Research Center, Rensselaer Polytechnic InsZtute, Troy NY

- 63. Smart LEDs are Tunable ! Along Color Spectrum

- 64. We thus see the future of public lighting as a transition from analog to digital, from fluorescent lightbulbs to solid-state lighting—all connected to an energy grid throug variety of last-mile access technologies (see Figure 1). Figure 1. Moving from “Traditional” to “Intelligent” Lighting Networks. Additional savings can be achieved by incorporating connected controls to the Intern Source: Philips and Cisco, 2012 Moving from “Traditional” to “Intelligent” Lighting Networks source: The Time Is Right for Connected Public Lighting Within Smart Cities, CISCO & Philips, October 2012

- 65. Smart LED RFPs Should Include ! Key Technical Specifications LED photometric testing standards: ! • IES LM-79-08 Light output, efficacy, color for LED products! • IES LM-80-08 Light output over time, temperature for LED packages IES TM-21-11 Extrapolating LM-80 test data to predict life! • IES LM-82-12 Light output, efficacy, color over temperature for light engines! • ANSI/UL 153:2002 (Secs. 124-128A) Methods for in-situ temperature ANSI/UL 1574:2004 (Sec. 54) method (ISTM) testing for EnergyStar! • IP6 Addressable Approved method describing procedures and precautions in performing reproducible measurements of LEDs:! ! – total flux, – electrical power, – efficacy (lm/watt), and – chromaticity! N A N C Y C L A N T O N , P E , F I E S , I A L D L E E D F E L L O W C L A N T O N & A S S O C I A T E S , I N C . B O U L D E R , C O L O R A D O W W W . C L A N T O N A S S O C I A T E S . C O M Streetlighting Guidel and Design Decisio www.clantonassociates.com Questions? www.clantonassociates.com

- 66. BIM EvoluZon BIM Evolution Hand Drawing 2D CAD evolution 3D CAD BIM 3D/4D/5D..XD BIM; Building Informa:on Modeling, but also encompasses Building Intelligence Management

- 67. Neil Calvert, “Why We Care About BIM…,” Direc:ons Magazine, Dec. 11, 2013, h,p://www.direc:onsmag.com/ar:cles/why-‐we-‐care-‐about-‐bim/368436

- 68. • 20% reducZon in build costs (buy 4, get one free!) • 33% reducZon is costs over the lifeZme of the building • 47% to 65% reducZon in conflicts and re-‐work during construcZon • 44% to 59% increase in the overall project quality • 35% to 43% reducZon in risk, beaer predictability of outcomes • 34% to 40% beaer performing completed infrastructure • 32% to 38% improvement in review and approval cycles BIM SIMs

- 69. Neil Calvert, “Why We Care About BIM…,” Direc:ons Magazine, Dec. 11, 2013, h,p://www.direc:onsmag.com/ar:cles/why-‐we-‐care-‐about-‐bim/368436

- 70. Issa, Suermann and Olbina (A) Solar radiation Analysis (B) Daylighting analysis (C) Shading analysis (D) Ventilation and Airflow Analysis Figure 1: Different kinds of analysis performed by Autodesk Ecotect (Source: <www.autodesk.com/revit>) Increase in project Value with increase in BIM details Solar RadiaZon Analysis DaylighZng Analysis Shading Analysis VenZlaZon & Airflow Analysis

- 71. h,ps://www.youtube.com/watch?v=g04-‐G53mbmc 3D, 4D, 5D, 6D, 7D BIM Con:nuous, smarter performance

- 72. Planned vs. Actual Planned vs. Actual

- 73. Building Analytics in action At one client facility running Building Analytics, the preheating coil and cooling coil were operating simultaneously and wasting more than $900 and 80,000 kBTUs on a daily basis. The problem was pinpointed at a leaking chilled water valve that once repaired produced $60,000 in annual savings with ROI in the first month. Mixed air temperature sensor Outdoor air temp “Occupancy” is at set point Return fan status Preheating discharge temperature Heating valve position Cooling valve position Supply air temperature set point Supply fan status Simultaneous heating and cooling Building name: Equipment name: Analysis name: Estimated daily cost savings: Problem: Excess or simultaneous heating and cooling either providing excess heating or cooling or operating simultaneously. Possible causes: and is leaking. > Temperature sensor error or sensor installation error is causing improper control of the valves.

- 74. Issa, Suermann and Olbina 2D 3D 4D 5D Risk Figure 3: Decrease in project risk with the increase in model details VICO Control is a location based virtual construction system that allows the creation of compressed schedules which al- low the user to determine progress by comparing actual productivity to the project schedule. Many BIM models are not able to store information beyond what the building looks like and as such do not allow the user to store info on the construction process. VICO Control allows integrated construction of the whole project and allows the user to link duration and cost in- formation directly to the model. Accordingly the user can instantly see the impact of changes in scope and schedule on the entire project. It links the building model to estimating and scheduling information going from 3D to 5D and allows the user Decrease in project risk with increase in BIM details 6D Cradle-‐to-‐Cradle Facility Lifespan Integra3on 7D Neil Calvert, “Why We Care About BIM…,” Direc:ons Magazine, Dec. 11, 2013, h,p://www.direc:onsmag.com/ar:cles/why-‐we-‐care-‐about-‐bim/368436

- 75. John Boecker, Integra:ve Energy, Water, and Waste Community Design…from vision and concept to prac:cal Implementa:on, Army Net-‐Zero Installa:ons Conference: 19 January 2012 Integrative Design Mantra Everyone Engaging Everything !!!!group Everything Early www.sevengroup.com

- 76. Benchmarking of Infosys buildings Design%target% Units% Exis:ng%(US)% BeXer% Best%prac:ce% Infosys% Delivered(energy(intensity( kBtu/sfYy( 90( 40Y60( <30( <25( LPD:(Design( W/sf( 1.5( 0.8( 0.4Y0.6( 0.4Y0.6( LPD:(Opera3onal( W/sf( 1.5( 0.6( 0.1Y0.3( <0.15( Installed(computers/appliances..( W/sf( 4Y6( 1Y2( <0.5( <0.7( Glazing(RYvalue((center(of(glass)( sfYF0Yh/Btu( 1Y2( 6Y10( ≥20( >5( Window(RYvalue((including(frame)( sfYF0Yh/Btu( 1( 3( 7Y8( >5( Glazing(spectral(selec3vity( Ke(=(Tvis/SF( 1( 1.2( >2.0( >2.0( Roof(solar(absorptance(and(emilance( α,(ε# 0.8,(0.2( 0.4,(0.4( 0.08,(0.97( 0.18,(0.99( Installed(mechanical(cooling( sf/ton( 250Y350( 500Y600( 1200Y1400+( 750(Y(1000( Cooling(designYhour(efficiency( kW/ton( 1.9( 1.2Y1.5( <0.6( <0.59( US India 11 Punit Desai, Environmental Sustainability at Infosys Driven by values, Powered by innova:on, InfoSys, presenta:on to RMI, 09-‐15-‐2014

- 77. Integrated and goal oriented design approach HVAC(Goal( Ligh3ng(Goal( Water(Goal( ! Max envelope heat gain 1.0 W/sqft ! Total building @ 750-1000 sqft/TR ! 25 deg C, 55% RH ! LPD of 0.45 W/sqft ! 90% of building to be day lit > 110 lux ! No Glare throughout the year ! Architects ! Facade Specialists ! IT Specialists ! HVAC Engineers ! Lighting Specialists ! Architects ! Facade Specialists ! Lighting Specialists ! Electrical Designers ! PHE Engineers ! Architects ! Landscape Architects ! Less than 25 LPD for office building ! Zero discharge ! 100% self sufficient T E A M G O A L( 13 Punit Desai, Environmental Sustainability at Infosys Driven by values, Powered by innova:on, InfoSys, presenta:on to RMI, Sept 15, 2014

- 78. und partnerund partner Arena Amazônia Leed Silver World Soccer Stadium 2014 Manaus, Brazil • Brazil ranks among the world’s top 5 countries with LEED-‐cerZfied projects. • 30 million •2 of LEED-‐cerZfied space. • Six were cerZfied for use in the 2014 World Cup Soccer Championships. • Arena Amazônia used a fracZon of the steel (5,700 tons) compared to convenZonal sports and entertainment venues.

- 79. Arena Amazônia State-‐of-‐the-‐art lightweight roof based on the principle of a horizontally oriented spoked wheel. The circular roof structure is comprised of high-‐strength cables connecZng inner “tension rings” at the center of the circle to an outer rim, or “compression ring.” The cable “spokes,” which are allocated at the inner edge of the roof, are Zghtened between the outer compression ring and the tension rings. This creates a lightweight, almost floaZng roof. A secondary steel structure serves as a frame to support the polytetrafluoroethylene (PTFE)-‐coated high-‐strength resilient fiberglass membrane cladding. The roof elements also serve as guaers to collect the large amounts of water expected during the rainy seasons. The design of the guaers facilitates rainwater collecZon to be used in the arena’s plumbing systems.

- 80. by Arup Associates [7], and the Saint-Etienne Métropole's Zénith Rhône-Alpes (fig. 18), by Foster and Partner architectural firme [8] represents a new contemporary interpretation for the Islamic-Arab windcatcher. Both applied the same design concept of capturing the prevailing wind and disperse it around the building. Fig. 17. Kensington cricket ground, ARP Associates [7] Fig. 19. Burj al 2008 by Eckhar The Showe projects in the into the futur behind the he and extensive ventilate the r drawn in from level) and ind shower tower Kensington Oval cricket Stadium, Barbados Designed with tradi:onal Wind Catcher Natural cooling & ven:la:on design by capturing the prevailing wind and dispersing it around the building Design with Nature: Windcatcher as a Paradigm of Natural Ven:la:on Device in Buildings, Dr. Abdel-‐moniem El-‐Shorbagy, Interna:onal Journal of Civil & Environmental Engineering IJCEE-‐IJENS Vol:10 No:03, 2010

- 82. Commercial building energy efficiency supply curve by end use, 2050

- 83. The Federal Energy Regulatory Commission has es:mated that the U.S. could avoid building 188 GWs of power plants, or approximately $400 billion in capital investment, through dynamic peak power controls. Amit Narayan, U:lity and Consumer Data: A New Source of Power in the Energy Internet of Things, GreenTechMedia, Oct 9, 2014, h,p://www.greentechmedia.com/ar:cles/read/U:lity-‐and-‐Consumer-‐Data-‐is-‐a-‐New-‐Source-‐of-‐Power-‐in-‐the-‐Energy-‐Internet-‐o? utm_source=Daily&utm_medium=Headline&utm_campaign=GTMDaily Demand Response (DR)

- 84. Figure 2: U.S Demand Response Potential by Program Type (2019) 0 50 100 150 200 PeakReduction(GW) 0% 5% 10% 15% 20% 25% %ofPeakDemand Other DR Interruptible Tariffs DLC Pricing w/o Tech Pricing w/Tech 38 GW, 4% of peak 82 GW, 9% of peak 138 GW, 14% of peak 188 GW, 20% of peak Business-as- Expanded Achievable Full Usual BAU Participation Participation effect of dynamic pricing over time is dependent on AMI market penetration, which increases throughout the forecast horizon. The more aggressive AMI deployment assumption in the AP and FP scenarios explains why demand response increases more significantly in the later years of those scenarios. It is interesting to compare the relative impacts of the four scenarios. Moving from the BAU scenario to the EBAU scenario, the peak demand reduction in 2019 is more than twice as large. This difference is attributable to the incremental potential for aggressively pursuing nonpricing programs in states that have U.S Demand Response (DR) PotenZal by Program Type (10 year Zmeframe) 2500 Peaking Plants (75MW each) =

- 85. The New Smart Power Plants Example of a networking kits capable of running the industrial Internet-‐of-‐Things (IoT), or Internet-‐of-‐Everything (IoE), and IT-‐based Energy Services

- 86. INTERNET-‐OF-‐EVERYTHING IP Cloud Controlled Wireless Smart Sensor Networks

- 87. Key advantage of IPv6 over IPv4 is large address space. IPv6 address length is 128 bits vs. 32 bits in IPv4. The address space therefore has 3.4×1038 addresses, or 314 trillion trillion trillion addresses (sex:llion). This would be about 100 addresses for every atom on the surface of the earth. IPv6 Internet Protocol version 6

- 88. Dr. Janusz Bryzek, Chair, TSensors Summit, VP, MEMS and Sensing Solu:ons, Fairchild Semiconductor, Roadmap for the Trillion Sensor Universe, Nov. 26, 2013

- 89. e Suite gy rs, nd e r ess Cisco EnergyWise Discovery Service and Optimization Service Cisco EnergyWise Management Software for Distributed Offices and Data Center Core Switches Storage UPSs CPUs PDUsMainframes Blade Servers Virtualized Servers Servers Data Center Gateways Lighting Access Control Systems Video Cameras CRAC HVAC Facilities (BMS partners) VoIP Phones Laptops Macs Thin Clients Access Points Servers Desktops Printers Campus Routers Switches Network Based No Agents! Policy Based and Automated Announcing the new and improved Cisco EnergyWise Suite See, Measure and Manage CISCO EnergyWise Management OpZmizaZon So•ware h,p://www.cisco.com/c/en/us/products/switches/energywise-‐op:miza:on-‐service/index.html

- 91. 9 12 3 6 9 12 3 6 9 Hourly Prices for 7/1/0915¢ 10¢ 5¢ ¢perkWh¢perkWh am pm Prevents PHEVs from charging during peak hours Adjusts space temp. and chilled water temp. set points Dispatches thermal storage or gen-sets in response to loss in solar PV output Throttles servers for non-critical applications Ensures fans do not overcompensate for new CHW set points Provides real-time visibility to building managers Automatically dims lighting Marginal cost of power increases, T&D systems become congested Curtailment signal or real-time price provided by ISO/utility 1 2 3 5 7 8 6 9 10 4 High summer temps drive up cooling loads Example of an Automated Demand Response Event 9

- 92. Control – A “Spectrum” of Demand Response Options Direct Load Control (AC Cycling) Logic, decision making and control can sit with the load-serving entity, the customer, or anywhere between (e.g. a curtailment service provider): Pure Real -Time PriceInterruptible Rate Wholesale Capacity Programs Traditional “Aggregator” Model Critical Peak Pricing Wholesale Energy Programs Voluntary Demand Bidding Central Control Autonomous Control 7 Historical DR has been centrally controlled, but there is a push to the right of the spectrum. Buildings benefit.

- 93. Case Study – Automated Demand Response: Georgia Institute of Technology • Georgia Institute of Technology is on a dynamic hourly tariff from Georgia Power. • Each hour, the building management system reads prices for the next 48 hours from the utility’s web-service feed. • The facilities director sets the price threshold for automated load shedding mode. Observing a 1MW peak load reduction, ~7% of load for participating buildings Savings during initial summer 2006 pilot 10

- 94. SMART SYSTEM INTELLIGENCE ATTRIBUTES

- 95. REMOTE SUPPLY END-‐USE/ONSITE Centralized Distributed Buildings & Vehicle as Nanogrids

- 96. Jim Lazar, The Regulatory Assistance Project, Status of Distributed Genera:on Installa:on and Rate Making In the US, American Public Power Associa:on Workshop, Jan. 13, 2014 Typical DG Advocate View Marginal Cost Perspective: • Value of distributed resource is greater than the than retail rate; • Net-metering results in subsidy to the grid from innovators. 12 Distributed GeneraZon (DG) MulZple System Values

- 97. Wind Power & Solar PV

- 98. Source: International Energy Agency, Energy Technology Perspectives, 2008, p. 366. The figure is based on National Petroleum Council, 2007 after Craig, Cunningham and Saigo. Oil Gas Uranium Coal ANNUAL Wind Hydro Photosynthesis ANNUAL Solar Energy Annual global energy consumption by humans SOLAR PHOTONS ACCRUED IN A MONTH EXCEED THE EARTH’S FOSSIL FUEL RESERVES 1 :me use

- 99. In the USA, cities and residences cover 56 million hectares. Every kWh of current U.S. energy requirements can be met simply by applying photovoltaics (PV) to 7% of existing urban area— on roofs, parking lots, along highway walls, on sides of buildings, and in dual-uses. Requires 93% less water than fossil fuels. Experts say we wouldn’t have to appropriate a single acre of new land to make PV our primary energy source! 15%

- 100. Energy Efficiency & Renewable Energy eere.energy.gov 1 Program Name or Ancillary Text eere.energy.gov WIND AND WATER POWER PROGRAM 1 2013 Wind Technologies Market Report Ryan Wiser and Mark Bolinger Lawrence Berkeley National Laboratory Report Summary August 2014

- 101. 10 U.S. Lagging Other Countries in Wind As a Percentage of Electricity Consumption Note: Figure only includes the countries with the most installed wind power capacity at the end of 2012 Wind as Percentage of a Country’s Electricity ConsumpZon

- 102. WIND AND WATER POWER PROGRAM Wind PPA Prices Have Reached All-Time Lows 50 $0 $20 $40 $60 $80 $100 $120 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 PPA Execution Date Interior (18,178 MW, 192 contracts) West (7,124 MW, 72 contracts) Great Lakes (3,044 MW, 42 contracts) Northeast (1,018 MW, 25 contracts) Southeast (268 MW, 6 contracts) LevelizedPPAPrice(2013$/MWh) 75 MW 150 MW 50 MW

- 103. that the turbine scaling and other improvements to turbine efficiency described in Chapter 4 have more than overcome these headwinds to help drive PPA prices lower. Source: Berkeley Lab Figure 46. Generation-weighted average levelized wind PPA prices by PPA execution date and region Figure 46 also shows trends in the generation-weighted average levelized PPA price over time among four of the five regions broken out in Figure 30 (the Southeast region is omitted from Figure 46 owing to its small sample size). Figures 45 and 46 both demonstrate that, based on our data sample, PPA prices are generally low in the U.S. Interior, high in the West, and in the middle in the Great Lakes and Northeast regions. The large Interior region, where much of U.S. wind project development occurs, saw average levelized PPA prices of just $22/MWh in 2013. USA Wind Power LCOE PPA in 2013 2.5¢/kWH GLOBAL Wind Power LCOE in 2013 6.5¢/kWh Ryan Wiser & Mark Bollinger, 2013 Wind Technologies Market Report, Lawrence Berkeley, August 2014 6¢/kWh 2¢/kWh 4¢/kWh

- 104. WIND AND WATER POWER PROGRAM Recent Wind Prices Are Hard to Beat: Competitive with Expected Future Cost of Burning Fuel in Natural Gas Plants 54 0 10 20 30 40 50 60 70 80 90 100 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 Range of AEO14 gas price projections AEO14 reference case gas price projection Wind 2011 PPA execution (3,980 MW, 38 contracts) Wind 2012 PPA execution (970 MW, 13 contracts) Wind 2013 PPA execution (2,761 MW, 18 contracts) 2013$/MWh Price comparison shown here is far from perfect – see full report for caveats

- 105. WIND AND WATER POWER PROGRAM Turbine Nameplate Capacity, Hub Height, and Rotor Diameter Have All Increased Significantly Over the Long Term 29

- 107. energy.gov/sunshot energy.gov/sunshot Photovoltaic System Pricing Trends Historical, Recent, and Near-Term Projections 2014 Edition David Feldman1, Galen Barbose2, Robert Margolis1, Ted James1, Samantha Weaver2, Naïm Darghouth2, Ran Fu1, Carolyn Davidson1, Sam Booth1, and Ryan Wiser2 September 22, 2014 1National Renewable Energy Laboratory 2Lawrence Berkeley National Laboratory NREL/PR-6A20-62558

- 108. Tracking the Sun VII An Historical Summary of the Installed Price of Photovoltaics in the United States from 1998 to 2013 Galen Barbose, Samantha Weaver and Naïm Darghouth Lawrence Berkeley National Laboratory — Report Summary — September 2014 This analysis was funded by the Solar Energy Technologies Office, Office of Energy Efficiency and Renewable Energy of the U.S. Department of Energy under Contract No. DE-AC02-05CH11231.

- 110. $0 $2 $4 $6 $8 $10 $12 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Installation Year 10-100 kW >100 kW Residential & Commercial PV (Median Values) InstalledPrice(2013$/WDC) Installed prices continued their precipitous decline in 2013 12 Median installed prices fell by $0.7/W (12-15%) from 2012-2013, across the three size ranges shown, and have fallen by an average of $0.5/W (6-8%) annually over the full historical period Note: Median installed prices are shown only if 15 or more observations are available for the individual size range Median prices for systems installed in 2013 (n=50,614): $4.7/W $4.3/W (10-100 kW), $3.9/W (>100kW)

- 111. PARAMETERS SUMMARIES In reality, conditions vary substantially among countries and, as discussed above, the LCOE for a technology is driven every bit as much by the cost of capital and the availability of equipment locally as it is by natural resource availability. This is particularly cost capital can at times be extremely challenging to source and tariffs or other barriers can make the importation of goods challenging. - Industrial power prices vs onshore wind and solar photovoltaic LCOE, 2013 ($/MWh) Source: Bloomberg New Energy Finance Botswana Haiti Guatemala Nigeria Myanmar SierraLeone ElSalvador Coted’Ivoire Bolivia Argentina Jamaica CostaRica India Kenya Venezuela Senegal Pakistan Bangladesh Paraguay Ethiopia Honduras Belize Nepal Trinidad&Tobago Zambia Nicaragua China Peru SouthAfrica Uganda Mexico Indonesia Suriname Rwanda Chile Zimbabwe Malawi Tajikistan Barbados Ghana Colombia Panama Bahamas Dom.Republic Brazil Tanzania Guyana Uruguay SriLanka Ecuador Mozambique 450 400 350 300 250 200 Solar PV LCOE Onshore wind LCOE 150 100 50 0 tial customers in the 55 nations and found they averaged 14.7 cents per kilowatt-hour in 20133 . However, prices were above 15 cents per kilowatt-hour in 20 Climatescope countries and 22 cents in 16 countries. Bloomberg New Energy Finance estimates the levelized cost of residential electricity for solar power at ap- proximately 15 cents per kWh with the LCOE potentially much lower in the sunniest parts of the world. That is, when power sense for a homeowner to install a solar system rather than La:n American & Caribbean na:ons Industrial power prices vs onshore wind & solar PV LCOE 2013 ($MWh)

- 112. PARAMETERS SUMMARY Progress on policy Climatescope surveyed 55 developing nations to get a better un- derstanding of what policy frameworks have been established to date and which may be most effective. Data collection included the creation of policy records now accessible at www.global-climatescope.org. In all, the survey found at least 359 clean energy-supportive poli- cies on the books in these countries today dating back to 2006. Residential power prices vs residential solar photovoltaic LCOE, 2013 ($/MWh) Source: Bloomberg New Energy Finance Barbados Haiti Peru Botswana Guyana Guatemala Nigeria China Argentina Rwanda Colombia Mexico Mozambique SriLanka Kenya SierraLeone Zimbabwe India Suriname ElSalvador Chile SouthAfrica Indonesia Myanmar Nicaragua Ghana Ecuador Zambia Venezuela Senegal Pakistan Tanzania Trinidad&Tobago Tajikistan Dom.Republic CostaRica Malawi Cameroon Ethiopia Jamaica Panama Honduras Bolivia Bahamas Belize Coted’Ivoire Nepal Uruguay Uganda Brazil Paraguay Bangladesh 450 400 350 300 250 200 Residential solar PV LCOE 150 100 50 0 Policies in force by type and year of establishment 64 71 75 Carbon Market Mechanism Debt Finance Mechanism Number of policies La:n American & Caribbean na:ons ResidenZal power prices vs residenZal solar PV LCOE, 2013 ($MWh)

- 113. FIRST SOLAR UZlity-‐Scale Solar PV 2013 LCOE $0.07-‐0.15/kWh* *2013 data, costs depending on irradiance levels, interest rates, and other factors, e.g. development costs, h,p://www.firstsolar.com/en/solu:ons/u:lity-‐scale-‐genera:on Cents/kWh

- 114. *Permi^ng, inspec:on, and interconnec:on costs ** Includes installer and integrator margin, legal fees, professional fees, financing transac:onal costs, O+M costs, produc:on guarantees, reserves, and warranty costs. Jesse Morris et al, REDUCING SOLAR PV SOFT COST, A FOCUS ON INSTALLATION LABOR, Rocky Mountain Ins:itute, 2013, www.rmi.org/ Solar PV roo•op system installed costs vary several-‐ fold from country to country, state to state, depending on pracZces and policies.

- 115. Bloomberg New Energy Finance, 2030 Market Outlook: Solar, June 27, 2014 Global ResidenZal-‐Scale Solar PV System Economics some parts of the Americas have already begun to see uptake of unsubsidised PV systems such as utility-scale PV in Chile. As solar technology gets cheaper we expect households and businesses to increasing opt for solar systems. There will however be opposition from utilities and changing rate structures for consumers. The first signs of this trend can already be observed: in Spain, for example, the government has threatened to impose a tax on electricity generated for auto-consumption, although the final bill is still pending. Ultimately however we don't believe developments such as this will have a material effect on the size of the market in the long term, particularly as the small-scale power storage solutions become increasingly viable. Figure 9: Global residential-scale PV system economics 2014 2025 500 ] 500 450 450 . any 50GW 400 . any 400 Hawaii .Hawaii Denmark 8 8..1350 tit 350 Slovakia Australia INeth. stralia Neth. • "' Slovakia 100GW "' - 100GW Q) Q) 0 Switz.Po 9 0 §. 250 '§. 250 ChileQ) 200 • Chile •a. 8. 200 - "(ij 150 '(ij 150 100 100 50 50 Arabia 0 0 750 1,250 1,750 2,250 750 1,250 1,750 2,250 Irradiation (kWhlkW/year) Irradiation (kWh/kW/year) Source: Bloomberg New Energy Finance. Note: NJ, New Jersey; CA, California. - c:. - !:.. ; <- "' -;: 2014 2025

- 116. RISKS IN RANKING LEAST-‐COST-‐RISK (LCR) DELIVERED ENERGY SERVICES (DES)

- 119. CO2e!budget!for!2°C!Limit! 111! Listed Fossil Fuel Reserves & Resources Global Non-Listed Fossil Fuel Reserves Remaining Available 2°C Carbon Budget Through 2100 2500 2000 1500 1000 500 0 Unburnable Carbon Reserves GtCO2Estimate A significant portion of the world’s fossil fuel reserves will need to remain in the ground in 2050 if we are to avoid catastrophic levels of climate change. Fossil fuel companies, however, continue to develop reserves that may never be used. 1541 987 2098 Fossil Fuel Assets at Risk Unburnable Carbon Reserves If!humanity!is!to!prevent!global!average! temperature!rise!from!exceeding!2°C!,!then! 80%!of!fossil!fuel!assets!(now!owned!by! corporaAons!or!governments)!must!not!be! burned.! ! This!means!leaving!the!majority!in!the! ground!as!stranded!assets,!or!those!that!are! consumed!must!be!done!with!zero!emission! releases,!such!as!carbon!capture!and! storage!(CCS).! ! With!CCS,!both!coal!and!most!gasZfired! power!plants!are!technically!and! economically!unnecessary,!given!robust! compeAAon!that!can!deliver!electricity! services!at!the!leastZcostZandZrisk!LCOE! (levelized!cost!of!electricity).! Chart!source:!CERES!&!CarbonTracker,!Investors!ask!fossil!fuel!companies!to!assess!how!business!plans!fare!in!lowZcarbon!future!ZZ!coaliAon!of!70!investors!worth! $3!trillion!call!on!world’s!largest!oil!&!gas,!coal!and!electric!power!companies!to!assess!risks!under!climate!acAon!and!‘business!as!usual’!scenarios,!Nov!2013!! CO2 budget for 2°C Limit $28 trillion in Stranded Carbon Assets

- 120. 2.2 5.5 27.3 0.0 5.0 10.0 15.0 20.0 25.0 30.0 $40/tCO2 $100 /tCO2 $500/tCO2 cents per kWh ¢ ¢ ¢ AddiZonal Cost per kWh of natural gas-‐generated electricity (at $40, $100 and $500 per metric ton of CO2 fee) Steam Turbine 1.4 3.5 17.7 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0 $40/tCO2 $100 /tCO2 $500/tCO2 cents per kWh Advanced Gas Turbine ¢ ¢ ¢

- 121. Amory Lovins & Imran Sheikh, The Nuclear Illusion, May 2008, www.rmi.org nuclear coal CC gas wind farm CC ind cogen bldg scale cogen recycled ind cogen end-use efficiency CCS Cost of new delivered electricity (US¢/kWh) US current average

- 122. 1¢/kWh 2¢ 47 93 kg Amory Lovins & Imran Sheikh, The Nuclear Illusion, May 2008, www.rmi.org Coal-fired CO2 emissions displaced per dollar spent on electrical services Carbon displacement at various efficiency costs/kWh Keystone high nuclear cost scenario 3¢ 4¢ kg CO2, displaced per 2007 dollar

- 123. ies was expected to decline, at the same time Mexico could see the highest growth rate jump, t from 1.8 percent in the current decade. Figure 31: Electricity in Latin America’s Generation Mix : Based on Ariel Yepes et al., Meeting the Balance of Electricity Supply and Demand in Latin America an ean. World Bank 2010 coal fuel oil natural gas hydro nuclear oil products others 2008 4.6% 8.4% 22.0% 58.6% 2.8% 2.3% 1.3% 2030 7.9% 3.3% 29.4% 50.0% 4.2% 1.2% 4.1% -10% 0% 10% 20% 30% 40% 50% 60% 2008 2030 Based on Ariel Yepes et al., Mee:ng the Balance of Electricity Supply and Demand in La:n America and the Caribbean. World Bank 2010, cited in “La:n America’s Energy Future” by Roger Tissot for the Inter-‐American Development Bank and the Inter-‐American Dialogue Energy Working Paper Series, No. IDB-‐DP-‐252, December 2012. Electricity in LaZn America’s GeneraZon Mix – 2008 and 2030

- 124. America and the Caribbean are rich in natural resources, not only of a renewable n. Since natural resources have historically been primarily harnessed through the blishment of hydro plants, this region can nowadays boost one of the cleanest ricity mixes in the world in terms of GHG emissions. e 1 below shows total installed capacity and hydroelectric share in the region. Figure 1. Installed capacity and hydroelectric share in Latin America (source: IDB, 2013) e the availability and quality of data on the real potential of each of these resources s considerably, the potential for exploiting new renewable energy sources, such as Installed capacity GW (Hydroelectric share %) Installed capacity & hydroelectric share in LaZn America (Le€ Map 2010, Right Map Amazon Dams Opera:ng & Planned) Le€ Map: Carlos Batlle and Juan Roberto Paredes, Analysis of the impact of increased Non-‐ Conven:onal Renewable Energy genera:on on La:n American Electric Power Systems, Tools and Methodologies for assessing future Opera:on, Planning and Expansion, Discussion paper No. IDB-‐DP-‐341, January 2014 Right Map: Dams in Amazonia, h,p://dams-‐info.org/en

- 125. Updated data, Synapse Leakage rates uncertainty Wind, Solar, Efficiency Wind power Solar power End-use Efficiency Assembled and adapted from mul:ple sources GHG Emissions Comparison from different Sources

- 126. Net Emissions from Brazilian Reservoirs compared with Combined Cycle Natural Gas Source: Patrick McCully, Tropical Hydropower is a Significant Source of Greenhouse Gas Emissions: Interim response to the International Hydropower Association, International Rivers Network, June 2004 DAM Reservoir Area (km2) Generating Capacity (MW) km2/ MW Emissions: Hydro (MtCO2- eq/yr) Emissions: CC Gas (MtCO2- eq/yr) Emissions Ratio Hydro/Gas Tucuruí 24330 4240 6 8.60 2.22 4 Curuá- Una 72 40 2 0.15 0.02 7.5 Balbina 3150 250 13 6.91 0.12 58

- 127. concentrations of methane at different reservoir depths, the depth of turbine and spillway intakes, and the type of spillway design. ■ Surface emissions vary widely among different parts of the same reservoir (largely due to changes in depth, exposure to wind and sun, and growth of aquatic plants), and from year to year, season to season, and between night and day. This greatly complicates efforts to develop reliable whole-reservoir estimates from a limited set of samples measured at specific points in the reservoir during specific time periods. Confidence in the measurements themselves is also hampered by the different results obtained through different measuring equipment and techniques, and disagreements over which measuring methods are most appropriate.22 Factors affecting degassing emission volumes include variations in the volume of water discharged, and the proportion of turbined water versus that which is spilled. Length of Annual Ice Cover CO2 Diffusion CH4 Bubbles Decomposition of Flooded Biomass & Soils Wind Forcing Growth & Decay of Aquatic Plants Degassing Water Level Fluctuation Plankton Growth & Decay Carbon Inputs from Watershed Drawdown Vegetation FIGURE 3. SOME KEY FACTORS INFLUENCING RESERVOIR GHG EMISSIONS Hydropower Dam GHG Emissions Can be Significant Some Key Factors Influencing Reservoir GHG Emissions

- 128. 4 TABLE 1. GREENHOUSE GAS EMISSIONS FROM HYDROPOWER PLANTS Hydro plant Power Installed Flooded CO2 CH4 CH4 Total Electricity Reservoir Emissions density capacity area reservoir reservoir degassing emissions generation age per kWh (W/m2 ) (MW) (km2 ) surface surface (Mt gas/yr) (Mt CO2eq/yr) (GWh/yr) (years)§ (gCO2eq/kWh) (Mt gas/yr) (Mt gas/yr) Boreal Sainte-Marguerite 10.38 882 85 0.02 0.000 0.02 2,770 N/A 8 gross Churchill/Nelson 2.80 3,925 1,400 0.22 0.003 0.28 14,000 N/A 20 (Canada) Manic Complex 1.91 5,044 2,645 0.64 0.008 0.80 20,000 N/A 40 La Grande Complex 1.20 15,552 13,000 3.28 0.039 4.10 82,000 N/A 50 Churchill Falls 0.81 5,428 6,705 1.67 0.020 2.09 35,000 N/A 60 Average 3.42 6,166 4,767 1.17 0.014 1.46 30,754 N/A 36 Tropical Tucuruí 1.74 4,240 2,430 9.34# 0.094 0.970 31.56 18,030 6 (1990) 1,751 “reservoir Curuá-Una .56 40 72 0.04# 0.001 0.022 0.51 190 13 (1990) 2,704 net”* (Brazil) Samuel 0.40 216 540 0.22# 0.010 0.030 1.06 530 12 (2000) 2,008 Average 0.90 1,499 1,014 3.20# 0.035 0.341 11.05 6,250 2,154 Balbina 0.08 250 3,150 23.60 0.036 0.034 28.44 970 3 (1990) 29,322 Tropical Petit Saut 0.32 115 365 0.24 0.012 0.023 1.21 470 20 year avg 2,577 gross (French Guyana) including degassing Tropical Xingó 50.00 3,000 60 0.13 0.001 0.15 13,140 4-5 12 gross Segredo 15.37 1,260 82 0.08 0.0003 0.09 5,519 6-7 16 excluding Itaipú 8.13 12,600 1,549 0.10 0.012 0.34 55,188 16-17 6 degassing Miranda 7.65 390 51 0.08 0.003 0.14 1,708 2-3 83 (Brazil) Tucuruí 1.74 4,240 2,430 7.52 0.097 9.55 18,571 14-15 514 Serra da Mesa 0.71 1,275 1,784 2.59 0.033 3.28 5,585 3-4 588 Barra Bonita 0.45 141 312 0.45 0.002 0.50 618 36-37 816 Samuel 0.39 216 559 1.52 0.021 1.97 946 10-11 2,077 Três Marias 0.38 396 1,040 0.42 0.075 1.99 1,734 35-36 1,147 Average 9.43 2,613 874 1.43 0.027 2.00 11,445 14-15 584 Table 1.: Patrick McCully, Fizzy Science, Interna:onal Rivers Network, November 2006 160 to 250 g CO2eq/ kWh *update *update: William Steinhurst, Patrick Knight, and Melissa Schultz, Hydropower Greenhouse Gas Emissions, State of the Research, Synapse, February 14, 2012, www.synapse-‐energy.com Table 1. GHG Emissions from Hydropower Plants

- 129. 2014 2010 2010 2005 COST OF DROUGHT

- 130. 2000-‐2009 2060-‐2069 2030-‐2039 2090-‐2099 Worsening Drought All Century Long

- 131. “We don’t have a robust energy system, and the costs are significant. The cost today is measured in the billions. Over the coming decades, it will be in the trillions. You can’t just put your head in the sand anymore.” U.S. Dept. of Energy Official Jonathan Pershing, 2013 Hurricane Sandy, 2012

- 132. SECURING THE U.S. ELECTRICAL GRID THE HONORABLE THOMAS F. McLARTY III & THE HONORABLE THOMAS J. RIDGE PROJECT CO-CHAIRS Energy Surety Microgrid U.S. Military bases mandated to be “islandable” – capable of operaZng even if grid collapses Power Grid DisrupZon Risks & Threats Human or Technical Error, Cybera,acks, Military A,acts or Terrorism, Climate Disrup:on & Natural Disasters

- 133. A:f Ansar, Bent Flyvbjerg, Alexander Budzier, Daniel Lun Should we build more large dams? The actual costs of hydropower megaproject development. Energy Policy (2014), h,p://dx.doi.org/10.1016/j.enpol. 2013.10.069 6. U.S. Bureau of Reclamation, also see Hufschmidt and Gerin (1970),3 and Merewitz (1973) on the U.S. water-resource con- struction agencies. acquisition and resettlement; design engineerin management services; construction of all civil w ities; equipment purchases. Actual outturn costs real, accounted construction costs determined a Fig. 1. Sample distribution of 245 large dams (1934–2007), across five continents, worth USD 353B (2010 prices). A. Ansar et al. / Energy Policy ∎ (∎∎∎∎) ∎∎∎–∎∎∎4 • ex post outcomes of schedule & cost es:mates of hydropower dams. • Es:mates are systema:cally & severely biased below actual values. • Projects that take longer have greater cost overruns; bigger projects take longer. • Upli€ required to de-‐bias systema:c cost under-‐ es:ma:on for large dams is +99%. 6. U.S. Bureau of Reclamation, also see Hufschmidt and Gerin (1970),3 and Merewitz (1973) on the U.S. water-resource con- struction agencies. The procedures applied to the cost and schedule data here are acquisition and resettlement; design engineering an management services; construction of all civil works ities; equipment purchases. Actual outturn costs are d real, accounted construction costs determined at the project completion. Estimated costs are defined as bud Fig. 1. Sample distribution of 245 large dams (1934–2007), across five continents, worth USD 353B (2010 prices). A. Ansar et al. / Energy Policy ∎ (∎∎∎∎) ∎∎∎–∎∎∎4 Hydropower Dam Cost Overruns

- 134. A:f Ansar, Bent Flyvbjerg, Alexander Budzier, Daniel Lun Should we build more large dams? The actual costs of hydropower megaproject development. Energy Policy (2014), h,p:// dx.doi.org/10.1016/j.enpol.2013.10.069 Fig. 3. Location of large dams in the sample and cost overruns by geography. A. Ansar et al. / Energy Policy ∎ (∎∎∎∎) ∎∎∎–∎∎∎6 “Using the largest and most reliable reference data of its kind and mul:level sta:s:cal techniques applied to large dams for the first :me, we were successful in fi^ng parsimonious models to predict cost and schedule overruns. …in most countries large hydropower dams will be too costly in absolute terms and take too long to build to deliver a posi:ve risk-‐adjusted return unless suitable risk management can be affordably provided.” “Policymakers, par3cularly in developing countries, are advised to prefer agile energy alterna3ves that can be built over shorter 3me horizons to energy megaprojects.” Hydropower Dam Cost Overruns

- 135. Corn ethanol Cellulosic ethanol Wind-battery turbine spacing Wind turbines ground footprint Solar-battery Mark Z. Jacobson, Wind Versus Biofuels for Addressing Climate, Health, and Energy, Atmosphere/Energy Program, Dept. of Civil & Environmental Engineering, Stanford University, March 5, 2007, http://www.stanford.edu/group/efmh/jacobson/E85vWindSol Area to Power 100% of U.S. Onroad Vehicles COMPARISON OF LAND NEEDED TO POWER VEHICLES Solar-battery and Wind-battery refer to battery storage of these intermittent renewable resources in plug-in electric driven vehicles

- 136. Map of basins with assessed shale oil & shale gas formaZons, 2013 Argen:na 2nd largest deposits in world

- 137. Natural Gas, Coal & Oil Fueled Power Plants in LaZn America (30%, 8%, and 4.5%, respecZvely, in 2030) Based on Ariel Yepes et al., Mee:ng the Balance of Electricity Supply and Demand in La:n America and the Caribbean. World Bank 2010, cited in “La:n America’s Energy Future” by Roger Tissot for the Inter-‐American Development Bank and the Inter-‐American Dialogue Energy Working Paper Series, No. IDB-‐DP-‐252, December 2012.

- 138. Natural!Gas!vs.!Coal! A!Climate!PerspecAve! 101! Source:!adapted!from!IEA,!“Golden!Age!of!Gas”!special!report!(Figure!1.5)!! Leakage&rate&(%&of&total&producKon)& RaKo&of&GHG&emissions&of&gas&over&coal& 8%& 7%& 6%& 5%& 4%& 3%& 2%& 1%& 0& 25& 50& 75& 105& 0& 0.5& 1& 1.5& 2& Global&Warming&PotenKal&(GWP)&for&methane&

- 140. Vulnerability!of!Natural!Gas!to!! Higher!Prices!and!VolaAlity! 131! UCS,!Gas!Ceiling,!Assessing!the!Climate!Risks!of!an!Overreliance!on!Natural!Gas!for!Electricity,!Sept.!2013,!Union!of!Concerned!ScienAsts.!! UCS, Gas Ceiling, Assessing the Climate Risks of an Overreliance on Natural Gas for Electricity, Sept. 2013, Union of Concerned Scientsts

- 141. AccounAng!for!VolaAlity! 132! commodity! options.! ! In! fact,! implied! volatility! levels! can! be! derived! from! listed! option!premiums!to!determine!the!magnitude!of!natural!gas!movements!“pricedbin”! by!the!options!market!at!a!given!future!date!(Figure!3).!!For!example,!options!are! currently! pricing! in! a! potential! range! of! $1.18! to! $13.80! per! mmBtu! at! the! 99%! confidence!interval!by!June!2015.!! ! ! ! Figure! 3:! Using! implied! volatility! levels! and! option! premiums! to! determine! future! natural! gas! price! ranges!at!68%,!95%,!and!99%!confidence!intervals! RISK+DISTRIBUTION+ ! Assets!generally!face!two!types!of!risk:!risk!associated!strictly!with!the!underlying! asset!(alpha),!and!risk!correlated!with!the!broader!market!(beta).!!A!positive!beta! value!represents!a!positive!correlation!with!the!broader!market,!whereas!a!negative! $13.80+ + + + + June+2015+ + + + + $1.18+ Potential NYMEX Henry Hub Prices RMI,!UKlity^Scale&Wind&and&Natural&Gas&VolaKlity:&Uncovering&the&Hedge&Value&of&Wind&for&UKliKes&and&Their& Customers,&2012!! Using&implied&volaKlity&levels&and&opKon&premiums&to&determine&future& natural&gas&prices&ranges&at&68%,&95%&and&99%&confidence&intervals.& NYMEX&Henry&Hub&Futures& 68%CI& 99%CI&95%CI&

- 143. Policies!&!Subsidies!promote!highZ Emission!investments!over!ZeroZE!OpAons! 128! Total Global Investments in Renewables Billions of Dollars Invested 2012 Investments in Fossil Fuel Reserves Versus Clean Energy 0 100 200 300 400 500 600 700 $674 $281 Corporate Investments in Developing Fossil Fuel Reserves www.ceres.org www.carbontracker.org Legacy!policies,!subsidies,! and!regulaAons!(or!lack! thereof)!conAnue!to!steer! investments!into!energy! opAons!with!highZemission! output.!!The!IMF!esAmates! $2!trillion!per!year! worldwide!in!subsidies!to! the!fossil!fuel!industry.!! Another!$4!trillion!per!year!in!economic!losses!are!due!to!fossil!fuel! externaliAes!that!go!unpriced!or!unregulated,!according!to!esAmates!by!UN! Finance!IniAaAve.!!This!skewing!of!decisionmaking!creates!uncertainty!as!to! whether!emissions!will!steeply!rise!(BAU)!or!major!policy!changes!will!occur.!! Chart!source:!CERES!&!CarbonTracker,!Investors!ask!fossil!fuel!companies!to!assess!how!business!plans!fare!in!lowZcarbon!future!ZZ!coaliAon!of!70!investors!worth! $3!trillion!call!on!world’s!largest!oil!&!gas,!coal!and!electric!power!companies!to!assess!risks!under!climate!acAon!and!‘business!as!usual’!scenarios,!Nov!2013!!

- 144. Water!&!CCS!impact!by!power!plant! 150! Water and Carbon Capture Impact Source: Gerdes, K.; Nichols, C. Water Requirements for Existing and Emerging Thermoelectric Plant Technologies; DOE/NETL Report 402/080108; U.S. Department of Energy National Energy Technology Laboratory: Morgantown, WV, 2009. 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 Subcritical pc Supercritical pc IGCC – Dry Feed IGCC – Slurry Feed NGCC No Capture 0.52 0.45 0.30 0.31 0.19 With Capture 0.99 0.84 0.48 0.45 0.34 Estimated Water Consumption Increase with CO2 Capture and Compression gal/ kWh % Increase 91 87 61 46 76 pc=!pulverized!coal;!IGCC=!integrated!gasificaAon!combined!cycle!coal!plant;!! NGCCZ!natural!gas!combined!cycle! Gerdes,!K.;!Nichols,!C.!Water!Requirements!for!ExisAng!and!Emerging!Thermoelectric!Plant!Technologies;!DOE/NETL! Report!402/080108;!U.S.!Department!of!Energy!NaAonal!Energy!Technology!Laboratory:!Morgantown,!WV,!2009.!