Model i best practice evaluation worksheet for ia

•

3 likes•2,778 views

The document outlines best practices for internal audit departments across five key areas: roles and structure, people, process, technology, and knowledge. It provides examples of best practice features for each area and a template for departments to evaluate the evidence of these features in their own practices. The template can be used to assess areas as low, medium, or high and identify opportunities for improvement. The document aims to help internal audit departments evaluate their practices against industry standards and enhance their ability to add value through continuous improvement.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Model i best practice evaluation worksheet for ia

Similar to Model i best practice evaluation worksheet for ia (20)

More from Rajeswaran Muthu Venkatachalam

More from Rajeswaran Muthu Venkatachalam (20)

Recently uploaded

Recently uploaded (20)

Model i best practice evaluation worksheet for ia

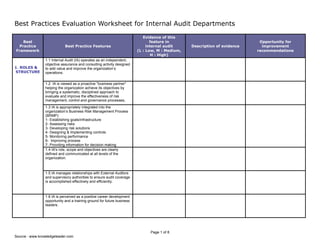

- 1. Page 1 of 8 Source : www.knowledgeleader.com Best Practices Evaluation Worksheet for Internal Audit Departments Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 1. ROLES & STRUCTURE 1.1 Internal Audit (IA) operates as an independent, objective assurance and consulting activity designed to add value and improve the organization’s operations. 1.2 IA is viewed as a proactive "business partner" helping the organization achieve its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes. 1.3 IA is appropriately integrated into the organization’s Business Risk Management Process (BRMP): 1- Establishing goals/infrastructure 2- Assessing risks 3- Developing risk solutions 4- Designing & Implementing controls 5- Monitoring performance 6- Improving process 7- Providing information for decision making 1.4 IA's role, scope and objectives are clearly defined and communicated at all levels of the organization. 1.5 IA manages relationships with External Auditors and supervisory authorities to ensure audit coverage is accomplished effectively and efficiently. 1.6 IA is perceived as a positive career development opportunity and a training ground for future business leaders.

- 2. Page 2 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 1.7 The structure of the IA department is aligned with the business and is effectively communicated to its customers, resulting in efficient service delivery. 1.8 A balanced set of performance measures is used to monitor the timeliness, cost-effectiveness and quality of IA's performance and to drive continuous improvement to the IA organization and audit process. 2. PEOPLE Qualitative 2.1 An appropriate competency model is in place (which defines the skills, knowledge and attributes required of IA professionals to deliver value to customers) to ensure that career and skill development programs are consistent with the business and its needs. 2.2 Career and skill development programs for IA professionals are in place and effective. 2.3 IA professionals are recruited from both traditional and non-traditional (operational) backgrounds to maximize performance and create a diverse, balanced IA organization. 2.4 Policies on training, appraisal, career development, roles and responsibilities, job descriptions, etc. are documented and consistent with corporate policies. 2.5 Regular initiatives are promoted to raise the profile of internal audit, attract and motivate suitably qualified professionals, and reduce IA professionals’ turnover. 2.6 The appraisal process is clearly defined and communicated to auditors. It is used as a means of performance review and to update career and skills development programs.

- 3. Page 3 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 2.7 Succession planning is in place to allow continuity in IA management and the audit process. It is aligned with career development programs. Quantitative 2.8 Training time averages between 60-100 hours per person per year 2.9 Cost of IA department per auditor in USD: - between X and Y (Benchmarks for this information can be obtained from annual GAIN surveys available from the Institute of Internal Auditors) 2.10 Headcount of auditors per 1000 employees : - Close to 5 2.11 Group revenue per auditor in USD : (Benchmarks for this information can be obtained from annual GAIN surveys available from the Institute of Internal Auditors) 3. PROCESS Risk assessment and planning 3.1 A straightforward, “top-down” business risk identification and assessment process drives audit planning. 3.2 The company risk profile is formally and regularly reviewed to ensure it reflects development in the business risk environment and is linked to a rolling audit plan. 3.3 A common language exists across the organization to ensure consistent approach of risks at all level in the organization. 3.4 Major stakeholders (Management, External Auditors, and Audit Committee) are involved in risk assessment and planning.

- 4. Page 4 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 3.5 Management and Audit Committee formally approve the audit plan. 3.6 A systematic approach is in place for planning and scheduling work programs and performance is monitored to allow optimum resources allocation. 3.7 Job scheduling and planning is organized to ensure auditors with the right competencies are assigned to the right job. Audit execution 3.8 Terms of reference, covering issues such as scope, objectives and timing, are agreed with management before each audit begins. 3.9 The audit process, and status of the audit program are effectively communicated to audit customers in order to promote awareness and greater "buy-in" 3.10 Clearly defined standard audit methodologies are in place. 3.11 The format, content and use of working papers and audit files is standardized across the IA organization to maximize efficiency and promote consistency. 3.12 There is a systematic process in place to link business risks to business processes. Evaluation of business controls is based on assessment of these process risks.

- 5. Page 5 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 3.13 The audit process is applied to the whole of the organization's BRMP and is not limited to looking at process controls. 3.14 Best practices (both internal and external) are used for evaluations of controls and recommendations. 3.15 Open communication is maintained with management throughout the audit process. 3.16 A formal closing meeting is held to discuss all open issues with management. 3.17 Self-assessment techniques are used to identify and analyze risks and controls. This helps the audit customers understand how controls help to meet business objectives. 3.18 Knowledge sharing is built into the audit execution process to allow effective contribution by auditors and control and approval by audit management. Reporting and follow-up 3.19 The report approval, sign-off and distribution process is clearly defined and documented. 3.20 Final reports are prepared and issued on site. 3.21 Standard, pre-defined report formats are used to promote a concise, consistent and efficient approach. Report formats reflect audit customer requirements (summary with appropriate level of detail on major issues for Audit Committee, more detailed report for Management).

- 6. Page 6 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 3.22 Issues and recommendations are regularly reported and prioritized using clear and agreed upon criteria (risk importance, ease of implementation, etc.). 3.23 Overall control ratings are assigned, based on audit findings, using a clearly defined rating scale communicated to IA staff and customers. 3.24 Reports include action plans setting responsibilities and target dates embraced by Management. 3.25 Regular follow-up is made by IA to ensure that agreed action plans are implemented. 3.26 There is a clearly defined process to capture customer satisfaction ratings and gather customer feedback on IA's performance to ensure IA services match the needs of the business 4. TECHNOL- OGY 4.1 Communication technology is widely used to support the IA's knowledge sharing process. Technology used by IA is integrated with the company’s technology platform. 4.2 Voting technology is used to facilitate risk and control self-assessment meetings and allow efficient team decision-making. 4.3 Technology is used to facilitate continuous risk and control self-assessment across the organization.

- 7. Page 7 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 4.4 Workflow technology is used to enable more effective and efficient implementation of standard audit processes (planning, electronic workpaper, etc.) 4.5 Data-mining technology is used to allow efficient retrieval and analysis of relevant corporate data for risk analysis. 4.6 Technology is used to capture and integrate audit data sources to provide comprehensive management information to support the BRMP. 4.7 Auditors are equipped with, and trained to use, appropriate technology to increase personal productivity (laptop computers, standard software, modem, printer, etc.). 4.8 Responsibility for maintenance of tools (and license agreements) is given to IT specialists within the company or outside providers if needed. 5. KNOWLEDGE 5.1 Standard, organization-wide knowledge sharing process and technology in place. 5.2 Culture in place that facilitates, encourages and rewards knowledge sharing. The sharing of knowledge is measured. 5.3 Local and remote access available to internal and external knowledge databases and resources that facilitate auditors and audit management in the performance of their duties (best control practices, best practices for auditing, industry specifics, benchmarking information etc).

- 8. Page 8 of 8 Source : www.knowledgeleader.com Best Practice Framework Best Practice Features Evidence of this feature in internal audit (L : Low, M : Medium, H : High) Description of evidence Opportunity for improvement recommendations 5.4 A knowledge manager is appointed to ensure responsibilities are clear and define the process in place to allow contribution in an organized way. 5.5 Responsibilities for controlling the quality of content/knowledge (ensure regular updates and upgrades, additions and consistency within the IA organization) are clearly identified.