Group Case 1 Part 1 Schedules of Cost of Goods Manufactured and C.docx

Case study 1 week 1

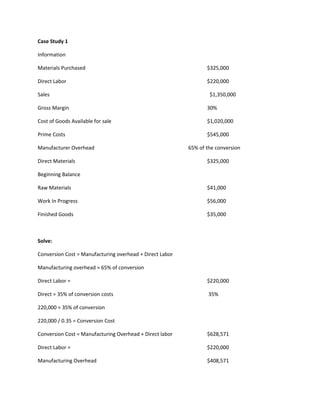

1. Case Study 1

Information

Materials Purchased $325,000

Direct Labor $220,000

Sales $1,350,000

Gross Margin 30%

Cost of Goods Available for sale $1,020,000

Prime Costs $545,000

Manufacturer Overhead 65% of the conversion

Direct Materials $325,000

Beginning Balance

Raw Materials $41,000

Work In Progress $56,000

Finished Goods $35,000

Solve:

Conversion Cost = Manufacturing overhead + Direct Labor

Manufacturing overhead = 65% of conversion

Direct Labor = $220,000

Direct = 35% of conversion costs 35%

220,000 = 35% of conversion

220,000 / 0.35 = Conversion Cost

Conversion Cost = Manufacturing Overhead + Direct labor $628,571

Direct Labor = $220,000

Manufacturing Overhead $408,571

2. Prime Cost = Direct material Cost + Direct Labor Cost

545,000 = Direct Material Cost + 220,000

Direct Material Cost = 545,000 – 220,000

Direct material Cost = 325,000

Therefore,

The Raw Material Cost $325,000

Work In Progress $24,471

Finished Goods Inventory $75,000

3. Solution

Calculating Gross Margin

Sales $135,000

Cost of Goods sold:

Beginning finished goods inventory 35,000

Add: cost of goods manufactured 985,000

--------------

Cost of Goods Available for Sale 1,020,000

Minus:

Ending Finished Goods Inventory 75,000 945,000

--------------- ---------------

Gross Margin $405,000

Gross Margin = 30% ($1,350,000)

Cost of Goods Sold

Beginning Bal. finished goods $35,000

Add:

Cost of goods manufactured 985,000

------------------

Goods available for sale 1,020,000

Less:

Ending bal. finished goods 945,000

------------------

Cost of goods sold $75,000

Total Manufacturing cost

Direct Material Cost $325,000

Direct Labor 220,000

Manufacturing Overhead 408,471

----------------

Total Manufacturing cost $953,471

4. Cost of Goods Manufactured

Beginning Balance work in progress $56,000

Total manufacturing cost 953,471

Less:

Ending Bal. work in progress 24,471

----------------

Cost of goods manufactured $985,000

Cost of goods manufactured

Direct Materials

Beginning Raw materials Inventory $41,000

Add:

Purchases of raw materials 325,000

-----------------

Raw materials available for use 366,000

Minus:

Ending Raw materials inventory 41,000

----------------- -------------------

Raw Material used in production $325,000

Direct Labor 220,000

Manufacturing Overhead 408,471

Total Manufacturing Cost 953,471

Add:

Beginning work in progress inventory 56,000

Less:

Ending work in progress Inventory 24,471

--------------

Cost of goods manufactured $985,000