Inflation targeting in Emerging Market Economies

•

1 like•879 views

The presentation represents inflation targeting in EMEs, with a focus on various exchange rate regimes in Asian countries and their susceptibility to financial crisis.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (13)

Similar to Inflation targeting in Emerging Market Economies

Similar to Inflation targeting in Emerging Market Economies (20)

Recently uploaded

Recently uploaded (20)

Inflation targeting in Emerging Market Economies

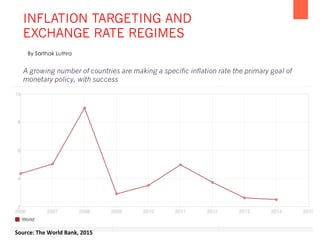

- 1. INFLATION TARGETING AND EXCHANGE RATE REGIMES A growing number of countries are making a specific inflation rate the primary goal of monetary policy, with success Source: The World Bank, 2015 By Sarthak Luthra

- 2. Table of Contents • What is Infla+on Targe+ng (IT)? • History of IT • Infla+on and Growth • IMF Classifica+on • Natural Classifica+on • Exchange Rate Arrangements • Asian Perspec+ve • Infla+on Targeters: Korea, Thailand, Philippines, and Indonesia • De Jure versus De Facto • Findings • Key Takeaways

- 3. “A monetary policy opera0ng strategy with four elements; an ins&tu&onalized commitment to price stability as the primary goal of monetary policy, mechanisms rendering the central bank accountable for a8aining its monetary policy goals, the public announcement of targets for infla0on, and a policy of communica&ng to the public and the markets the ra&onale for the decision taken by the central bank” Eichengreen, 2001 “This involves the public announcement of medium-term numerical targets for infla&on with an ins&tu&onal commitment by the monetary authority to achieve these targets. Addi0onal key features include increased communica&on with the public and the markets about the plans and objec&ves of monetary policymakers and increased accountability of the central bank for aDaining its infla0on objec0ves. Monetary policy decisions are guided by the devia0on of forecasts of future infla0on from the announced target, with the infla0on forecast ac0ng (implicitly or explicitly) as the intermediate target of monetary policy” IMF, 2015 What is Inflation Targeting (IT)?

- 4. One approach: Place exchange rate into interest rate rule it = gππt + gyyt + ge0et + ge1et-1 + ρit-1 where it is the nominal interest rate, πt is the infla+on rate (smoothed over four quarters), yt is the devia+on of real GDP from poten+al GDP, et is the exchange rate (higher e is an apprecia+on). Exchange rate in Policy Rule in IT Infla&on targe&ng and monetary policy rules: Experience and Research, John B. Taylor, Stanford University, 2000

- 5. What is Inflation Targeting (IT)? • Maintain price stability by focusing on devia+ons in published infla+on forecasts from an announced infla+on target (ECB, 2004) • Control the general rise in the price level - In this framework, a central bank es+mates and makes public a projected, or “target,” infla+on rate and then a_empts to steer actual infla+on toward that target, using such tools as interest rate changes * Because interest rates and infla+on rates tend to move in opposite direc+ons, the likely ac+ons a central bank will take to raise or lower interest rates become more transparent under an infla+on targe+ng policy • Strengthen the Central Bank (CB)’s accountability for a_aining those objec+ves “Infla+on targe+ng is a framework for monetary policy characterized by the public announcement of official quan+ta+ve targets for the infla@on rate […] stable infla@on is monetary policy’s primary long-run goal.” (Bernanke et al., 1999) Infla@on targe@ng is to:

- 6. What is Inflation Targeting (IT)? Key Takeaways: 1) Clear mandate for monetary policy to aim for low infla@on 2) CB independence – at least in terms of instrument 3) CB accountability for achieving mandate Alterna@ve defini@ons of IT

- 7. Why infla@on targe@ng: • High infla+on distorts decisions on investment, saving: may lead to slower economic growth; • Greater ins+tu+onal independence to central banks with monetary policy commitment ; • Prevent defla@on Monetary policy restric0ve (expansionary) if actual infla0on is systema0cally above (below) the infla0on target. • Nominal anchor to the economy. Ex. Currency peg Concern with the nominal anchor: Country’s monetary policy à DEPENDANT on the country to which it peggedà Limi+ng the central bank’s ability to respond to shocks (terms of trade or changes in real interest rate à Many countries began to adopt flexible exchange rates (New Anchor) History of IT – Why has it become popular? Infla@on targe@ng has been adopted in the early 1990s by industrial countries like New Zealand, Canada, the United Kingdom and Sweden, Mexico, and Czech republic

- 9. • Measure of infla&on to use? Consumer price index (CPI) or GDP deflator • Whether monetary policy should target all movements in infla@on • The target level of infla+on? • Whether to adopt an infla&on target point or target ranges? • Choice of policy horizon— speediness in decline of the target path. Issues in IT Benefits: • Low infla+on vola+lity (Svensson, 1997); • Cushioning of infla+onary shocks (Mishkin, 2004); • Anchoring of infla+on expecta+ons (Kohn, 2007, Swanson, 2006, Levin et al., 2004). Costs If infla+on targe+ng were implemented as a very strict policy rule then it could have some serious costs (Bernanke et al., 2003): • Restricted ability of the central bank to respond to financial crises; • Poor outcomes in employment, exchange rate and other macroeconomic variables; • Poten+al instability in the event of large supply-side shocks; • Lack of support from the public.

- 10. • Capital inflows à currency board monetary authority buys forex at fixed exchange rate, expanding monetary base. The interest rate are lowered and capital inflows are discouraged. • Case of automa+c adjustment mechanism. The interest rate à Capital inflows and ouqlows are balanced. If capital mobility is high, then the credible currency board will equate the domes+c interest rate with the one in the foreign country to which the peg is maintained (Hong Kong + US dollar). • Under the currency board, there is no room for independent monetary policy. Fixed Exchange rate regime (under currency board) Flexible Exchange rate regime The exchange rate is ler to the market force, while monetary policy is concentrated on the domes+c price stability. The central bank mandate is to keep the domes+c price stability, and interven+on into the foreign exchange market is kept minimal, if at all. *Three major economies—the US, the Euro land, and Japan—have adopted free floa@ng Fixed and Floating Exchange Rate Regimes

- 11. IMF Classification • Dependent on Fixed (sor/hard) and managed • 1950: 53% of all arrangements had two or more exchanges • Pegs reigned supremacy in early 1970s, with 90% of all the exchange rate arrangements • De jure – 8 classifica+ons and De Facto – 3 classifica+ons (Hard, Sor, and Floa+ng) Unified Exchange Rate Dual, Mul+ple, Parallel • Hard peg: Broadly consistent 13.1% • SoT peg: 42.9% Conven&onal peg:23.6% Stabilized Arrangement: 9.9% • Floa0ng: 34% Managed floa&ng: 18.3% Free floa&ng: 15.7% • Residual: 9.9%

- 12. The fine classification codes are: 1 No separate legal tender 2 Pre announced peg or currency board arrangement 3 Pre announced horizontal band that is narrower than or equal to +/-2% 4 De facto peg 5 Pre announced crawling peg 6 Pre announced crawling band that is narrower than or equal to +/-2% 7 De factor crawling peg 8 De facto crawling band that is narrower than or equal to +/-2% 9 Pre announced crawling band that is wider than or equal to +/-2% 10 De facto crawling band that is narrower than or equal to +/-5% 11 Moving band that is narrower than or equal to +/-2% (i.e., allows for both appreciation and depreciation over time) 12 Managed floating 13 Freely floating 14 Freely falling 15 Dual market in which parallel market data is missing. The course classification codes are: 1 No separate legal tender 1 Pre announced peg or currency board arrangement 1 Pre announced horizontal band that is narrower than or equal to +/-2% 1 De facto peg 2 Pre announced crawling peg 2 Pre announced crawling band that is narrower than or equal to +/-2% 2 De factor crawling peg 2 De facto crawling band that is narrower than or equal to +/-2% 3 Pre announced crawling band that is wider than or equal to +/-2% 3 De facto crawling band that is narrower than or equal to +/-5% 3 Moving band that is narrower than or equal to +/-2% (i.e., allows for both appreciation and depreciation over time) 3 Managed floating 4 Freely floating 5 Freely falling 6 Dual market in which parallel market data is missing. Taxonomy of Exchange Rate Arrangements

- 13. Natural Classification- Carmen Reinhart Database • Based on Market Determined rates • Be_er barometers of underlying monetary policy • Market determined exchange rates consistently an+cipates devalua+on of official rate (posi+ve coefficient) • Be_er correla+on of market exchange rate with infla@on (be_er pulse of monetary policy) • Presence of Dual (mul+ple) rates and parallel markets – in 1950 45% of the countries had dual or mul@ple exchange rates • In Official Classifica+on as managed floa+ng – 53% had de facto pegs, crawls, or narrow bands in natural classifica@on • Popular regimes in Emerging Asia and Western Hemisphere – Crawling peg (more than 36% and 42% of the observa+ons), 1990-2001 • New Category – Freely falling (13% of the observa+on with freely falling category in 1990), which is 3 +mes freely floa+ng category (Wherein the 12 month infla+on rate is above 40%) Ex Chile in 1956

- 14. Natural versus IMF Classifications • In Natural Classifica+on almost 40% of the regimes in 1950 were pegs • Between 1974–1990 the official classifica+on has roughly 60% of all regimes as pegs, natural classifica+on has only half as many àSome of natural pegs are not official pegs (vice-versa) • 1993 - “freely falling” con+nues to be a significant category, accoun+ng for 15 percent of all regime à declining trend from 2001-2010 • In 2010, 45% (Peg), 22% (De facto and pre announced crawling pegs), 19% (Managed floa+ng), 3% (Freely floa+ng). 0% (Freely falling), 2% (Dual and parallel markets) Overlap between IMF and Natural classifica+on IMF label in one way and Natural Clas. label it differently Natural classifica+on label in one way and IMF label in differently

- 15. Natural versus IMF Classifications • Natural classifica+on elevates limited flexibility as an important regime (unlike official arrangement) • Natural classifica+on (less than 10% between 1991-2001) has less freely floa+ng regimes vis-à-vis official classifica+on (more than 30%) à Fear of Floa+ng (Calvo and Reinhart, 2002) IMF Classification Probability in Natural Classification Natural Classification Peg 44% Flexible arrangment Float 31% Peg / limited flexibility Managed float 53% Peg / limited flexibility • Correla+on between Natural and Official Classifica+on: 0.42 • Greater overlap for European countries • Least overlap in developing countries

- 16. Transi@on - % of countries with different exchange rate regimes (1941 – 2010) 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 1940 1942 1944 1946 1948 1950 1952 1954 1956 1958 1960 1962 1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 ONE TWO THREE FOUR FIVE SIX WORLDWIDE EXCHANGE RATE REGIMES IMF Data on Exchange Rate Arrangements, Course Classifica&on, 1940-2010

- 17. • Recent development - Depolici@se exchange rate movements since soa pegs are suscep@ble to specula@ve aSacks à Increased pressure for developing countries to adopt corner solu+ons to exchange rates arrangements; • The exchange rate is an important variable for policy decisions; • Prior to 1990, Asian economies maintained fixed exchange rateàexchange rate stability is essen+al for promo+ng trade and investment; • Fixed exchange rate regime became difficult to maintain when the capital accounts were liberalized; • Some emerging market economies, including Mexico and Thailand, first received large capital inflows followed by large ouqlows; • When the central bank, faced with massive ouqlows, tried to maintain the fixed exchange rate and exhausted the foreign exchangeà CURRENCY CRISIS • Fear of apprecia+on – due to asymmetric exchange rate interven+on—i.e., a willingness to allow deprecia+ons but reluctance to allow apprecia+ons Impossibility of having capital mobility, the fixed exchange rate, and independent monetary policy, is oaen called “impossible trinity Asian Economies – A Perspective

- 18. • Asian crisis, the “two-corner solu+on” was advocated by the IMF and the United States. It says that the stable exchange rate regime is either the hard peg (currency board or dollariza+on) or free float. • Intermediate regimes àmanaged float/fixed exchange rate regime without a currency board arrangement, were regarded as inherently unstable. Fischer (2001) • Since 1998, the IMF has recommended to emerging market economies in addi+on to advanced countries a combina+on of free float and infla@on targe@ng in order to lessen the probability of a currency crisis with stability of domes+c prices. • The free float regime, seemed to have gained more popularity, and so has infla+on targe+ng. In East Asia, Korea, Thailand, the Philippines, and Indonesia adopted infla+on targe+ng since 1998 • Many EM countries adopted a fully-fledged IT regime or many elements of it in the late 1990s as a transi+on arrangement, mostly in response to difficul+es in keeping pegged currencies stable in the wake of the East Asian crisis. During 2003–2011, the move from fixed exchange rate arrangements to infla+on targe+ng or mixed policy regimes con+nued among EM countries Post Asian Crisis

- 21. In East Asia, Korea, Thailand, the Philippines, and Indonesia adopted infla@on targe@ng since 1998 Inflation Targeting Economies – East Asia

- 22. 0 200 400 600 800 1000 1200 0 2000 4000 6000 8000 10000 12000 14000 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 Indonesia 0.00 5.00 10.00 15.00 20.00 25.00 30.00 35.00 40.00 45.00 50.00 -5.00 0.00 5.00 10.00 15.00 20.00 25.00 30.00 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 Thailand 0.00 10.00 20.00 30.00 40.00 50.00 60.00 0.00 10.00 20.00 30.00 40.00 50.00 60.00 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 Philippines Korea 0.00 200.00 400.00 600.00 800.00 1000.00 1200.00 1400.00 1600.00 0 5 10 15 20 25 30 35 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 Inflation and Exchange Rate Movements Infla@on (Blue and Lea Axis) Exchange rate (Red and Right Axis)

- 25. Country De Jure Exchange Rate Regimes in Asia' Bangladesh The exchange rates set by the dealer banks themselves, based on Demand and-supply interaction. Bangladesh Bank is not present in the market on a day-to-day basis and undertakes purchase/sale transactions with dealer banks (if need be) PRC 2005 - managed floating exchange rate regime based on market supply and demand (link to basket of currencies). The new exchange rate system has operated stably The exchange rate of the RMB against US dollar has been moving both upward and downward with greater flexibility Hong Kong, SAR 1983 - Hong Kong dollar linked to US dollar Maintained under strict and robust Currency Board system (requiring) both the stock and the flow of the Monetary Base to be fully backed by foreign reserves India Monitoring and management of exchange rates with flexibility, without a fixed target or a pre-announced target or a band Indonesia 2005- Bank Indonesia launched new monetary policy known as the Inflation targeting framework: (1) use of the BI rate as a reference rate in monetary control in replacement of the base money operational target (2) forward looking monetary policymaking process (3) more transparent communications strategy (4) strengthening of policy coordination with the Government The rupiah exchange rate is determined wholly by market supply and demand Korea Inflation targeting - Central bank announces an explicit inflation target and achieves its target directly. Inflation targeting places great emphasis on inducing inflation expectations to converge on the central bank’s inflation target level by the prior public announcement and successful attainment of that target level The exchange rate is, in principle, decided by the interplay of supply and demand in the foreign exchange markets Malaysia 2005 - Shifted from a fixed exchange rate regime to a managed float against a basket of currencies Exchange rate determined demand and supply in the foreign exchange market. Economic fundamentals and market conditions are the primary determinants of the level of the ringgit exchange rate Pakistana Floating inter-bank exchange rate since 2001 Monetary-cum-exchange rate policies are judgment- and discretion-based rather than model- or rule-based Philippines 2002 - Inflation targeting framework for monetary policy in January 2002 The Monetary Board determines the exchange rate policy of the country, determines the spot rates Singapore 1981 - monetary policy has been centered on the management of the exchange rate. (1) Managed against a basket of currencies of its major trading partners and competitors. (2) Monetary Authority of Singapore operates a managed float regime withtrade-weighted exchange rate (3) Use of exchange rate as the intermediate target --> MAS gives up control over domestic interest rates (and money supply). Sri Lanka Independently floating exchange rate regime within a framework of targeting monetary aggregates Reserve money (i.e., high powered money) as the operating target broad money (M2b) as the intermediate target. Thailand 1997 - Managed-float exchange rate regime Value of baht is determined by market forces (both on-shore and off-shore foreign exchange market Bank of Thailand implements monetary policy by influencing short-term money market rates Viet Nam Crawling peg with the US dollar for its exchange rate Set official exchange rate daily and dealing rate within a trading band of plus or minus 0.25%percent. Currencey if depreciated against US dollar by keeping the exchange rate on an upward trend. De Jure Exchange Rate Classification- Asia The evolu&on and impact of Asian Exchange rate regimes, Ramkishen S. Rajan no. 208, July 2010

- 26. De Facto Exchange Rate Classification- Asia

- 27. Key components of Inflation Targeters The evolu&on and impact of Asian Exchange rate regimes, Ramkishen S. Rajan no. 208, July 2010

- 28. • There is no discrepancy between the de jure and de facto regimes of Hong Kong, China, which operates an exchange rate fixed to the US dollar • India, Malaysia, Pakistan, Singapore, and Thailand are categorized as managed floaters, broadly consistent with their official pronouncements • Korea and the Philippines are characterized as independent floaters, consistent with their official asser+ons but somewhat odd in view of the fact that both countries have been rapidly building up reserves. • Viet Nam is classified as having a conven+onal fixed peg regime compared to its official pronouncement of maintaining a crawling peg and band around the US dollar. • Bangladesh, Indonesia, and Sri Lanka have also been characterized as managed floaters (with no predetermined exchange rate path), despite their official declara+ons of being independent floaters Findings

- 29. • Central banks should prac@ce both infla@on targe@ng and substan@al interven@on • The correla@on between the infla@on rate and the exchange rate movement is reviewed for Asian infla@on targe@ng countries • Monetary policy ac@ons in order to keep the infla@on rate stable can internalize the impact on the exchange rate from the infla@on shock • An exchange rate shock may be countered by monetary policy that will keep both the exchange rate and the infla@on rate stable Key Takeaways

- 30. • Exchange rate arrangements for East Asia post- crisis: examining the case for open economy infla+on targe+ng, Tony Cavoli and Ramkishen Rajan, April 2003 • IMF policy paper, condi+onality in evolving monetary policy regimes, March 2014 • The role of exchange rate in infla+on targe+ng, Takatoshi Ito, University of Tokyo, post-conference version final, May 2007 • The country chronologies and background material to exchange rate arrangements into the 21st century: Will the anchor currency hold? Ethan ilzetzki, London School of Economics, Carmen M. Reinhart, University of Maryland and NBER, Kenneth S. Rogoff, Harvard university and NBER, March 2011 • Annual report on exchange arrangements and exchange restric+ons, IMF, 2014 • Infla+on targe+ng turns 20, ScoD Roger , March 2010 • The evolu+on and impact of Asian Exchange rate regimes, Ramkishen S. Rajan no. 208, July 2010 • Characterizing exchange rate regimes in post-crisis east asia, Taimur Baig, IMF, Asia and Pacific department, October 2001 • De jure versus de facto exchange rate regimes in sub-saharan africa, Slavi Slavov, imf, August 2011 • Exchange rate arrangements entering the 21st century: which anchor will hold?, Ethan Ilzetzki, Carmen M. Reinhart and Kenneth S. Rogoff • The modern history of exchange rate arrangements: a reinterpreta+on*, Carmen m. Reinhart and Kenneth S. Rogoff, quarterly journal of economics, February 2004 • Macroeconomic policy, the defini+on of infla+on targe+ng, Jennifer Smith - University of Warwick Bibliography