Recommended

More Related Content

Viewers also liked

Similar to A mdel to estimate the value of the option to abandon a project or investment

Similar to A mdel to estimate the value of the option to abandon a project or investment (20)

More from Soumitra Kansabanik

Recently uploaded

Recently uploaded (20)

A mdel to estimate the value of the option to abandon a project or investment

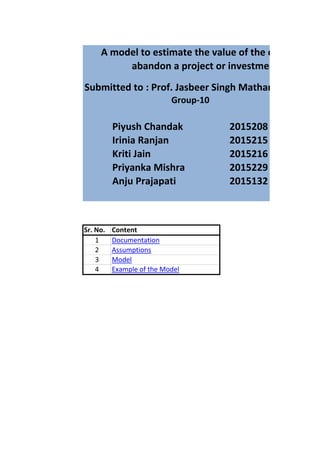

- 1. Submitted to : Prof. Jasbeer Singh Matharu Piyush Chandak 2015208 Irinia Ranjan 2015215 Kriti Jain 2015216 Priyanka Mishra 2015229 Anju Prajapati 2015132 Sr. No. Content 1 Documentation 2 Assumptions 3 Model 4 Example of the Model A model to estimate the value of the option to abandon a project or investment Group-10

- 2. Matharu of the option to estment

- 3. 1 Project's present value will drop by roughly 1/n each year into the project 2 Riskfree rate is assumed as 7% that is equal to Treasury bond rate 3 Time of abandonment is considered as time of option life 4 Tenue of the project more than 10 years should not be considered ASSUMPTIONS

- 4. VALUING AN OPTION TO ABANDON A PROJECT Table 1 : Input Data related to Net Present Value of the Project Initial investment in the project Expected cash flow each year Tenure of the project Discount rate Table 2: Calculation of Present Value of the Project Year Cash Flow 0 0 1 0 2 0 3 0 4 0 5 0 6 0 7 0 8 0 9 0 10 0 PV of investment 0 Table 3: Inputs relating the underlying asset Present value of cash flows from project 0 Variance in Underlying Assets's Value Annualized standard deviation in ln(present value of CF) 0.00% Remaining life of the project Salvage Value on abandonment Time to expiration Enter the riskless rate that corresponds to the option lifetime = Output relating to long term option Table 4: VALUING A LONG TERM OPTION Stock Price 0.00 Treasury Bond Rate Strike Price 0.00 Variance Expiration (in years) 0 Annualized dividend yield d1 = N(d1) = d2 = N(d2) = Value of Option to Abandon =

- 5. ECT in million Rs. in million Rs. in years in million Rs. in % in years in million Rs. in years in % sury Bond Rate 0.00% 0 ualized dividend yield

- 6. VALUING AN OPTION TO ABANDON A PROJECT Table 1 : Input Data related to Net Present Value of the Project Initial investment in the project 100 Expected cash flow each year 45 Tenure of the project 10 Discount rate 12% Table 2: Calculation of Present Value of the Project Year Cash Flow 0 -100 1 45 2 45 3 45 4 45 5 45 6 45 7 45 8 45 9 45 10 45 PV of investment 254 Table 3: Inputs relating the underlying asset Present value of cash flows from project 254 Variance in Underlying Assets's Value 0.09 Annualized standard deviation in ln(present value of CF) 30.00% Remaining life of the project 10 Salvage Value on abandonment 150.00 Time to expiration 5 Enter the riskless rate that corresponds to the option lifetime = 7.00% Output relating to long term option Table 4: VALUING A LONG TERM OPTION Stock Price 254.26 Treasury Bond Rate Strike Price 150.00 Variance Expiration (in years) 5 Annualized dividend yield d1 = 0.898485228 N(d1) = 0.815536542 d2 = 0.227664835 N(d2) = 0.590046594 Considering that a company XYZ Ltd. is considering a 10-years project which requires an initial investment of Rs. 100 million i the project from the project is Rs. 45 million. The company has the option to abandon this project anytime by selling its share 150 million. A simulation of the cash flows on the time share investment yields a variance in the present value of the cash flo discount rate is 12%.

- 7. Value of Option to Abandon = $14.89

- 8. ECT in million Rs. in million Rs. in years in million Rs. in % in years in million Rs. in years in % sury Bond Rate 7.00% 0.09 ualized dividend yield 10.00% investment of Rs. 100 million in a real estate firm. The expected cash flow from ject anytime by selling its share back to the developer in the next 5 years for Rs. e present value of the cash flows from being in the partnership is 0.09. The