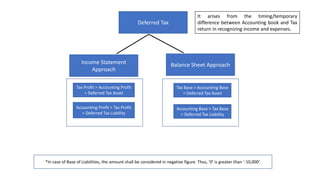

1. Deferred Tax

Income Statement

Approach

Balance Sheet Approach

It arises from the timing/temporary

difference between Accounting book and Tax

return in recognizing income and expenses.

Tax Profit > Accounting Profit

= Deferred Tax Asset

Accounting Profit > Tax Profit

= Deferred Tax Liability

Tax Base > Accounting Base

= Deferred Tax Asset

Accounting Base > Tax Base

= Deferred Tax Liability

*In case of Base of Liabilities, the amount shall be considered in negative figure. Thus, ‘0’ is greater than ‘-10,000’.

2. Example: Depreciation

An Office Equipment has been Purchased at cost of 100,000 and depreciated in straight line basis. Suppose, For Tax

purpose, reducing Balance method depreciation of 10% is used. Consider Profit Before tax and Depreciation is 50,000.

Year Depreciation

(Accounting)

Depreciation

(Tax)

Difference Deferred Tax Entry Income Tax Entry

1 20,000 10,000 10,000

(Tax profit > Accounting Profit)

Deferred Tax Asset Dr----- 3,000

Deferred Tax Income Cr ---------3,000

Income Tax Expense – Dr 12,000

Provision for Tax----------Cr 12,000

2 20,000 9,000 11,000

(Tax profit > Accounting Profit)

Deferred Tax Asset Dr----- 3,300

Deferred Tax Income Cr ---------3,300

Income Tax Expense – Dr 12,300

Provision for Tax----------Cr 12,300

3 20,000 8,100 11,900

(Tax profit > Accounting Profit)

Deferred Tax Asset Dr----- 3,000

Deferred Tax Income Cr ---------3,000

Income Tax Expense – Dr 12,570

Provision for Tax----------Cr 12,570

4 20,000 7,290 12,710

(Tax profit > Accounting Profit)

Deferred Tax Asset Dr----- 3,813

Deferred Tax Income Cr ---------3,813

Income Tax Expense – Dr 12,813

Provision for Tax----------Cr 12,813

5 20,000 6,561 13,439

(Tax profit > Accounting Profit)

Deferred Tax Asset Dr----- 4,031

Deferred Tax Income Cr ---------4,031

Income Tax Expense – Dr 13,031

Provision for Tax----------Cr 13,031

6 0 5,905 5,905

(Accounting Profit > Tax Profit)

Deferred Tax Expense – Dr----1,771

Deferred Tax Asset - Cr----------1,771

Income Tax Expense – Dr 13,228

Provision for Tax----------Cr 13,228

3. Yea

r

Accounti

ng Base

Tax

Base

Temporary Difference Deferred Tax Deferred Tax Entry Income Tax Entry

1 80,000 90,000 10,000

(Tax base > Accounting base)

3000 (Asset) Deferred Tax Asset Dr----- 3,000

Deferred Tax Income Cr ---------3,000

Income Tax Expense – Dr 12,000

Provision for Tax----------Cr 12,000

2 60,000 81,000 21,000

(Tax base > Accounting base)

6,300 (Asset) Deferred Tax Asset Dr----- 3,300

Deferred Tax Income Cr ---------3,300

Income Tax Expense – Dr 12,300

Provision for Tax----------Cr 12,300

3 40,000 72,900 32,900

(Tax base > Accounting base)

9,870 (Asset) Deferred Tax Asset Dr----- 3,000

Deferred Tax Income Cr ---------3,000

Income Tax Expense – Dr 12,570

Provision for Tax----------Cr 12,570

4 20,000 65,610 45,610

(Tax base > Accounting base)

13,683 (Asset) Deferred Tax Asset Dr----- 3,813

Deferred Tax Income Cr ---------3,813

Income Tax Expense – Dr 12,813

Provision for Tax----------Cr 12,813

5 0 59,049 59,049

(Tax base > Accounting base)

17,714 (Asset) Deferred Tax Asset Dr----- 4,031

Deferred Tax Income Cr ---------4,031

Income Tax Expense – Dr 13,031

Provision for Tax----------Cr 13,031

6 0 53,144 53,144

(Tax base > Accounting base)

15,943 (Asset) Deferred Tax Expense – Dr----1,771

Deferred Tax Asset - Cr----------1,771

Income Tax Expense – Dr 13,228

Provision for Tax----------Cr 13,228